Key Data Snapshot

| Asset | XAU (Gold) | Quote Currency | EUR |

|---|---|---|---|

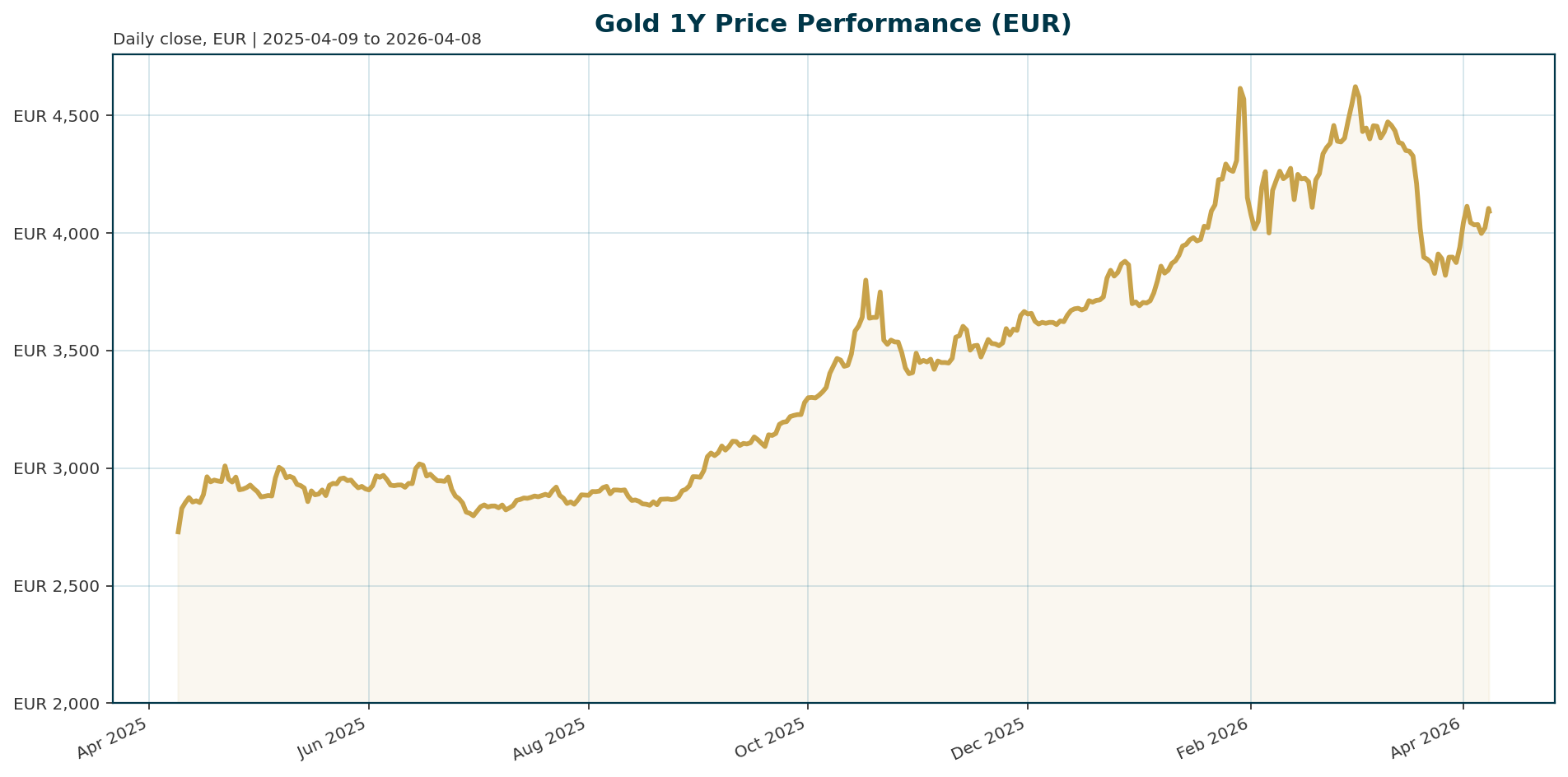

| Current Price | 4,086.60 | EUR | — |

| 24h Change | +1.75% | — | — |

| 30d Change | -7.73% | — | — |

| 200d Change | +30.02% | — | — |

| 1y Change | +48.38% | — | — |

| All-Time High | 4,688.32 | EUR | -12.69% |

| Market Cap Rank | 39 | — | — |

| BTC Dominance | 56.75% | — | — |

Macro Backdrop

The immediate macro environment presents headwinds for gold as monetary policy tightens. Higher energy prices linked to the Iran conflict have rekindled inflation concerns, prompting a shift in market expectations from anticipated rate cuts to a potential hike by the Federal Reserve [T1][T6]. This shift has driven real yields higher, increasing the opportunity cost of holding nonyielding assets like gold [T1]. Consequently, institutional cash on the sidelines has fallen to record lows, amplifying selling pressure during recent price reversals [T1]. Despite these short-term pressures, the overarching macro environment remains structurally supportive, driven by lofty fiscal deficits and a declining trust in the US dollar [T1][T3].

