Listen to the summary

Key Data Snapshot

| Metric | Value |

|---|---|

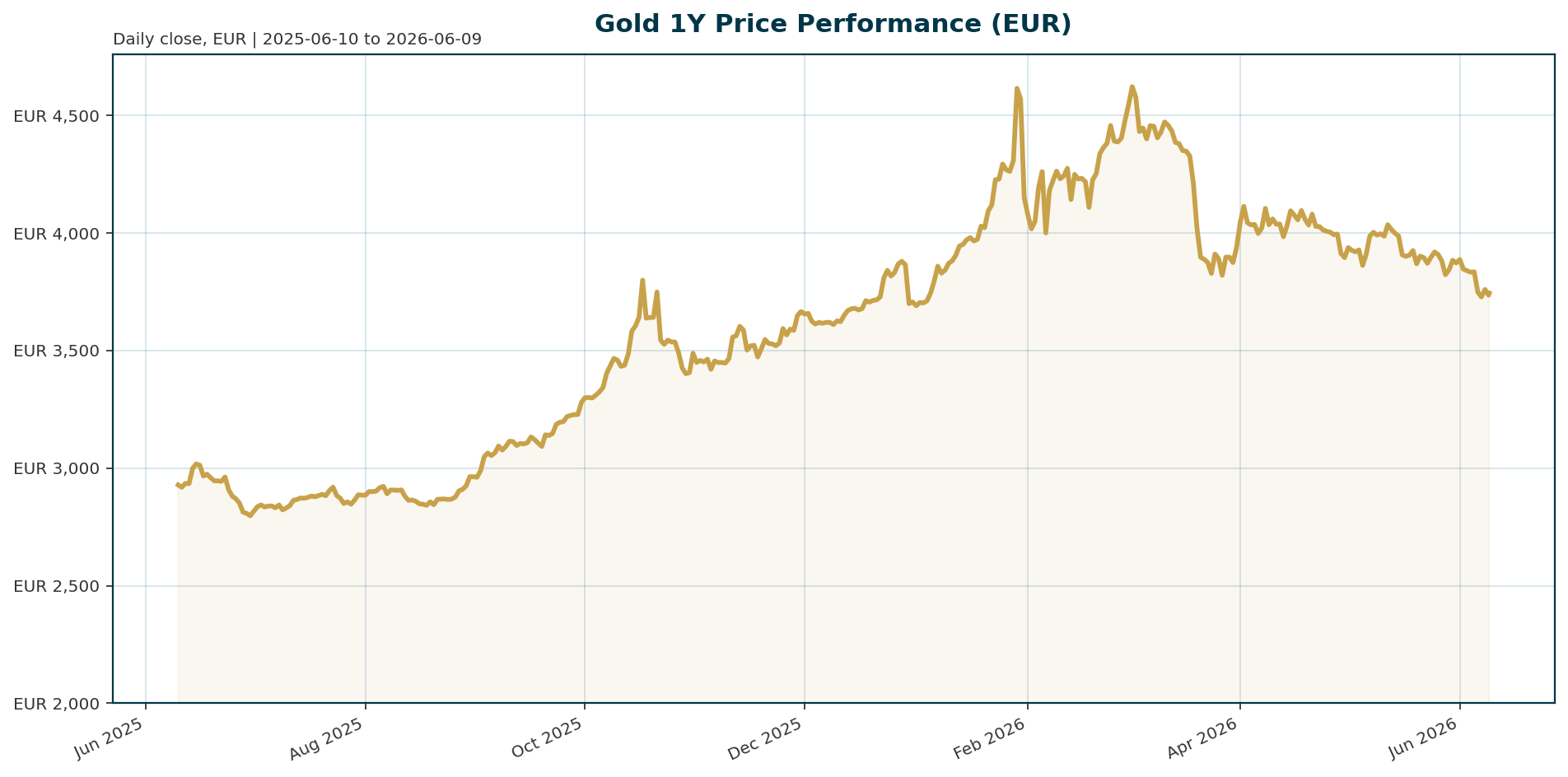

| Current Price (XAU/EUR) | 3,745.11 |

| 7-Day Change | -2.52% |

| 1-Year Change | +28.64% |

| ATH (Jan 2026) | 4,688.32 (-20.10% from current) |

| Euro Area 10Y Yield | 3.09% |

| Real Yield Proxy | -0.11% (3.09% – 3.20% inflation) |

| Global Gold Reserve Share | 27% (vs US Treasuries 22%) |

| Central Bank Net Buy (2025) | 863 tonnes |

Macro Backdrop

Risk sentiment is neutral to negative while rates are mixed and FX markets show divergence. The DACH equity indicators average -2.02% over 5 days versus -3.95% for global indicators, with the Euro Stoxx 50 leading the decline at -0.75%. The Nikkei 225 is the weakest performer at -4.69% over 5 days. In rates, the Euro Area AAA 10Y yield stands at 3.09%, up 2.0 bp over the period. FX markets are mixed, with EUR/USD down 0.59% and EUR/CHF up 0.28%. The dominant weight on gold remains the policy backdrop, with the FedWatch tool showing 96% odds of rates being held unchanged at the upcoming meeting, effectively eliminating near-term easing premiums [T1]. The ECB is expected to raise rates for the first time since 2023 due to Eurozone inflation at 3.2% [T6].

