Key Data Snapshot

| Metric | Value |

|---|---|

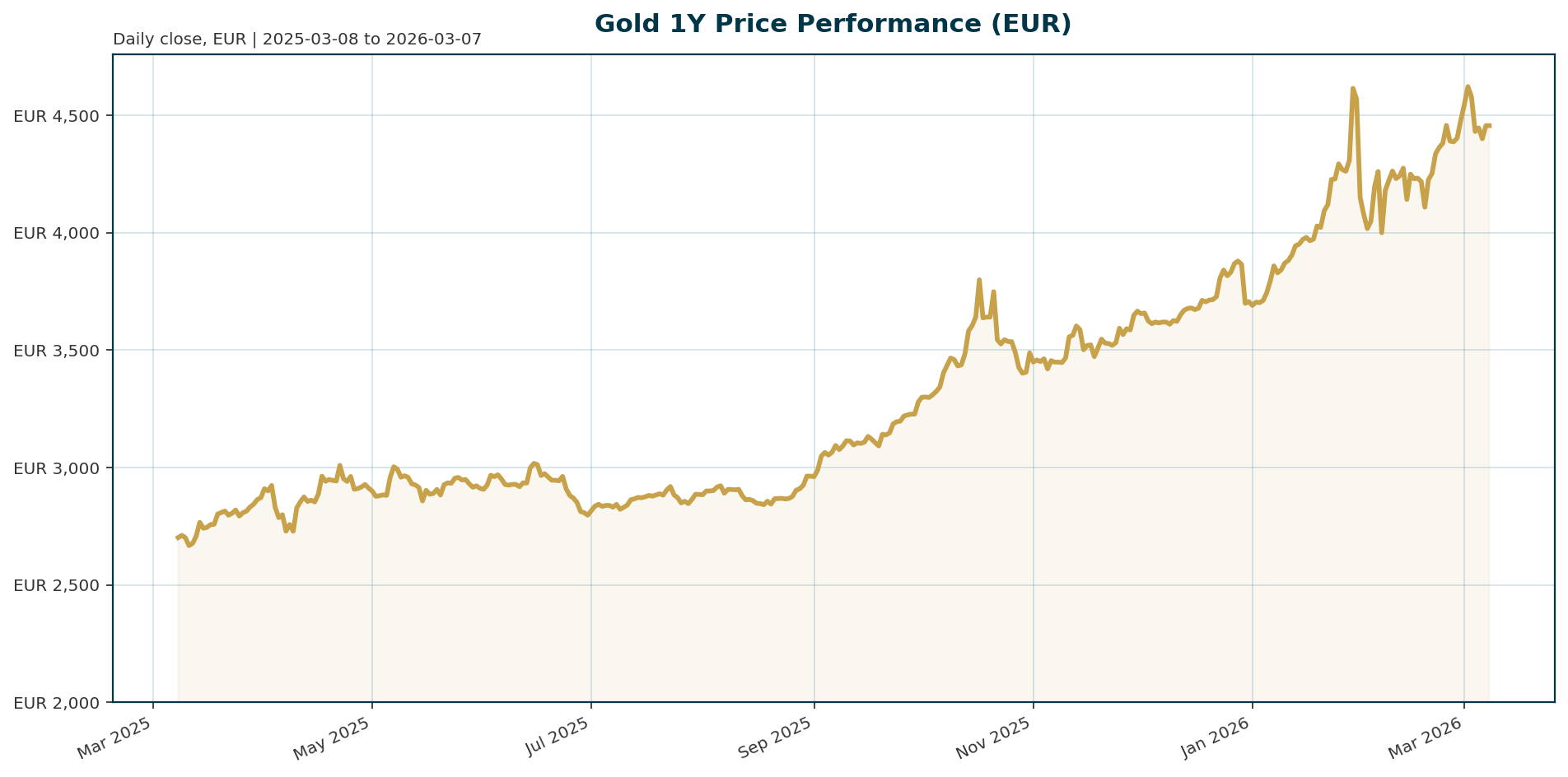

| Current Price (XAU/EUR) | 4,455.87 EUR |

| All-Time High (ATH) | 4,688.32 EUR (Jan 29, 2026) |

| Distance to ATH | -4.97% |

| Year-to-Date Return | +65.45% |

| 7-Day Return | -1.79% |

| 24-Hour Return | -0.15% |

| BTC Dominance | 56.50% |

Macro Backdrop

The current macro environment presents a dichotomy for gold. On one hand, geopolitical tensions are escalating. The outbreak of conflict with Iran and supply-shock implications in the Middle East have fueled fears of higher inflation [T1][T4]. On the other hand, monetary policy is tightening. Traders have pushed expectations of Federal Reserve rate cuts from June to later in the fall, with 43% expecting a target range of 3.25% to 3.5% for the mid-September meeting [T1]. Higher rates make yield-bearing assets more attractive, creating a headwind for gold. Additionally, a stronger dollar, fueled by risk-off sentiment and energy price shocks, is currently putting a lid on further gains [T4][T8].

