Listen to the summary

Key Data Snapshot

| Metric | Value |

|---|---|

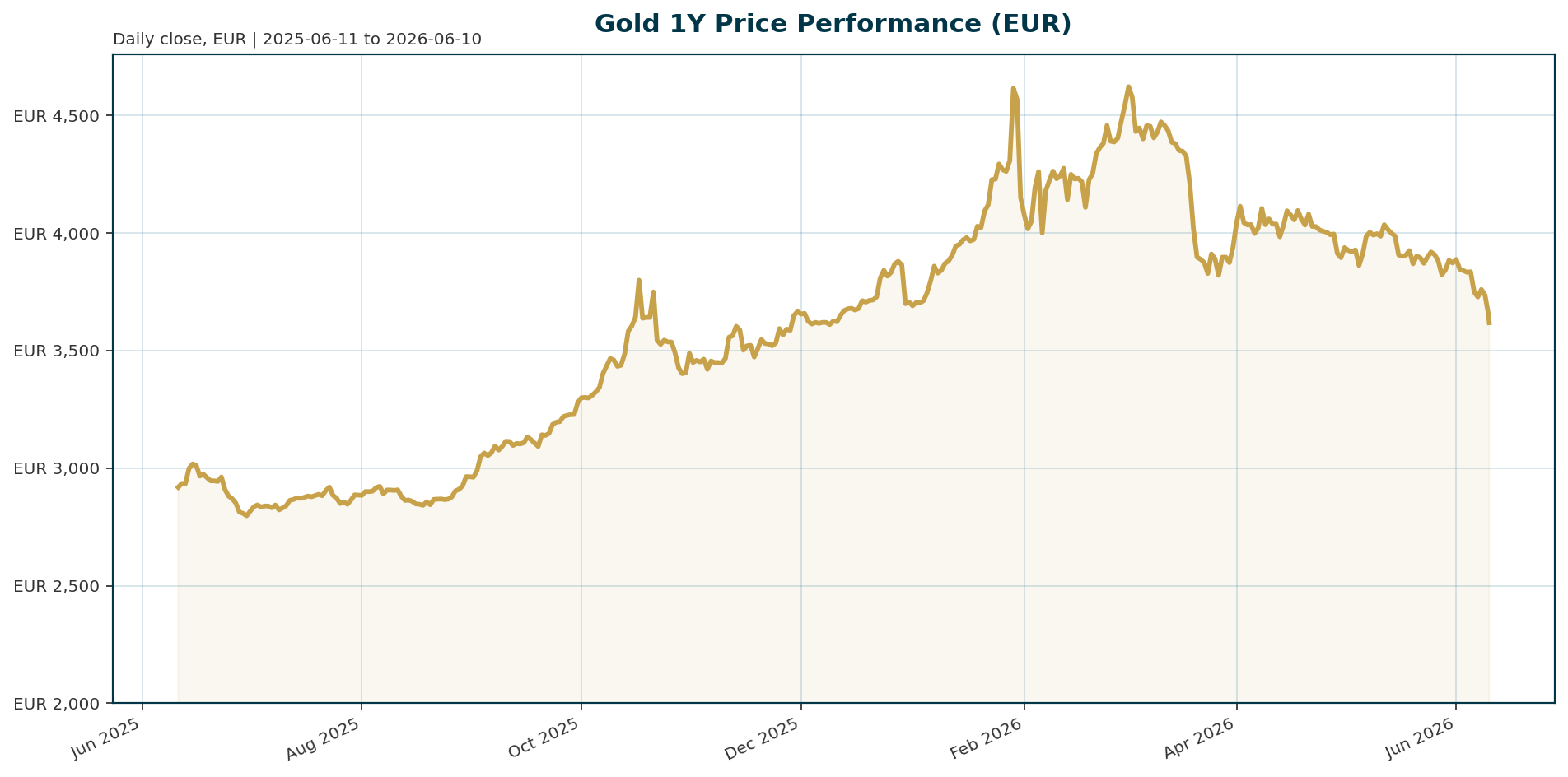

| Current Price (XAU/EUR) | 3,618.31 EUR |

| 30-Day Change | -9.02% |

| 200-Day Change | +2.70% |

| All-Time High (ATH) | 4,688.32 EUR (Jan 29, 2026) |

| 24-Hour Range | 3,613.85 – 3,756.65 EUR |

| EUR/USD | 1.1564 |

| Euro Area AAA 10Y Yield | 3.09% |

| Global Central Bank Gold Reserves | 27% (vs 22% US Treasuries) |

Gold is currently in a correction phase, trading 22.8% below its January 2026 ATH. The recent break of the 200-day moving average indicates a shift in medium-term momentum, with the 24-hour range showing high volatility around this technical level.

Macro Backdrop

Risk sentiment is neutral to negative, characterized by a divergence between regional equity performance and global benchmarks. The Euro Stoxx 50 has outperformed the Nasdaq Composite over the last five days, with the Nasdaq suffering a -4.38% drawdown. This rotation suggests investors are rotating away from high-beta assets.

The rates backdrop is mixed. Euro area AAA 10-year yields sit at 3.09%, a level that creates headwinds for non-yielding gold by increasing the opportunity cost of holding the metal. However, the FX backdrop offers support. The EUR/USD pair is trading at 1.1564, down 0.49% over five days. This weakness in the euro provides a direct tailwind for XAU/EUR pricing, offsetting some of the pressure from elevated nominal yields.

Investment Thesis

The investment thesis for gold rests on a structural shift from an inflation hedge to a primary store of value in a regime of expanding government debt. As governments accumulate liabilities faster than economies can grow, policymakers face difficult choices between fiscal austerity, higher inflation, and debt monetization [T1]. In this environment, gold serves as an asset independent of the financial system and governments.

While short-term price action is driven by cyclical factors such as real yield dynamics and Federal Reserve policy expectations, the underlying thesis remains intact. The “debasement trade” is rebuilding as investors shift from fiat currencies into hard assets to preserve purchasing power [T2]. The market is currently pricing in a complex interplay where structural demand is high, but cyclical headwinds from inflation expectations are weighing on immediate returns.

