Listen to the summary

Key Data Snapshot

| Asset | Price (EUR) | 7D Change | 1Y Change | ATH (Date) | Key Macro |

|---|---|---|---|---|---|

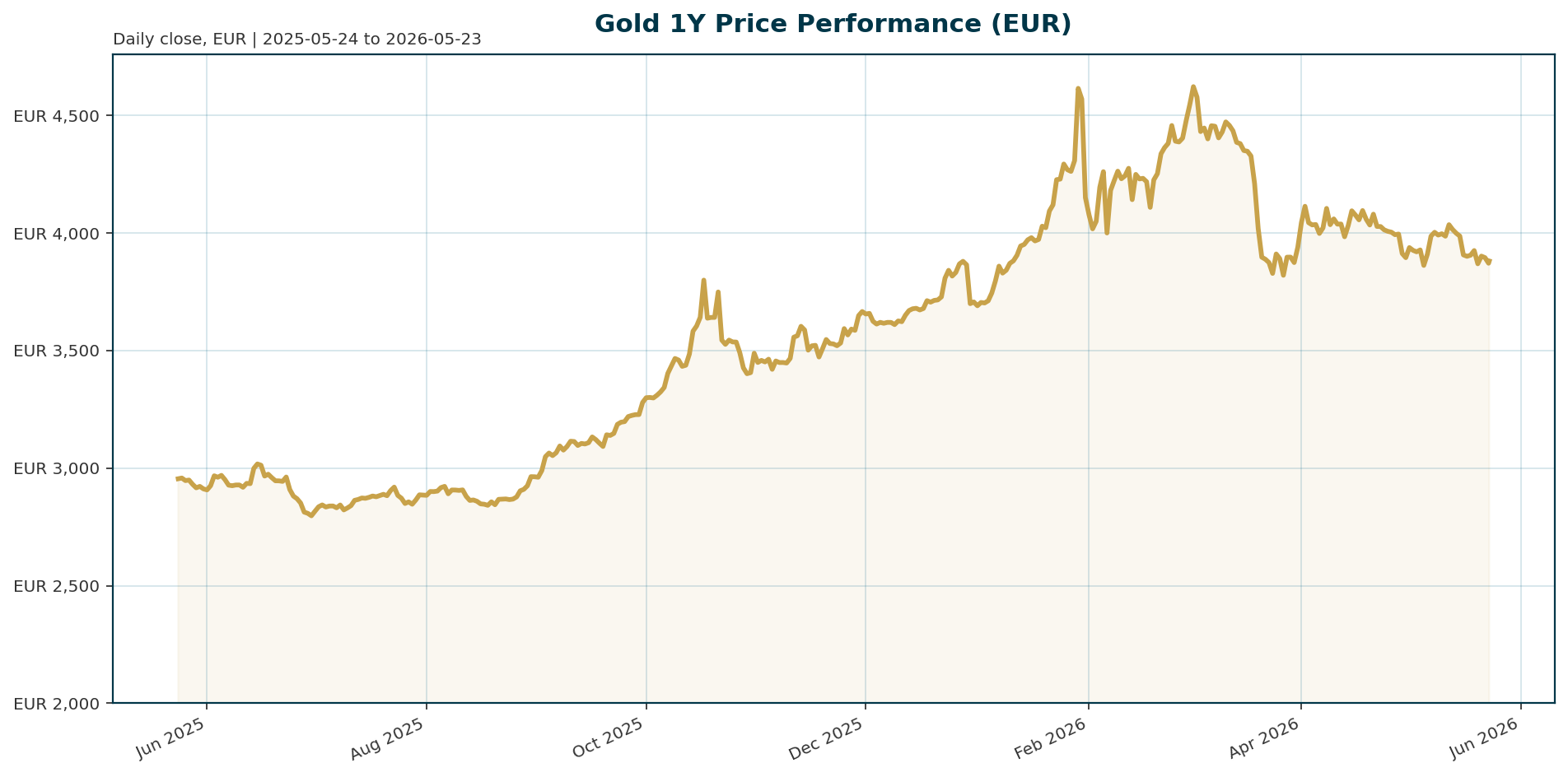

| XAU | 3,880.81 | -0.69% | +32.80% | 4,688.32 (Jan 29, 2026) | Euro 10Y Yield: 3.14% |

Technical Context: Gold is currently trading 17.2% below its January 2026 all-time high. The asset is underperforming risk assets this week, with the Nikkei 225 up 4.15% while Gold slipped 0.69%.

Macro Backdrop

Risk sentiment remains positive, driven by strong equity performance in Japan and Europe, though the backdrop for Gold is mixed. Euro area yields are mixed, with the 10-year yield at 3.14% and the 2-year yield at 2.63%, creating a modest yield floor that weighs on the non-yielding metal. The FX backdrop is also mixed, with EUR/USD at 1.1611.

