Key Data Snapshot

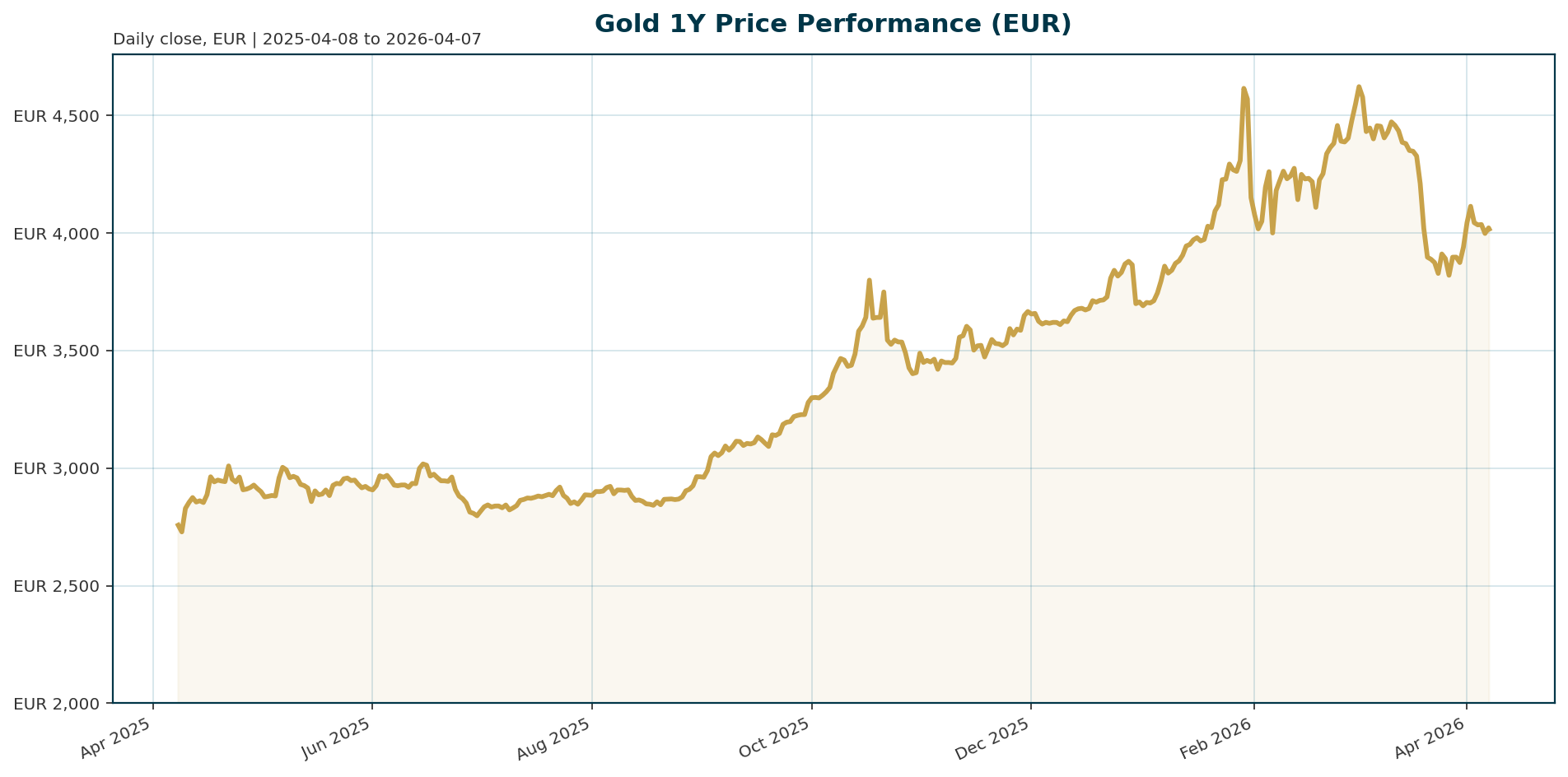

Gold is currently correcting from a January 2026 peak, trading at 4016.6 EUR. The metal has experienced significant volatility, with a 30-day decline of 9.84% and a 24-hour change of -0.09%. Despite the short-term pullback, the asset remains in a strong long-term uptrend, up 44.22% over the last year and 29.35% over 200 days.

| Metric | Value | Context |

|---|---|---|

| Spot Price (XAU/EUR) | 4,016.60 | Current market price |

| 24h Change | -0.09% | Marginal decline |

| 30-Day Return | -9.84% | Short-term correction |

| 1-Year Return | +44.22% | Strong long-term trend |

| All-Time High (ATH) | 4,688.32 EUR | Jan 29, 2026 |

| ATH Drawdown | -14.31% | Current pullback level |

| BTC Dominance | 56.60% | Market share of crypto |

| Gold ETF AUM | $701 Billion | Record high assets |

Macro Backdrop

The current environment presents a dichotomy for gold. The bearish pressure comes from the Federal Reserve holding rates at 3.5% to 3.75% and the 10-year US Treasury yield nearing 4.5%. These factors increase the opportunity cost of holding non-yielding gold, while the dollar rebound has exacerbated the price decline [T1][T8].