Investment Thesis

The investment thesis for gold centers on its role as a defensive allocation during periods of structural and geopolitical uncertainty. While gold has historically been a poor inflation hedge—returning negative in 13 of 28 years where inflation exceeded 3%—it stands out as a reliable diversifier during equity stress [T6]. The current rally is supported by a structural shift in demand, specifically the return of official buyers. Central banks, particularly in China, are aggressively diversifying away from the dollar, extending gold buying for a 16th consecutive month [T3]. Furthermore, the tokenization of physical metal is emerging as a new avenue for liquidity and access, signaling a maturation of the gold market beyond traditional physical holdings [T7].

Bullish Drivers

- Geopolitical Escalation: The Middle East conflict serves as a primary catalyst. Analysts suggest that if geopolitical risks rise to a new height, gold could rally to $6,000 by year-end [T4].

- Central Bank Accumulation: China’s central bank increased reserves to 74.22 million ounces, signaling sustained official demand for a non-fiat asset [T3].

- Regional Infrastructure: Singapore is actively positioning itself as a regional gold hub, supported by major banks like JPMorgan and UBS, which will likely increase liquidity and accessibility for Asian investors [T5].

- Tokenization: The tokenization of physical gold offers a practical escape from fiat currency and traditional banking, attracting private investors seeking exposure without physical storage [T7].

Relative Positioning vs Bitcoin and Ethereum

Gold maintains its status as the premier safe-haven asset, distinct from the risk-on nature of Bitcoin and Ethereum. With Bitcoin dominance at 56.50%, the crypto market is currently absorbing significant risk appetite, which can pressure gold as investors rotate into higher-yielding or higher-risk assets [Data]. However, historical data indicates that gold tends to rise when equities perform terribly. Over a five-year horizon since 1970, gold has always been higher than five years prior when the S&P 500 has declined [T8]. In a severe equity downturn, gold is likely to outperform Bitcoin and Ethereum as the primary store of value.

Scenario Framework

- Bull Case (2026 Q3): Geopolitical tensions escalate significantly, triggering a risk-off rush. The Fed delays cuts further due to sticky inflation. Gold retests and breaks its ATH, targeting 6,000 EUR [T4].

- Base Case (2026 Q3): Conflict remains contained but persistent. The Fed cuts rates in September as inflation expectations moderate. Gold consolidates between 4,500 and 4,700 EUR.

- Bear Case (2026 Q3): A peace deal is reached, and the Fed cuts rates in June. The dollar strengthens aggressively. Gold tests support levels near 4,200 EUR.

Valuation Discussion

Valuation is currently stretched relative to historical averages. The 65.45% year-to-date gain reflects a premium for current geopolitical risk. Historically, gold has underperformed bonds and stocks in normal inflationary environments, with a real annualized return of only 1.3% since 1900 [T6]. However, the post-1971 era has been more favorable, with a real return of 4.7%. The current price action suggests the market is pricing in a “new regime” where structural demand from central banks and tokenization justifies a higher multiple than historical inflation periods.

Risks

- Higher Real Yields: If inflation remains persistent due to oil shocks, central banks may keep rates higher for longer, increasing the opportunity cost of holding gold [T1].

- Supply Shock: Poland’s proposal to sell gold reserves to fund defense spending introduces a potential short-term supply-side risk to the market, though legal hurdles remain [T2].

- Dollar Strength: A strong dollar acts as a direct headwind for gold denominated in EUR, as it makes gold more expensive for foreign buyers [T4][T8].

Appendix

Sources

- Gold Prices Aren’t Doing What You’d Expect. Here’s Why Experts Say That’s Happening. – Investopedia [T1]

- Polish central bank chief weighs gold sales to fund defense – Mining.com [T2]

- China’s central bank extends gold buying to 16th month – Mining.com [T3]

- Gold Eyes $6,000 if Middle East Conflict Escalates – TradingView [T4]

- Singapore taps JPMorgan, UBS to push regional gold hub ambition – Mining.com [T5]

- On ignoring geopolitics, buying bubbles and hoarding gold – Financial Times [T6]

- Schiff on Kitco News: Tokenization Signals a New Era for Gold – SchiffGold.com [T7]

- Gold bulls say broader rally is intact despite investors’ dash for cash – KITCO [T8]

Disclaimer

This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed herein are those of the AI assistant and do not reflect the official positions of any financial institution. Past performance is not indicative of future results. Readers should conduct their own due diligence before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.