Key Data Snapshot

| Asset | Symbol | Price (EUR) | 7D Change | 30D Change | YTD Change | 200D Change | ATH (EUR) | ATH Drawdown |

|---|---|---|---|---|---|---|---|---|

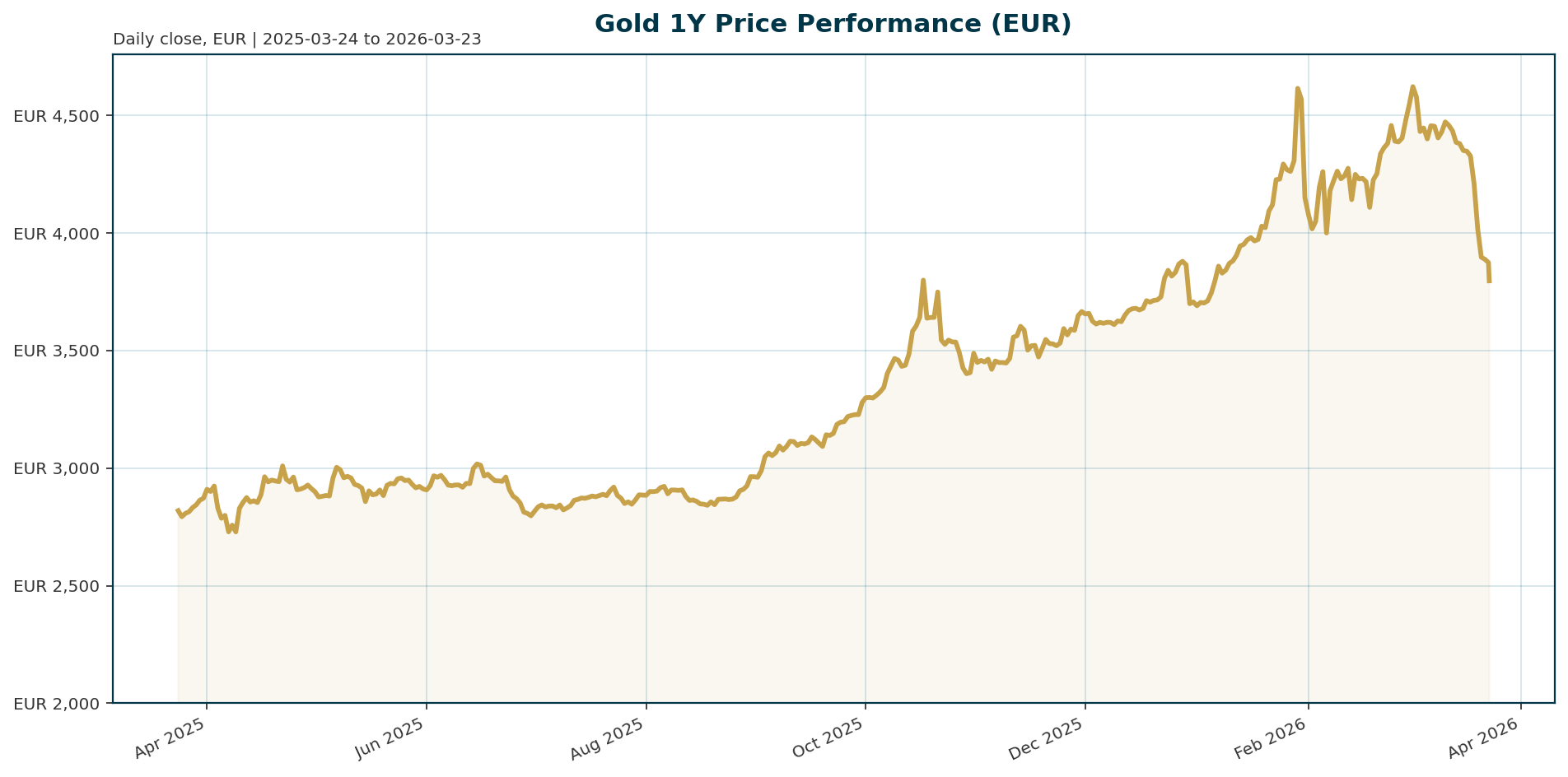

| Gold | XAU | 3,796.51 | -13.24% | -12.55% | +35.42% | +24.77% | 4,688.32 | -19.25% |

Interpretation: Gold is in a deep correction phase following its January 2026 all-time high. The metal has shed 13.24% over the last week, reflecting a sharp rotation out of safe-haven assets as markets price in delayed monetary easing. Despite the short-term weakness, the long-term secular bull trend remains intact, evidenced by a 35.4% year-to-date gain and a positive 200-day trend.

Macro Backdrop

The current macro environment is defined by a “higher-for-longer” monetary policy stance and energy-driven inflationary pressures. The Federal Reserve is widely expected to hold interest rates steady for a second consecutive meeting, with futures markets pricing in only one rate cut for September 2026 [T2]. This delay in easing is pressuring the non-yielding nature of gold. Concurrently, the U.S.-Israel conflict with Iran has disrupted energy flows through the Strait of Hormuz, pushing oil prices above $100 per barrel [T1][T3]. This surge in energy costs is stoking inflation fears, prompting major central banks including the European Central Bank and the Bank of England to signal a hawkish tilt, potentially raising rates as early as April [T4][T5]. The divergence between the Fed and European peers is creating a complex backdrop where gold faces headwinds from real yield pressure while simultaneously benefiting from geopolitical uncertainty.

