It’s the first time we have lowered our expectations for global growth since 2016. Schroders’ Economics Team provides the reasons why.

Although growth remains strong, there are a number of factors that we believe will have a negative impact on global growth in both 2018 and 2019.

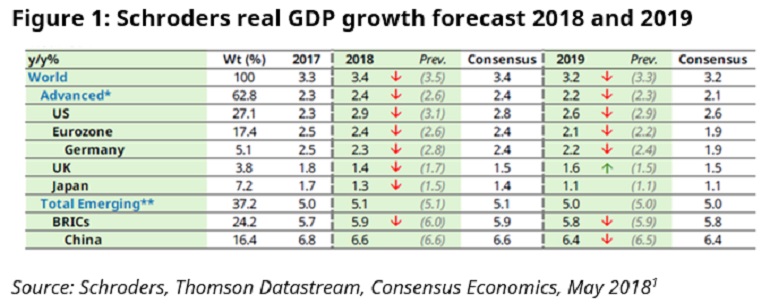

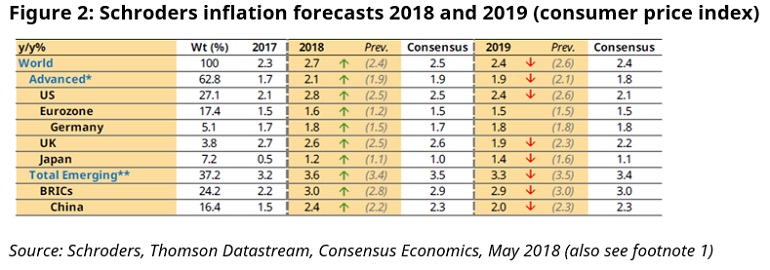

As a result, we have downgraded our forecast for the first time in nearly two years: from 3.5% to 3.4% in 2018 and from 3.3% to 3.2% in 2019. Meanwhile, global inflation is expected to be higher and we have raised our forecast for 2018 from 2.4% to 2.7% with implications for monetary policy throughout the world.

A weak start to the year

The year did not get off to a particularly strong start in most economies. In Europe, severe winter weather, a related outbreak of influenza, transportation strikes and the timing of Easter seem to have weighed on growth figures.

Meanwhile, in the US growth also weakened. It had received a one-off boost at the end of last year from post-hurricane rebuilding and replacement spending, but as the impact of this faded, growth pulled back in the first quarter of 2018.

Elsewhere, some of the emerging market economies also saw a softening in first quarter data, notably Russia and Brazil.

While many of these factors should now fade, helping activity to normalise in the current quarter, we are cognisant that leading indicators are providing mixed signals as to whether growth will rebound in Q2. In addition, rising oil prices and trade tensions are likely to contribute to an easing of growth.

Higher oil prices

Oil prices have risen meaningfully this year so far thanks to OPEC production cuts and the likely re-imposition of sanctions on Iran following President Trump’s termination of the nuclear deal. This will have an impact on consumer spending.

In the US, for example, the rise in oil prices will cost the consumer about $60 billion. Of course, consumers are already saving $120 billion thanks to President Trump’s tax cuts, but this means that half of their savings will go toward paying for costlier gasoline. For those in the lowest 20% income bracket, higher gasoline prices more than offset the gain from tax cuts. Overall, real consumer spending is therefore likely to be lower as a result.

The key question will be whether workers can gain some of this back through higher wages. So far wages have remained remarkably subdued but some recent data suggest that this could be changing.

Among the large emerging markets, Indian growth is also expected to suffer in an environment of rising oil prices given its oil import bill while Russia stands to gain, although the benefit will be limited by the impact of US sanctions.

Tense trade talks

As a brief recap, the US and China are currently threatening one another with $50 billion in tariffs. Though a small share of either country’s trade, let alone GDP (less than half of one percent for China), the growth impact could be larger as the dispute is unlikely to end with one round of tariffs.

The uncertainty over future trade relations is likely to act as a drag on business decisions to hire and invest, particularly for exporters. This, in combination with certain policy measures, prompts a downgrade to Chinese growth in 2019 (from 6.5% to 6.4%) which in turn accounts for some of the modest lowering of global growth expectations in 2019.

Rising inflation

Higher oil prices will push up inflation on a global basis. Even in the US, we expect core inflation to move higher over the next two years.

In Europe, the combination of higher energy prices and a lower US dollar/euro exchange rate means inflation will rise here too.

In the emerging markets, inflation remains low by historical standards but is beginning to creep upwards in Brazil, India and Russia.

What does this mean for monetary policy?

In most of the developed world, we expect monetary policy to tighten. In the US, we see the Federal Reserve hiking interest rates three more times this year and two in the next, such that the Fed funds rate reaches 3% by mid-2019.

The European Central Bank (ECB) is expected to end quantitative easing in Q4 this year and raise rates three times in 2019, ending the era of negative policy rates in the eurozone. The Bank of England is likely to remain on hold until November when there should be greater clarity on the outcome of the Brexit negotiations.

In the emerging markets, we expect Brazil’s central bank to avoid further easing and begin a gradual hiking cycle late in 2019. In India we anticipate a slightly faster tightening given the economy’s reliance on oil. We expect two hikes this year, with the first likely in June, to take rates to 6.5%, with two further hikes in 2019.

In contrast, lower inflation and liquidity concerns means that China heads the other way, with the People’s Bank of China (PBoC) easing the reserve requirement ratio (RRR). This sets the minimum amount of reserves that must be held by banks in the country and is used by the central bank as a way to fight inflation. A rate cut in China may also be warranted in 2019 as growth slows further amid a drag on sentiment from trade tensions.

Against this backdrop the US dollar is expected to strengthen further in the near term before weakening in 2019 as central banks outside the US begin to tighten.

Expansion for now, but the forecast takes a stagflationary turn

We continue to expect another year of expansion for the world economy, but at the margin the forecast has moved in more stagflationary direction with more inflation and less growth than before. This is a result of higher oil prices and the increased threat of trade wars.

This is a summary version of the Schroders Economic and Strategy Viewpoint for June 2018.

1. Market data as at 24/05/2018. Previous forecast refers to February 2018. Consensus inflation numbers for emerging markets is for end of period and not directly comparable. Advanced markets: Australia, Canada, Denmark, Euro area, Israel, New Zealand, Singapore, Sweden, Switzerland, UK, US. Emerging markets: Argentina, Brazil, Chile, Colombia, Mexico, Peru, China, India, Indonesia, Malaysia, Philippines, South Korea, Russia, Czech Republic, Hungary, Poland, Romania, Turkey, Ukraine, Bulgaria, Croatia, Latvia, Lithuania.

This article has first been published on schroders.com.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.