UK equities are unloved, undervalued and high yielding; an ideal scenario for stock pickers, argues Sue Noffke, Head of UK Equities at Schroders.

Whatever the opposite of a sweet spot is, many investors think UK equities are currently in one. With Brexit still unresolved, some have put the market in the “too difficult” basket. While it is understandable to fear uncertainty, as stock pickers we embrace the mis-priced opportunities created by it.

The global nature of the market means that international developments often set the tone for UK equities, and following the trough in the wake of the global financial crisis (GFC) of 2007/08 they’ve had a good run, as have equities generally. However, Brexit has still loomed large and been a drag on returns.

UK equities have underperformed global equities since the EU referendum. As a consequence, relative to global equities they are now the most lowly valued for decades. The market also looks very attractive in absolute terms: its current dividend yield is significantly in excess of the long-term average yield.

1. Unloved

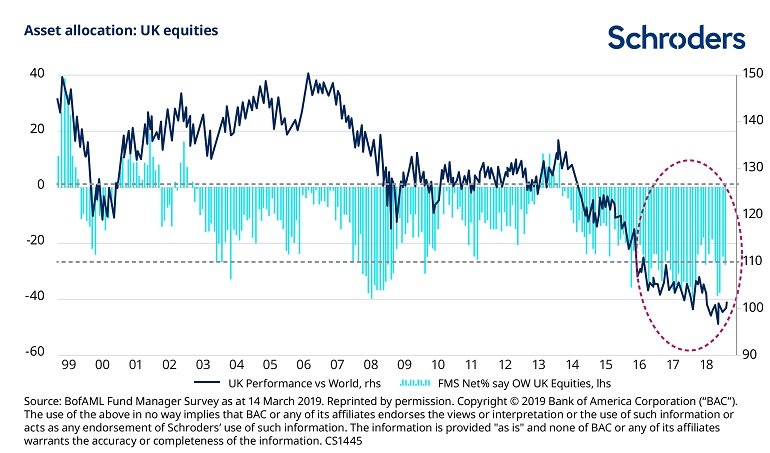

The negativity of international investors towards UK equities is entrenched – global fund managers have been “underweight” the UK for three years, according to the Bank of America Merrill Lynch’s global fund manager survey (see chart, below). Investors are said to be underweight an asset class when they are allocating less capital to it than would normally be the case.

As patient investors, we are often interested in how corporate investors are behaving since we share their long-term mentality. Overseas companies (and private equity) buyers are capitalising on the relative valuation opportunity of UK equities, and sterling weakness.

To cite two recent examples, Coca Cola has acquired the Costa Coffee chain from FTSE 100 group Whitbread, while shareholders in mid-cap speciality pharmaceutical company BTG have approved a bid from Boston Scientific.

Costa Coffee generates the bulk of its profits from the UK, although it has a fast growing international franchise business. In contrast, 90% of BTG’s revenues derive from customers based in the US1. To our minds the bids for these assets underline the indiscriminate negativity towards UK equities – many investors have sold ALL UK equities, both their domestically and internationally focused ones. Remember the UK equity market derives more than two thirds of its revenues from overseas.

Share buybacks2 by companies are another interesting theme. It is, perhaps, no coincidence that Whitbread has proceeded to use the larger part of the the Costa sale proceeds to repurchase stock.

Whitbread has joined a number of other UK quoted companies which have either recently initiated, or extended share buyback programmes, including Standard Chartered and UK-focused peer Lloyds Banking.

It seems to us that many UK corporates see their own shares as undervalued, so are sending another valuable signal.

2. Undervalued

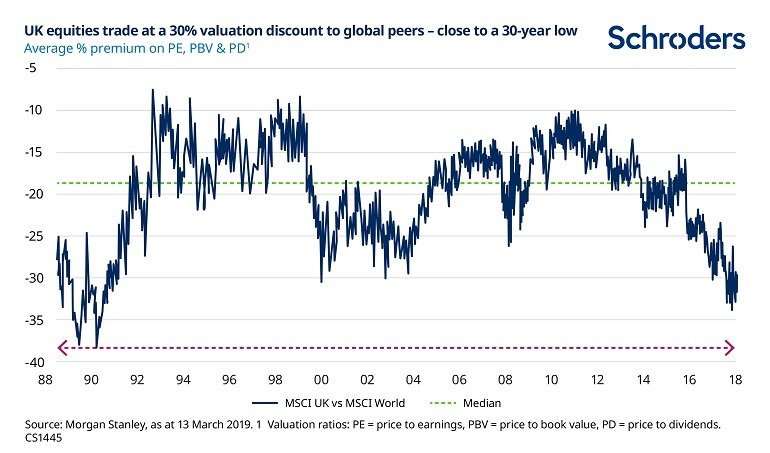

Indeed, valuations reflect the degree to which investors have shunned UK equities. The chart below tracks the market’s valuation discount versus global equities based on the average of three metrics. The metrics used are the price-to-book value (PBV) ratio and price-to-earnings (PE) and price-to-dividends (PD) ratios.

