Listen to the summary

Key Data Snapshot

| Asset | XAU/USD |

|---|---|

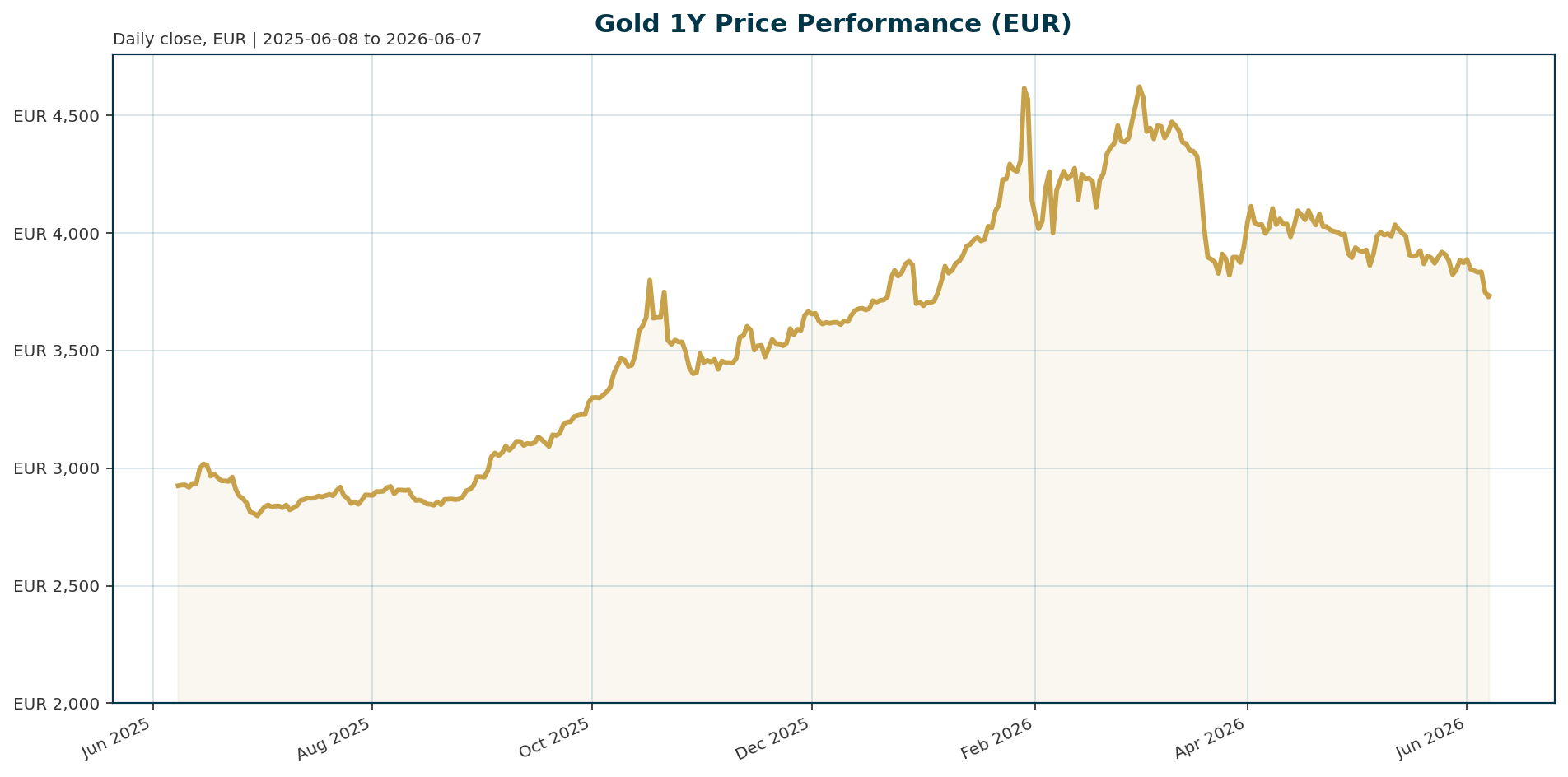

| Current Price (EUR) | 3,733.83 |

| 24h Change | -0.16% |

| 1 Year Change | +27.63% |

| All-Time High (ATH) | 4,688.32 (Jan 2026) |

| Distance to ATH | -20.35% |

| Global Reserve Share | 27% (ECB, 2025) |

| US Treasuries Share | 22% (ECB, 2025) |

Macro Backdrop

Market sentiment remains neutral as investors digest mixed macro signals. The Euro area AAA 10Y yield sits at 3.07%, offering a modest yield premium that weighs on non-yielding gold. The FX backdrop is mixed, with EUR/USD at 1.1623, reflecting recent dollar strength. Notably, regional equity divergences offer a nuanced view: the DAX is the strongest 5-day performer at -0.98%, while the Nasdaq Composite is the weakest at -5.09%. This divergence suggests European investors are rotating into value and safe havens, potentially supporting gold demand in the region.