Investment Thesis

The investment thesis for Gold is currently a balancing act between two opposing macro forces. On one hand, the “higher-for-longer” rate narrative and elevated real yields make gold structurally expensive, as seen in the recent 19% drawdown from the January peak [T8]. On the other hand, the prolonged Iran conflict introduces significant stagflation risks and geopolitical uncertainty. Analysts suggest that long-term drivers such as central bank diversification and hedging demand remain intact, potentially supporting higher prices by the end of 2026 [T2]. The thesis relies on the assumption that the Fed will eventually pivot to dovishness once inflationary pressures from the energy shock subside, or that the geopolitical risks will force a re-evaluation of the “higher-for-longer” stance.

Bullish Drivers

- Geopolitical Uncertainty: The intensifying conflict in the Middle East and the potential for a blockade of the Strait of Hormuz are driving hedging demand. Analysts note that the longer the conflict persists, the higher the risk of negative economic impacts, which supports gold [T1][T6].

- Central Bank Diversification: Long-term structural demand from central banks remains a key pillar of support. Despite short-term volatility, these institutions continue to accumulate gold as a hedge against currency debasement and systemic risk [T2][T5].

- Stagflation Risks: The combination of high oil prices and potential economic slowdowns creates a stagflationary environment. In such scenarios, gold serves as a superior hedge compared to interest-bearing assets, as it preserves purchasing power without generating yield [T2][T6].

- Technical Rebound Potential: Following a third consecutive weekly decline, some strategists suggest that a move back above $4,800 USD (implying a recovery in EUR terms) could ease downside pressure and signal a move toward new highs [T4].

Relative Positioning vs Bitcoin and Ethereum

In the current macro backdrop, Gold is positioned to outperform speculative risk-on assets such as Bitcoin and Ethereum. The “higher-for-longer” interest rate environment and the focus on inflation hedging favor hard assets with a proven store of value. While crypto assets are sensitive to rate cuts and liquidity, Gold offers a distinct “rate hedge” utility that becomes more attractive during periods of heightened inflation and geopolitical tension. Consequently, relative strength is likely to favor Gold until the Federal Reserve signals a clear dovish pivot and the risk-on trade re-asserts itself.

Scenario Framework

- Base Case: The Fed holds rates steady through mid-2026. Oil prices remain elevated but stable. Gold consolidates in a range between 3,700 and 4,000 EUR, trading sideways as markets await clarity on the duration of the Iran conflict.

- Bull Case: The Iran conflict de-escalates, reducing energy supply fears. The Fed cuts rates in September 2026 as inflation moderates. Gold reclaims its January ATH, targeting 4,800+ EUR.

- Bear Case: Oil prices spike further due to a prolonged blockade, cementing high inflation. The Fed delays cuts into 2027. Gold tests the 3,000 EUR support level as the “higher-for-longer” narrative dominates.

Valuation Discussion

Current valuations reflect a correction within a broader secular bull market. The 19.25% drawdown from the January all-time high is a standard pullback in a trend that has seen a 35.4% year-to-date gain. However, the inverse correlation between gold and real yields remains a critical valuation driver. With real yields elevated due to the hawkish Fed stance, gold is structurally expensive. The 200-day moving average trend of +24.77% suggests that the long-term uptrend remains intact, but short-term valuations are likely to remain range-bound until real yields normalize.

Risks

- Oil Shock Persistence: If the blockade of the Strait of Hormuz continues, oil prices could remain above $100 per barrel, forcing the Fed to delay rate cuts indefinitely and putting sustained downward pressure on gold [T1][T3].

- Geopolitical De-escalation: A sudden resolution to the Iran conflict could remove the geopolitical hedge, leading to a sharp rotation out of gold and into riskier assets [T6].

- European Hawkishness: If the ECB and BoE raise rates aggressively in April, the EUR could strengthen, making gold more expensive for international investors and dampening demand [T4][T5].

Appendix

Sources

- Gold falls as inflation fears pressure Fed rate-cut outlook – CNBC [T1]

- Gold eases as inflation fears bolster hawkish Fed bets – KITCO [T2]

- Gold rises but face third straight weekly drop on higher rate outlook – KITCO [T4]

- Gold steady as markets track Iran war tensions and await Fed decision – KITCO [T6]

- Central banks talk tough on inflation after 2021-22 lessons: EFG Bank – CNBC [T5]

- Gold Heading for Biggest Weekly Drop Since Start of Covid-19 Pandemic – Barron’s [T8]

Disclaimer: This report is AI-generated for informational purposes only and does not constitute investment advice. The analysis presented is based on data available as of March 23, 2026, and may become outdated. Readers should conduct their own due diligence before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may contain AI-assisted analysis or be generated entirely by AI, which processes market data from publicly available sources for which altii accepts no responsibility for its accuracy. We strongly advise against using this report as a basis for investment decisions.

DE: Dieser Bericht kann KI-gestützte Analysen enthalten oder vollständig von KI erstellt worden sein, die Marktdaten aus öffentlich zugänglichen Quellen verarbeitet, für deren Richtigkeit altii keine Verantwortung übernimmt. Wir raten dringend davon ab, diesen Bericht als Grundlage für Anlageentscheidungen zu verwenden.