Key Data Snapshot

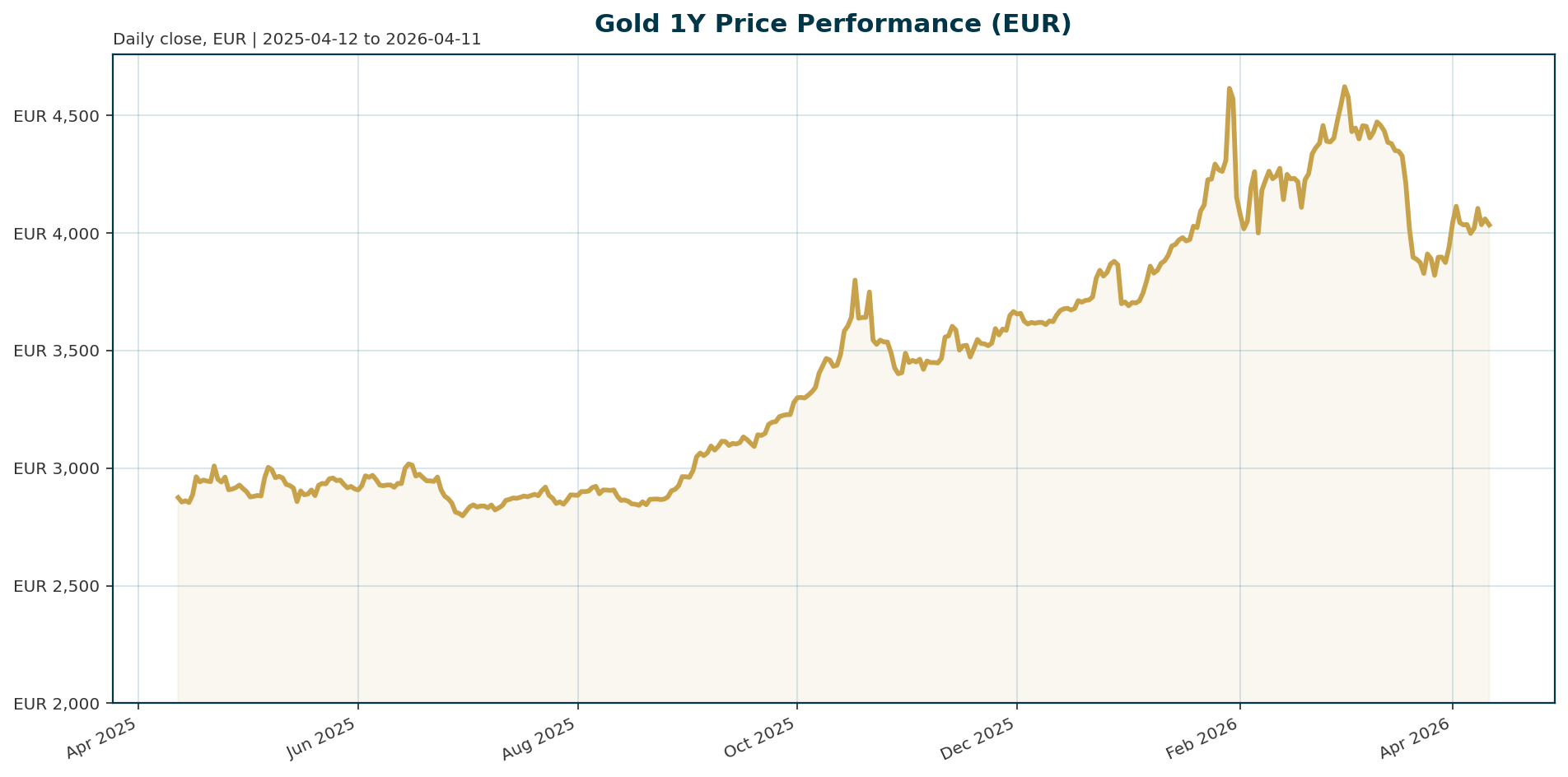

Gold (XAU/EUR) is currently navigating a consolidation phase following a robust 1-year rally. The metal is trading 13.95% below its January 2026 all-time high (ATH) of 4688.32 EUR, reflecting short-term headwinds from monetary tightening, yet remains up 218.83% from its 2019 low.

| Metric | Value |

|---|---|

| Current Price (EUR) | 4,034.23 |

| 24h Change | -0.69% |

| 30d Change | -9.65% |

| 1Y Change | +40.56% |

| ATH (Jan 29, 2026) | 4,688.32 (-13.95% drawdown) |

| Market Cap | 2.05B EUR |

| Circulating Supply | 507,641.80 t oz |

Macro Backdrop

The immediate macro environment presents a dichotomy between cyclical headwinds and structural tailwinds. On the negative side, rising real yields and higher energy prices have rekindled inflation fears, prompting a hawkish pivot in Fed expectations where rate hikes are now priced in [T1]. This increases the opportunity cost of holding non-yielding gold. However, the structural backdrop remains supportive. Lofty fiscal deficits and the risk of debt servicing crises are creating a “policy pivot” narrative, suggesting that central banks may eventually be forced to cut rates despite inflationary pressures [T2].

