Tightening capacity and recent underinvestment are among the factors pointing to a sustained increase in corporate spending, show Martin Skanberg, Fund Manager for European Equities, and Stephen Shields, Research Analyst and Fund Manager for European Equities, both Schroders.

Global capital expenditure (capex) is budgeted to grow by 8.3% in 2018, our analysis shows. This marks a significant turnaround; it follows a 0.1% rise in 2017 and a 8.9% contraction in 2016.

These figures refer to capex by listed companies, so they exclude planned spending by unlisted firms and the state. However, combined with our top-down analysis of the drivers of capex, we are confident that they are directionally correct.

What do we mean by capex?

Capex refers to spending on investments or new projects, for example acquiring or upgrading assets such as equipment or property. The point of such spending is to increase a company’s production capacity. Capex therefore tends to pick up at times when companies are confident there will be growing demand for their products, and so reflects their confidence in the strength of the economy.

Why has capex been weak in recent years?

Capex stagnated in the wake of the global financial crisis (GFC), with companies reluctant to invest at a time when economies worldwide were suffering recession. More recently, the end of the commodity boom was another significant factor causing capex to decline, since oil & gas and mining companies have historically made up a significant proportion of total corporate spending.

Europe in particular has seen a slow recovery from the GFC, with economic expansion only really taking hold in the last 12 months.

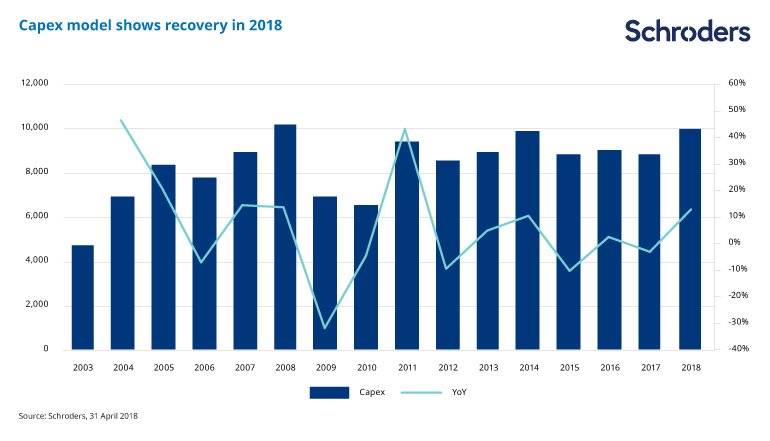

The chart below shows our capex model and indicates that the past few years have seen a multi-year downturn in capex – the most protracted for several decades. The 2014-16 peak-to-trough contraction in capex across all the companies in the model was 15.8%, or $450 billion.

Our model aggregates consensus capex forecasts for thousands of companies across various different end-markets. The 2018 forecasts, showing an expected 8.3% capex increase, incorporate the guidance released by companies at the full year results. With capital budgets typically set months in advance, these should be reasonably accurate.

European capacity utilisation nearing peak levels

An important part of why capex is expected to pick up this year is that many industries are already close to full capacity. The chart below shows the capacity utilisation rate in Europe. This fell dramatically in the wake of the GFC and then remained at relatively low levels during the eurozone sovereign debt crisis. However, the rate is now close to its all-time high.

This indicates that factories in the eurozone are almost as close to capacity as they have ever been. Companies will therefore need to increase capacity and/or efficiency if they want to increase the amount they produce.

There are other factors at play too which could see capex increase in the coming years:

- Tighter labour markets: when there is a lot of slack in labour markets companies can hire staff cheaply in order to increase output. However, labour markets are tightening across Europe (i.e unemployment levels are falling). This should encourage more companies to invest in equipment to improve productivity, rather than simply hiring new people.

- Bringing production back onshore: the offshoring wave of the 2000s saw significant manufacturing capacity move from developed markets to emerging markets. This is now partly reversing. With time-to-market a key consideration, many companies now prefer to locate their factories closer to their end markets.

- Increased automation: advances in robotics make it cheaper to run a facility in Europe with high levels of automation. The underinvestment in the years since the GFC also means that many plants or factories are in need of modernisation, again pointing to a revival in capex.

- US tax reforms: the tax cuts enacted in the US are expected to spur greater investment. Some European companies with US exposure will benefit from this too.

A long-term trend

The above are largely factors that we would expect to play out over a period of several years. The pent-up demand from a decade of underinvestment cannot be caught up in an instant. In our view, there is no reason why capex cannot continue to grow in 2019 and 2020, so long as GDP growth remains robust.

We see a capex pick-up as being the next leg in the slow European economic recovery. Greater capital spending by corporates is a sign they are confident that the recovery will be long-lasting. Capex should also help to sustain the recovery, given the prospect that QE could be withdrawn in the fairly near future.

What does this mean for stockpickers?

As active fund managers, it is not enough for us simply to identify general economic or sector trends; we must translate that into selecting specific stocks for our portfolio. We can count on an experienced team of European equity analysts to support this process.

We look for industries where the current investment levels look to be low versus “normalised levels” or where there is a structural reason for capex to increase.

- Automakers are a clear example of a structural need to invest amid the growth of electric and autonomous cars. Our model indicates strong year-on-year growth in capex by the auto and auto parts sector in 2018.

- Utilities are also under pressure to invest as demand for power remains high and environmental concerns push wind, solar and hydro power up the agenda.

- Technology is clearly a fast-growing, high capex sector. Google’s parent company Alphabet announced $7.3 billion of capital spending in Q1 2018 alone, compared to the $13.2 billion the company spent in the whole of 2017. Investment in datacentres and networks is critical for Google to be able to handle heavier use of its services.

- Similarly, telecommunications is an important sector given the need to invest in 5G networks, and a 9% increase is budgeted for 2018.

- Oil & gas is an interesting area to consider: since the oil price plunged, the sector has shrunk from representing 30% of total capex spend to just 20%. We do not expect capex here to return to peak levels but nonetheless our model indicates an 8% increase for 2018 as the industry does need to invest in order to grow and the recent upturn in oil prices supports this.

Companies increasing their capex may in the short-term see returns to shareholders drop or plateau, as capex takes priority over dividends. On the other hand, the companies who build the new plants, re-tool the factories, and produce the new equipment or robotics should be the short-term beneficiaries as spending picks up. Our task is to discover the most attractive mispriced opportunities in order to deliver the best returns we can.

Any references to securities, sectors, regions and/or countries are for illustrative purposes only and should not be construed as advice or a recommendation to buy or sell.

This article has first been published on schroders.com.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.