Key Data Snapshot

| Metric | Value |

|---|---|

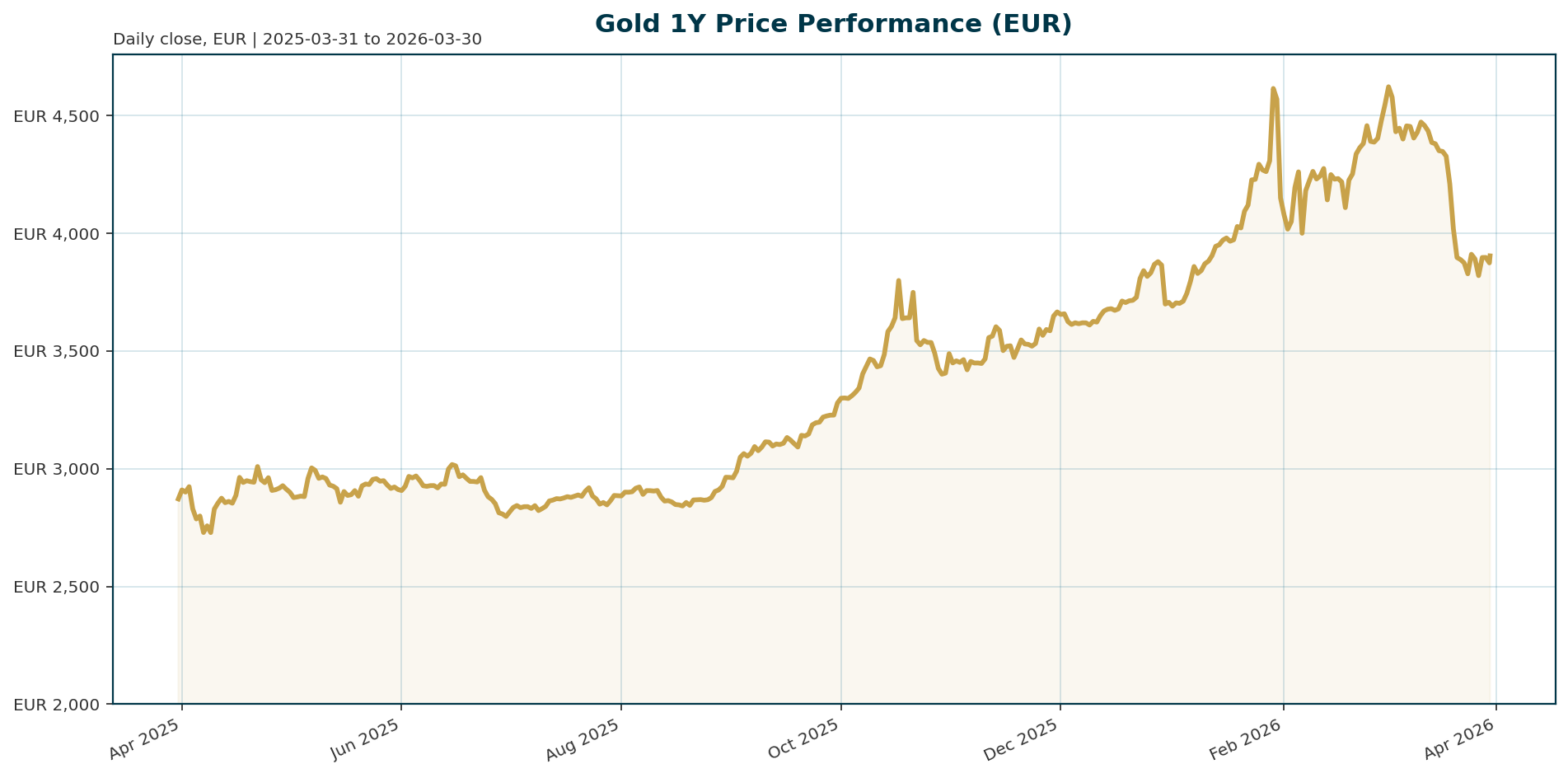

| Current Price (XAU/EUR) | 3,904.29 |

| 24h Change | +0.29% |

| 7d Change | +3.04% |

| 30d Change | -13.03% |

| 1Y Change | +35.96% |

| All-Time High (ATH) | 4,688.32 (Jan 29, 2026) |

| ATH Change | -16.55% |

| Global Central Bank Reserves | $4.3+ trillion (WGC) |

| WGC 2026 Forecast (Demand) | 850 metric tons |

Macro Backdrop

The current macro environment is defined by a structural shift in gold’s primary drivers. The immediate catalyst for the recent pullback is the divergence between nominal interest rates and inflation expectations. As nominal yields on the 10-year Treasury rise faster than expected inflation, real yields have climbed. This environment increases the opportunity cost of holding non-yielding assets like gold [T5].

Geopolitical tensions, specifically the ongoing conflict in the Middle East, have failed to trigger the traditional safe-haven flight into gold. Instead, the market has priced in higher inflation expectations due to energy price shocks, which has led to the removal of June rate cut expectations. This has created a headwind for the metal, as the correlation between geopolitical risk and gold price has temporarily broken down [T1][T5][T8].