Investment Thesis

The investment thesis for Gold is anchored in its role as a strategic diversifier and a hedge against currency debasement. Despite recent volatility, the sector remains under-owned and undervalued when viewed through the lens of global debt dynamics. A critical argument posits that policymakers will be compelled to lower rates to alleviate the severe strain of debt servicing, creating a favorable environment for gold [T2]. Furthermore, gold serves as a necessary anchor in diversified portfolios to hedge against geopolitical uncertainty and currency volatility [T8].

Bullish Drivers

Structural demand from central banks is the primary bullish catalyst. BRICS+ nations now hold over 6,000 tonnes of gold, representing 17.4% of global reserves, up from 11.2% in 2019, signaling a permanent structural shift in reserve management [T5]. China has maintained a 17-month streak of gold accumulation, while France repatriated its last US-held gold, generating a $15 billion capital gain and reinforcing the trend of de-dollarization [T6][T7]. Geopolitical risk has surged to the top concern for central banks (70% of respondents), making gold the primary beneficiary of this uncertainty [T3][T4].

Relative Positioning vs Bitcoin and Ethereum

Direct quantitative comparison metrics for Bitcoin and Ethereum are unavailable in this dataset. However, qualitatively, Gold maintains its status as the traditional “anchor” asset in portfolios, often decoupling from risk-on assets during geopolitical shocks. While digital assets may trade on distinct narratives such as AI or decentralized finance, gold’s role as a store of value and a hedge against fiat debasement remains distinct from the high-beta nature of the crypto market. Gold’s correlation with traditional macro factors like real yields and inflation expectations currently provides a more predictable risk profile compared to the volatility seen in the cryptocurrency sector.

Scenario Framework

- Base Case (Hawkish Hold): Real yields stabilize as inflation fears moderate. Gold consolidates between 3800 and 4100 EUR, supported by central bank buying but capped by higher opportunity costs.

- Bull Case (De-dollarization & De-escalation): The dollar continues its moderation trend, and geopolitical tensions ease. Central bank diversification accelerates, pushing prices toward or above the ATH (4800+ EUR) [T1][T5].

- Bear Case (Yield Shock): Inflation spikes due to energy price shocks, forcing aggressive rate hikes. Gold corrects sharply, testing support levels below 3500 EUR [T2][T3].

Valuation Discussion

Valuation metrics suggest Gold is currently undervalued relative to its historical role in the monetary system. The US holds approximately 3% of its federal debt in gold reserves, a stark contrast to the 51% held in the 1940s [T2]. This massive under-coverage implies significant “dry powder” for future demand. Additionally, the dollar’s share of global reserves has fallen to 57%, the lowest since 1994, while gold’s share has more than doubled to over 23% [T5]. This structural rebalancing argues that the current price of 4034.23 EUR does not fully price in the long-term implications of reserve diversification.

Risks

- Real Yield Spike: A resurgence in inflation could force the Fed to hike rates, crushing the gold price [T1][T2].

- Dollar Reversal: If the dollar strengthens significantly, it could erode the price of gold in EUR terms despite domestic demand [T3][T4].

- Chinese Jewelry Demand: High gold prices are currently stifling demand in the Chinese jewelry sector, creating a potential demand bottleneck [T1].

Appendix

Sources

- Gold’s demand drivers ‘should once again reassert themselves’ after Iran war shock fades – Merrill’s Avioli – Shanghai Metals Market [T1]

- Gold pullback offers profit opportunity as debt risks grow, says analyst – CryptoRank [T2]

- Central banks’ concern over rising geopolitical tensions surges, survey shows – Reuters [T3]

- Central banks’ concern over rising geopolitical tensions surges, survey shows – KITCO [T4]

- BRICS+ nations hold over 17% of world’s gold reserves: report – Mining.com [T5]

- China’s central bank maintains gold buying for 17th month – Mining.com [T6]

- France pulls last gold held in US for $15B gain – Mining.com [T7]

- Gold remains an “anchor” in a diversified portfolio – FTSE Russell’s Indrani De – KITCO [T8]

AI-generated, for informational purposes only. This report does not constitute investment advice. Always conduct your own research before making financial decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.