Investment Thesis

The core thesis for gold rests on a structural shift in global reserve allocation, rather than short-term rate dynamics. The European Central Bank reported that gold has overtaken U.S. Treasuries as the largest share of global official reserves for the first time since 1996, at 27% versus 22% [T1][T3]. While valuation effects from a 60% price surge in 2025 contributed to this share increase, active buying by major central banks—specifically Poland and China—confirms a deliberate strategic pivot away from dollar-denominated assets [T4][T5]. This diversification trend, accelerated by geopolitical fragmentation, positions gold as the premier alternative to fiat liquidity in sovereign balance sheets.

Bullish Drivers

- Central Bank Accumulation: Despite a slowdown from the 1,000+ tonne annual pace of previous years, central banks remain net buyers, targeting 850 tonnes for 2026 [T1][T3]. Poland’s aggressive 14-tonne April purchase and China’s 8-tonne addition highlight continued conviction in the asset [T4].

- Private Sector Demand: The ECB report highlighted Tether as the largest single buyer of gold in 2025, acquiring over 100 tonnes, signaling strong demand from the private sector and stablecoin issuers [T3].

- Fed Policy Constraints: New Fed Chair Kevin Warsh faces a challenging environment with 3.8% inflation that he cannot cut through, creating a “structural trap” that limits the Fed’s ability to pivot to easing [T2].

- Geopolitical Fragmentation: Forces of fragmentation are becoming more pronounced, driving reserve managers to seek non-sovereign assets [T6].

Relative Positioning vs Bitcoin and Ethereum

Gold maintains its structural dominance as the primary reserve asset, holding a 27% share versus 22% for U.S. Treasuries [T1][T3]. While Bitcoin dominance sits at 56.05%, gold remains the bedrock of sovereign wealth. Relative to crypto assets, gold offers superior liquidity and legal recognition for central banks. In the current market environment, the divergence between the DAX (Euro strength) and the Nasdaq (US tech weakness) favors gold, which typically outperforms during periods of global risk aversion where crypto assets often underperform.

Scenario Framework

- Base Case: The Fed maintains its restrictive stance through Q3. Gold consolidates between 3,700 and 3,800 EUR, supported by ongoing central bank buying but capped by elevated Euro area real yields.

- Bull Case: US labor data weakens, forcing the Fed to cut rates. This triggers a retest of the January 2026 ATH at 4,688.32 EUR, driven by a renewed debasement trade and a weaker USD.

- Bear Case: US inflation spikes, causing yields to rise sharply. Gold breaks below the 3,700 EUR support level, potentially testing the 3,500 EUR mark as profit-taking accelerates after the 2025 rally.

Valuation Discussion

Gold is currently trading approximately 20% below its January 2026 ATH of 4,688.32 EUR, offering a margin of safety. However, the high nominal yield environment in the Euro area (3.07% on 10Y) presents an opportunity cost. The bullish argument relies on the assumption that real yields remain suppressed due to sticky inflation expectations. If the Euro area can decouple from US monetary policy tightening, the current valuation level may be attractive relative to the structural shift in reserves.

Risks

- Euro Strength: A sustained rally in EUR/USD above 1.20 would pressure gold prices priced in EUR, as the asset becomes more expensive for foreign buyers.

- Real Yield Spike: If Euro area inflation proves stickier than anticipated, real yields could rise, forcing a repricing of gold as a non-yielding asset.

- Profit Taking: The 60% price surge in 2025 [T5] has created significant unrealized gains. A shift in sentiment towards risk-on could trigger a sharp correction as investors rotate into equities.

Appendix

Sources

- [T1] Central banks see gold as the reserve asset of choice – ECB report – KITCO https://www.kitco.com/news/article/2026-06-02/central-banks-see-gold-reserve-asset-choice-ecb-report

- [T2] Central Banks Picked Gold Over Treasuries. Should You? – GoldSilver https://goldsilver.com/industry-news/goldsilver-news/central-banks-picked-gold-over-treasuries-should-you/

- [T3] Gold overtakes US Treasuries in global reserve shift: ECB – Mining.com https://www.mining.com/gold-overtakes-us-treasuries-in-global-reserve-shift-ecb/

- [T4] Central banks buy net 17 tonnes of gold in April, led by Poland and China – WGC – KITCO https://www.kitco.com/news/article/2026-06-03/central-banks-buy-net-17-tonnes-gold-april-led-poland-and-china-wgc

- [T5] New report reveals gold has overtaken U.S. Treasuries – Yahoo Finance Singapore https://sg.finance.yahoo.com/news/report-reveals-gold-overtaken-u-180925690.html

- [T6] Euro fails to nab big market share from dollar despite erratic US policy, report shows – KITCO https://www.kitco.com/news/off-the-wire/2026-06-02/euro-fails-nab-big-market-share-dollar-despite-erratic-us-policy

- [T7] Gold prices fall the most since March after US jobs report – Laodong.vn https://news.laodong.vn/tien-te-dau-tu/gia-vang-giam-manh-nhat-ke-tu-thang-3-sau-bao-cao-viec-lam-my-1714583.ldo

- [T8] Is the Debasement Trade Over? – Forex Factory https://www.forexfactory.com/news/1402295-is-the-debasement-trade-over

This report is AI-generated for informational purposes only and does not constitute investment advice. Users should conduct their own due diligence before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.