Investment Thesis

The investment thesis for gold remains anchored in de-dollarization and reserve diversification. Despite the recent price correction, the fundamental demand structure has not deteriorated. The primary driver has shifted from speculative demand to institutional strategic accumulation. Central banks, representing approximately 20% of total market demand, are aggressively diversifying away from the US dollar due to concerns over currency debasement and asset seizure risks [T3][T6].

Gold is increasingly serving a dual role. It remains a hedge against monetary debasement, but it is also evolving into a liquidity source, or “piggy bank,” for sovereign nations facing energy and defense expenditure crises. This utility supports a floor in prices, as nations are less likely to sell gold to meet immediate operational costs than to trade it for speculative gains [T3][T7].

Bullish Drivers

- Central Bank Accumulation: Central banks remain the most consistent buyers. Poland led the charge in 2026, adding over 80 tonnes to reserves, followed by Kazakhstan and Brazil. The World Gold Council forecasts 850 metric tons of demand for 2026, a figure that remains elevated compared to pre-2022 levels [T1][T4][T8].

- Geopolitical Fragmentation: The seizure of Russian reserves has accelerated the move away from the US dollar. Emerging markets, led by China, are increasing their gold holdings to reduce reliance on dollar-denominated assets, creating a structural demand floor [T1][T3].

- Emerging Market Defense: Turkey holds approximately $135 billion in gold reserves and is actively preparing to utilize these assets for Lira defense mechanisms. This guarantees a baseline level of demand and provides liquidity support for the metal [T2].

- New Market Entrants: Central banks from Guatemala, Indonesia, and Malaysia have re-entered the market, signaling a broadening of the base for gold demand beyond traditional holders [T8].

Relative Positioning vs Bitcoin and Ethereum

Gold is currently decoupling from traditional risk-off correlations that often benefit Bitcoin and Ethereum. During the recent escalation of the Iran conflict, gold failed to act as a safe haven, while crypto assets often exhibit higher beta to specific risk sentiment or technological narratives rather than pure macro hedging [T5][T7].

While Bitcoin and Ethereum may offer asymmetric upside in scenarios of hyperinflation or monetary expansion, gold is currently tethered to the performance of real interest rates. This makes gold less volatile to short-term geopolitical shocks and more sensitive to macroeconomic policy shifts regarding the yield curve. In a de-globalization scenario, gold serves as the liquidity anchor, whereas crypto assets may face regulatory headwinds or liquidity crunches [T5].

Scenario Framework

- Base Case: Real interest rates normalize as inflation expectations stabilize from the energy shock. Central bank buying slows to the WGC forecast of 850 tons. Gold finds a base between 3,800 and 4,200 EUR.

- Bull Case: Geopolitical escalation in the Middle East forces central banks to intervene aggressively, leading to a spike in real yields. This scenario triggers a flight to safety, re-establishing gold as the premier haven asset. Price targets the 2026 ATH at 4,688.32 EUR or higher.

- Bear Case: Turkey utilizes its $135 billion in gold reserves for Lira intervention, creating a sudden supply shock. Simultaneously, real yields spike due to hawkish central bank policy. Margin call selling exacerbates the drop, potentially pushing prices below 3,500 EUR.

Valuation Discussion

The current valuation of XAU/EUR at 3,904.29 reflects a deep discount to the January 2026 all-time high of 4,688.32 EUR, representing a 16.55% drawdown. However, this correction places the asset at a premium to pre-2022 levels, supported by a structural shift in demand.

The “piggy bank” utility of gold—using reserves to pay for energy and defense—suggests a premium on liquidity over purely speculative value. While the market has moved from speculative fervor to a “balanced two-way” market, the fundamental value proposition has strengthened due to the increasing concentration of gold in sovereign balance sheets [T3][T7].

Risks

- Supply Shock Risk: Turkey’s potential conversion of gold reserves into foreign currency to defend the Lira poses a significant supply-side risk. A large-scale drawdown could trigger a sharp price correction [T2].

- Rate Persistence: If the Federal Reserve maintains higher-for-longer policy due to sticky inflation, real yields could remain elevated, suppressing the gold price for an extended period [T5].

- Liquidity Squeezes: The World Gold Council noted that recent price plunges have been partly driven by margin call-related selling. A further increase in leverage could exacerbate volatility [T8].

- De-escalation: If the Middle East conflict de-escalates, the spike in energy prices and associated inflation fears could fade, removing a key support mechanism for gold [T1].

Appendix

Sources

- Central banks’ gold buying momentum carries into 2026 – Bitget [T1]

- Turkey eyes $135 billion gold reserves for lira defense – Mining.com [T2]

- Gold Becomes More Useful As A Piggy Bank Than A Haven – NDTV Profit [T3]

- Central banks’ gold buying momentum carries into 2026 – Mining.com [T4]

- The charts to watch in tech, gold and emerging market stocks as volatility persists – CNBC [T5]

- Singapore looks to become hub for hosting central bank gold – Bitget [T6]

- Gold Becomes More Useful as a Piggy Bank Than a Haven – Bloomberg.com [T7]

- Additional central banks to buy gold on geopolitical risks, WGC says – KITCO [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed are those of the AI assistant and should not be taken as financial guidance.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.