All valuation metrics have their strengths and weaknesses, so combining three reduces the risk of distortions (see the end of the article for a description of these metrics).

Based on this analysis, UK equities are trading at a 30% valuation discount to global peers, close to their 30-year lows. While it is likely to persist until there is some form of clarity over the terms of any Brexit deal, the valuation gap provides an attractive entry point for investors with long time horizons.

Please be aware the value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

The valuation of domestically-focused equities is particularly attractive, and consequently we have been increasing exposures to this area of the market. The uncertainty created by Brexit has driven a slowdown in the UK economy since the EU referendum (albeit, by less than feared), while the global economy has held up well.

Associated UK political uncertainty is further weighing on valuations, and might continue to do so given the relatively high probability of either a leadership election or a UK general election in 2019.

3. Attractive yield

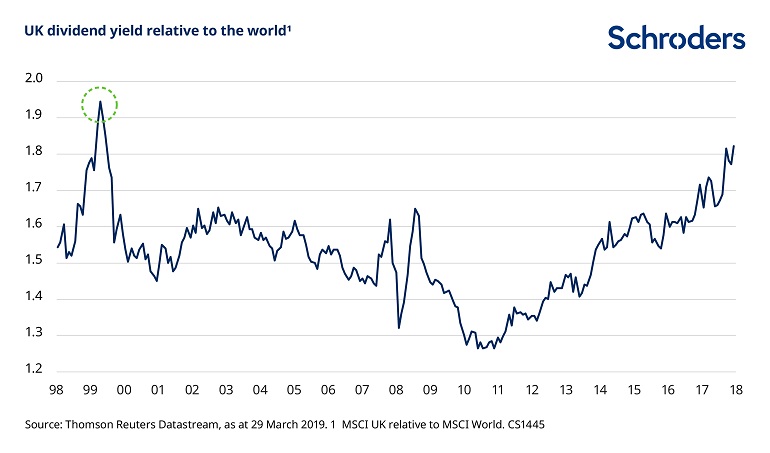

Over the past 30 years the dividend yield of the UK equity market, relative to the rest of the world has only been higher during the 1991 recession and at the peak of the technology media and telecoms (TMT) bubble (see chart, below).

Past performance is not a guide to future performance and may not be repeated.

Past performance is not a guide to future performance and may not be repeated.

In absolute terms, the UK equity market is currently yielding c. 4.5% (MSCI UK index), which compares very favourably to the average dividend yield over the past 30 years of 3.5%. For yields to revert back to their long-term average, either the market has to rise or bad news needs to arrive soon and companies cut payments. They would need to cut by a good margin more than they did following the GFC and ensuing global recession – is this likely?

Following the GFC, UK dividends fell by 15% over two years on a cumulative basis, and that includes the effect of BP suspending its dividend following the Deepwater Horizon disaster in the Gulf of Mexico. We don’t believe we are on the cusp of a recession like the one which followed the GFC. Despite some recent high profile and material dividend cuts from Vodafone and Marks & Spencer, overall we still believe that the market’s dividend payment will continue to rise.

If we do experience a recession in the near term, we would expect it to be local to the UK (possibly the result of a disordely Brexit) rather than a global one, although we are in the latter stages of the economic cycle. This gives us a degree of comfort that the UK equity market’s yield is sustainable as the large majority of UK stock market dividends derive from overseas.

The charts and data highlighted help put the opportunities within UK equities into a broader context. In light of these conditions it is perhaps unsurprising that our allocation to overseas equities is currently at the lower end of its historical range.

As stock pickers we see plenty of opportunities within the UK – across all parts of the market, large as well as small and mid-sized companies – which could help build portfolios capable of generating superior long-term returns.

Investments concentrated in a limited number of geographical regions can be subjected to large changes in value which may adversely impact the performance of the fund.

Equity [company] prices fluctuate daily, based on many factors including general, economic, industry or company news.

Please be aware the value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

1) See page 124 of BTG’s 2018 annual report and accounts, at: https://btgplc.com/BTG/media/BTG/pdf/annual-report-and-accounts-2018.pdf

2) Share buybacks are where a company repurchases its own shares in the open market. Similar to dividends, it is a way for companies to return cash to shareholders.

This article has first been published on schroders.com.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.