Conversely, the bullish structural backdrop is supported by sticky inflation (2.4% YoY) and a deteriorating US fiscal position. The national debt has reached $39 trillion, with annual net interest payments expected to hit $1 trillion. This debt burden may force policymakers to cut rates even if inflation remains elevated, creating a favorable environment for hard assets [T5][T7]. The ECB sits at the midpoint of its neutral rate estimate (2%), leaving room for further tightening or a pivot depending on inflation outcomes.

Investment Thesis

The core thesis for gold in 2026 rests on its role as a hedge against fiscal deterioration and currency debasement. Despite the recent correction, gold remains fundamentally undervalued when compared to the US debt burden. Today, US gold reserves represent only approximately 3% of federal debt, a stark contrast to the 51% ratio recorded in the 1940s [T5].

Additionally, gold is positioned as a hedge against stagflation. Even if the Iran conflict de-escalates, energy prices are likely to remain elevated, supporting inflation expectations. Gold tends to rally during periods of rising inflation, particularly when it is unexpected and prolonged [T1]. The market is currently not pricing in recession risks or full-blown stagflation fears, leaving room for upside should these scenarios materialize.

Bullish Drivers

Central Bank Diversification: Global central banks remain a pillar of support, maintaining a net buying trend. In February, central banks purchased 19 metric tons of gold, continuing a trend of reserve diversification away from the US dollar despite rising geopolitical uncertainty [T6]. While net buying volume slowed to 863 tonnes last year, the dollar value of purchases reached record highs [T1].

ETF Inflows: Physical gold ETFs have demonstrated remarkable resilience, adding $5.3 billion in February and reaching a record AUM of $701 billion. This streak of nine consecutive months of inflows indicates sustained institutional interest, though March saw net redemptions on track for the steepest decline since 2022, suggesting a flush of frothy positioning [T4][T1].

Geopolitical Fragmentation: The search for alternative reserve assets is driving infrastructure development. Singapore is actively considering expanding gold storage facilities to attract global central banks, aiming to challenge London’s dominance in the bullion market [T3].

Relative Positioning vs Bitcoin and Ethereum

Gold maintains its status as the premier safe haven asset, contrasting sharply with the risk-on correlation of Bitcoin and Ethereum. With Bitcoin dominance at 56.6%, the crypto market remains highly sensitive to macro liquidity conditions [market_data].

Gold’s inverse sensitivity to US yields and the dollar provides a distinct risk management tool compared to digital assets. While crypto markets often move in tandem with equities during risk-on periods, gold tends to outperform when risk sentiment collapses, offering a crucial diversification benefit within a portfolio.

Scenario Framework

- Bull Case (Target $5,400/oz): The Federal Reserve delivers the expected 50 basis points of rate cuts by year-end. The Iran conflict de-escalates, stabilizing oil prices and reducing safe-haven volatility. Speculative positioning normalizes, and central bank buying continues unabated [T2].

- Base Case (Consolidation): The Fed maintains a hawkish hold, with inflation proving sticky. Gold trades in a range, supported by central bank buying and debt concerns, but capped by elevated real yields. The asset consolidates around current levels as the market waits for clearer policy signals.

- Bear Case (Support Test): Geopolitical risks escalate, disrupting the Strait of Hormuz. US yields remain above 4.5%, and ETP redemptions accelerate. Gold faces further liquidation pressure, potentially testing support levels as investors rotate into cash or the strengthening dollar.

Valuation Discussion

Gold’s valuation is currently dictated by the real yield environment. The traditional inverse relationship between gold prices and real yields has reasserted itself as expectations for immediate Fed rate cuts have waned [T1].

With nominal Fed rates at 3.5% to 3.75% and inflation at 2.4%, real yields are estimated to be approximately 1.35%. This positive real yield environment acts as a headwind for gold. For the metal to reach its potential upside, a sustained decline in real yields is required, likely triggered by aggressive Fed easing to address the $1 trillion annual interest burden [T5][T8].

Risks

- Geopolitical Escalation: The Iran war entering its fifth week poses a significant risk. Persistent disruption to the Strait of Hormuz could trigger a spike in oil prices and renewed safe-haven demand, potentially exacerbating inflation and prompting central banks to remain hawkish [T2][T4].

- Yield Reversal: If the 10-year Treasury yield breaks above 4.5% and stays there, the opportunity cost of holding gold will rise, triggering a deeper correction. The recent strength of the dollar has already demonstrated gold’s sensitivity to these metrics [T8].

- Positioning Flush: Net ETP redemptions in March are on track for the steepest decline since 2022. If liquidation accelerates faster than anticipated, it could lead to a “flush” of profitable positions, creating short-term volatility and downside pressure [T1].

Appendix

Sources

- Reasons to be bullish on gold – ft.com [T1]

- Gold on track for worst month since 2008 as Iran war enters its fifth week – CNBC [T2]

- Singapore weighs adding gold storage for global central banks – Mining.com [T3]

- UBS has surprising message for gold investors after recent weakness – TheStreet [T4]

- Gold pullback offers profit opportunity as debt risks grow, says analyst – CryptoRank [T5]

- Central banks remain net gold buyers in February despite rising geopolitical uncertainty – KITCO [T6]

- War deal – Financial Times [T7]

- Treasury market’s next test: rising war costs – kitco.com [T8]

Disclaimer: This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed herein are those of the author and do not reflect the official policy or position of any institution.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.