Investment Thesis

The primary thesis for gold is structural rather than cyclical. Gold has overtaken US Treasuries as the world’s second-largest reserve asset, accounting for 27% of global official reserves compared to 22% for US Treasuries [T2][T4]. This shift reflects a deliberate diversification away from the US dollar, accelerated by concerns over the weaponization of dollar assets following the Ukraine conflict [T7]. While traditional safe-haven demand is waning, gold is behaving as a high-beta risk asset, rallying on peace prospects and falling with risk aversion spikes [T8]. The current valuation, supported by a 60% price surge in 2025, is mechanically increasing the share of gold in reserves, but the underlying demand for non-sovereign diversification remains robust.

Bullish Drivers

- Structural Reserve Shift: Central banks continue to accumulate gold despite slowing volumes. The World Gold Council expects roughly 850 tonnes of gold purchases this year, with 95% of surveyed banks indicating they expect global reserves to increase over the next 12 months [T5]. Poland has purchased 45 tonnes year-to-date, while China holds 2,322 tonnes [T5].

- Non-Sovereign Demand: A significant new source of demand has emerged. The ECB report highlighted stablecoin issuer Tether as the largest single buyer of gold in 2025, acquiring more than 100 tonnes [T4][T7].

- Dollar Diversification: Geopolitical fragmentation is driving reserve managers to reduce exposure to dollar-denominated assets. Seventy percent of reserve managers are increasingly concerned about the US political environment, with 31% citing geopolitics as the most important factor in their decisions [T7].

Relative Positioning vs Bitcoin and Ethereum

Gold is currently exhibiting characteristics of a risk asset rather than a traditional safe haven. Following the breakout above $4,500 per ounce, gold has fallen when risk aversion spikes and rallied back when peace deals appear imminent [T8]. This high-beta behavior contrasts with the crypto market, where Bitcoin dominance sits at 56.14%. While both assets are sensitive to global liquidity and risk sentiment, the correlation suggests that capital rotation between risk assets is currently driving price action in gold more than its traditional role as a hedge against inflation or currency debasement.

Scenario Framework

- Base Case (Hawkish Hold): Inflation prints remain sticky, reinforcing the 96% Fed odds of unchanged rates and ECB hikes. Gold consolidates around 3,700–3,800 EUR as real yields remain negative but volatility compresses.

- Bull Case (Soft Landing): CPI prints soften, leading to expectations of rate cuts. Real yields collapse, providing a strong floor for gold. If geopolitical tensions ease, gold could reclaim 4,500 EUR.

- Bear Case (Hard Landing/Conflict): Inflation spikes or a recession looms, prompting aggressive rate hikes. As gold behaves as a risk asset, it could break 3,500 EUR, selling off alongside equities despite the hawkish backdrop.

Valuation Discussion

Gold is trading at a 20.1% discount to its January 2026 ATH of 4,688.32 EUR, following a 60% surge in 2025 [market_data][T8]. The current price of 3,745.11 EUR reflects a complex valuation mix. On one hand, the structural reserve shift (27% share) supports a premium valuation. On the other, the mechanical valuation effect—where rising prices mechanically increase the share of gold in reserves—suggests that a portion of the rally may be disconnected from future physical flows [T2]. With real yields at -0.11%, gold remains attractive relative to bonds, but the “risk asset” label implies that valuation support is contingent on broader market liquidity.

Risks

- Risk-On Rotation: Gold’s high-beta nature means it could sell off sharply if peace talks in the Middle East progress, as it has fallen on risk aversion spikes [T8][T3].

- Policy Tightening: The 96% probability of Fed inaction and the ECB’s expected hike create a headwind for non-yielding assets [T1][T6].

- Geopolitical Stagnation: Ongoing conflict could sustain inflation expectations, forcing central banks to stay hawkish, which pressures gold prices [T3][T6].

Appendix

Sources

- Gold steadies after Friday’s rout as markets brace for CPI and FOMC – KITCO [T1]

- Central banks see gold as the reserve asset of choice – ECB report – KITCO [T2]

- Gold Falls as Geopolitical Tensions Spark Inflation Concerns – WSJ [T3]

- Gold overtakes US Treasuries in global reserve shift: ECB – Mining.com [T4]

- Central banks buy net 17 tonnes of gold in April, led by Poland and China – WGC – KITCO [T5]

- Gold gets no boost from geopolitical conflict, Russia makes outsized precious metals output claims for 2026 – Heraeus – KITCO [T6]

- New report reveals gold has overtaken U.S. Treasuries – Yahoo Finance Singapore [T7]

- Why gold is now more like a risk asset – Axios [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed herein are those of the AI model GLM 4.7 Flash and do not reflect the official positions of any financial institution or entity.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.