Investment Thesis

The fundamental thesis for gold remains robust, centered on the metal’s role as a strategic diversifier and a hedge against currency debasement. While current pricing reflects the drag of higher real yields, the long-term value proposition is anchored in the disparity between US gold reserves and federal debt. Today, US gold reserves constitute only approximately 3% of federal debt, a stark contrast to the 51% they represented in the 1940s [T3]. This ratio suggests that gold remains significantly undervalued relative to the fiscal risks facing major economies. Furthermore, the persistent threat of debt servicing costs may compel policymakers to lower rates regardless of inflation data, creating a favorable environment for non-yielding assets [T3].

Bullish Drivers

Several structural and cyclical factors support a bullish outlook for gold. The most significant driver is the massive reallocation of global reserves away from the dollar. BRICS+ nations now hold over 17.4% of global gold reserves, up from 11.2% in 2019, accounting for more than half of all central bank gold purchases between 2020 and 2024 [T2]. A Reuters survey confirms this trend, finding that 73% of central bankers believe the dollar’s reserve share will decrease further and that 43% plan to increase gold holdings—a record high [T2][T4]. Geopolitical risk is also a primary catalyst, with tensions now viewed as the top global risk by nearly 70% of surveyed central banks [T4]. Additionally, physical repatriation trends are accelerating, such as France selling 129 tonnes of gold from the NY Fed to book a 13 billion euro capital gain and repatriating all assets domestically [T8].

Relative Positioning vs Bitcoin and Ethereum

Gold currently faces competition from risk-on assets, particularly Bitcoin, which holds a dominance of 56.75% [T1]. The current hawkish monetary stance favors income-generating alternatives like government bonds over non-yielding assets, creating a headwind for gold relative to crypto assets [T1][T6]. In a risk-off environment, gold typically outperforms Bitcoin and Ethereum, but the current market pricing in higher rates suggests a temporary divergence where equities and crypto may lead. However, the structural reserve diversification by central banks provides a floor that may eventually decouple gold from the volatility of the crypto market.

Scenario Framework

Scenario 1: Hawkish Stagflation (Base Case) The Fed maintains high borrowing costs to combat persistent inflation. Real yields remain elevated, capping gold’s upside and keeping prices in a consolidation phase below the 2026 ATH of 4,688.32 EUR [T1][T6].

Scenario 2: Debt Crisis Pivot (Bullish) Policymakers are compelled to cut rates to alleviate the severe strain of debt servicing, regardless of inflation metrics. This shift would trigger a sharp rally in gold as the opportunity cost of holding the metal collapses [T3].

Scenario 3: Geopolitical Shock (Catalyst) Escalation of the Middle East conflict leads to a flight-to-safety event. Gold prices spike, potentially breaking the current resistance levels and reclaiming the ATH as investors seek safe-haven assets [T4][T6].

Valuation Discussion

Gold is currently trading at a discount to its recent highs, offering a value entry point following a -12.69% pullback from the January ATH. However, valuation is highly sensitive to real yield movements. While the spot price of 4,086.60 EUR appears elevated on a nominal basis, the structural support from central bank buying and the low reserve-to-debt ratio suggests the metal is not overvalued relative to the systemic risks it mitigates. The current pullback may represent a profit opportunity as debt risks continue to grow [T3].

Risks

The primary risks to the bullish thesis are short-term macroeconomic. A sustained rise in real yields could trigger a deeper correction, as seen in the recent sell-off [T1]. Additionally, a stronger US dollar makes gold more expensive for international buyers, potentially dampening demand. The hawkish stance of major central banks threatens the appeal of gold and mining equities, creating new vulnerabilities in the sector [T6]. Finally, geopolitical events, while bullish for gold in the long run, can cause immediate volatility that may test the metal’s downside resilience.

Appendix

Sources

- Gold’s demand drivers ‘should once again reassert themselves’ after Iran war shock fades – Merrill’s Avioli – Shanghai Metals Market [T1]

- BRICS+ nations hold over 17% of world’s gold reserves: report – Mining.com [T2]

- Gold pullback offers profit opportunity as debt risks grow, says analyst – CryptoRank [T3]

- Central banks’ concern over rising geopolitical tensions surges, survey shows – Reuters [T4]

- Central banks remain net gold buyers in February despite rising geopolitical uncertainty – KITCO [T5]

- Gold mining companies encounter dual pressures as broader economic factors turn unfavorable for their operations – Bitget [T6]

- Turkey’s Economy Was Winning. Then The Iran War Came – Forbes [T7]

- France pulled all its gold from the NY Fed — and made $15 billion doing it – Boing Boing [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. The analysis is based on data available as of 2026-04-08.

Important Note / Wichtiger Hinweis:

EN: This report may contain AI-assisted analysis or be generated entirely by AI, which processes market data from publicly available sources for which altii accepts no responsibility for its accuracy. We strongly advise against using this report as a basis for investment decisions.

DE: Dieser Bericht kann KI-gestützte Analysen enthalten oder vollständig von KI erstellt worden sein, die Marktdaten aus öffentlich zugänglichen Quellen verarbeitet, für deren Richtigkeit altii keine Verantwortung übernimmt. Wir raten dringend davon ab, diesen Bericht als Grundlage für Anlageentscheidungen zu verwenden.