However, the immediate headwinds for Gold are driven by energy markets and monetary policy. Elevated oil prices above $105/barrel are stoking inflation fears, which has boosted the probability of a Federal Reserve rate hike before year-end to 58% [T2]. This “Higher-for-Longer” narrative is dampening Gold’s appeal. Conversely, the long-term inflationary backdrop is characterized by the “FAITH” acronym (Fed dovishness, anti-immigration, Iran war, tariffs, hyper-valuation), suggesting supply-driven inflation pressures remain a structural concern [T7].

Investment Thesis

The investment thesis for Gold is bifurcated. Short-term, the asset faces headwinds from rising real yields and oil-driven inflation expectations, which increase the probability of Fed tightening. Long-term, the structural bull case remains intact due to persistent inflation and central bank reserve accumulation.

Veteran commodities strategist Jeffrey Currie exemplifies this dichotomy. He is currently short Gold, citing a structural shift where central banks may be forced to sell bullion to pay for energy imports rather than buying it [T3][T6]. However, he maintains a long-term bullish outlook, projecting a pullback to $4,000/oz before a surge towards $10,000/oz once central banks pivot dovish after an energy crisis impacts growth [T3][T6].

Bullish Drivers

- Structural Central Bank Demand: Global central banks are aggressively stockpiling bullion as prices soar. A prime example is Ghana, which has requested large-scale miners to sell 30% of annual output to the central bank, up from 20%, targeting 157 tons by 2028 to rebuild external buffers [T1].

- Inflation Hedge: The “FAITH” macro environment suggests inflation is entrenched. Supply-driven inflation pressures, exacerbated by the Iran war and tariffs, provide a fundamental rationale for holding Gold as a store of value [T7].

- Long-Term Asymmetry: Currie argues Gold is the “most asymmetric trade in modern financial history,” having quietly become the best-performing asset class of the decade as investors chased AI trades while ignoring the physical assets required for that technology [T6].

Relative Positioning vs Bitcoin and Ethereum

Gold is currently underperforming during this specific risk-on phase. With Bitcoin dominance at 58.03%, capital is flowing into crypto assets rather than traditional safe havens. Gold’s 7-day decline of -0.69% contrasts sharply with the Nikkei 225’s 5-day gain of 4.15% and the Nasdaq Composite’s 1-month gain of 6.84%.

This positioning suggests Gold is acting as a “barbell” asset—serving as a safe haven in crises but losing favor to digital assets during periods of economic expansion and equity strength. A potential rotation back into Gold may occur if rate hike fears intensify or if geopolitical tensions flare.

Scenario Framework

- Scenario A (Bearish – ‘Higher-for-Longer’): Oil prices spike above $120/barrel, cementing inflation fears. The Fed hikes rates, and Euro area yields rise. Gold tests support near 3,800 EUR.

- Scenario B (Base – ‘FAITH Inflation’): Inflation remains sticky due to supply shocks. Rates stay high but stable. Gold consolidates in a range between 3,800 EUR and 4,100 EUR.

- Scenario C (Bullish – ‘Energy Crisis Pivot’): The energy crisis forces central banks into forced selling (as seen with Turkey) before eventually pivoting dovish. Gold surges past 4,500 EUR, targeting the $10,000/oz mark [T3][T6].

Valuation Discussion

Gold is currently trading at a discount to its recent highs, sitting 17.2% below the January 2026 ATH of 4,688.32 EUR. This pullback offers a potential entry point for long-term holders. However, the opportunity cost of holding Gold is elevated, with Euro area 10-year yields at 3.14%.

Valuation attractiveness will depend on real yield levels. If inflation remains sticky, real yields will likely stay negative, supporting the Gold price. Conversely, if real yields normalize due to a softening economy, the discount may widen.

Risks

- Monetary Policy Tightening: A 58% probability of a Fed rate hike before year-end poses a significant headwind [T2]. Higher rates increase the opportunity cost of holding non-yielding assets.

- Central Bank Forced Selling: Structural risks exist where central banks, facing energy deficits, may be forced to sell gold reserves to fund imports, removing the structural bid [T3][T6].

- Geopolitical Resolution: A de-escalation in the Middle East conflict could lower oil prices, removing the inflation hedge demand and potentially triggering a sharper correction in Gold [T2][T8].

Appendix

Sources:

- Ghana seeks to buy 30% of gold from miners to boost reserves, central bank – Mining.com [T1]

- Gold set for weekly loss as oil-driven inflation fears boost rate-hike bets – Reuters [T2]

- Jeff Currie sees gold price pullback before $10,000 run – Bitget [T3]

- NY Fed’s Perli says rate control toolkit can navigate lower reserve demand – KITCO [T4]

- RESERVE MANAGEMENT AND THE FED’S SYSTEM OPEN MARKET ACCOUNT: RECENT EXPERIENCE AND INSIGHTS FROM SURVEYS – InsuranceNewsNet [T5]

- Jeff Currie sees gold price pullback before $10,000 run – Mining.com [T6]

- The Case For Real Estate Amid Higher Inflation – Forbes [T7]

- ‘Self-fulfilling’ inflation expectations risk recession – Yahoo Finance Australia [T8]

Disclaimer: This report is AI-generated for informational purposes only and does not constitute investment advice. All data is provided as of 2026-05-23. Please conduct your own due diligence before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.