Bullish Drivers

- Central Bank Diversification: A structural bullish driver is the confirmed shift in reserve composition. The ECB reported that gold now accounts for 27% of global official reserves, surpassing US Treasuries at 22% for the first time since 1996 [T4, T7]. This trend is active, with Poland purchasing 14 tonnes in April alone and China adding 8 tonnes [T6].

- Debt Cycle Dynamics: The rising supply of sovereign debt is eroding the effectiveness of bonds as a store of value. Sprott notes that real yields are becoming difficult to sustain at positive levels, reinforcing gold’s role as a store of value rather than a yield competitor [T2].

- FX Tailwinds: Continued weakness in the EUR/USD pair supports XAU/EUR. As the dollar remains a weaponized currency due to geopolitical tensions, non-US investors are increasingly favoring gold priced in their local currency [T7].

Relative Positioning vs Bitcoin and Ethereum

Gold is currently exhibiting high-beta characteristics, behaving more like a risk asset than a traditional safe haven. Since the Iran war began, gold has fallen when risk aversion spikes and rallied when peace deals appear, mirroring the behavior of the Nasdaq Composite [T7]. This contrasts with the traditional safe-haven narrative.

While Bitcoin and Ethereum are gaining institutional interest, central banks are prioritizing physical gold for reserve diversification over crypto assets. The ECB data confirms that despite the price surge in 2025, central banks chose not to rebalance away from gold, indicating a preference for the established store of value over emerging digital assets [T4, T7].

Scenario Framework

- Bull Case (Base): If the May CPI print comes in below 4.0%, signaling that inflation is abating, real yields could ease. This would likely weaken the dollar and restore the probability of a September Fed rate cut. In this scenario, gold could recover toward the 4,500 EUR area [T5].

- Bear Case (Downside): A CPI reading at or above 4.2% would confirm re-accelerating inflation. This would trigger intensified rate-hike expectations, causing real yields to spike and gold to break below the 3,600 EUR support level [T5].

- Stagflation Trap: If geopolitical tensions (such as US-Iran) spike energy prices while rates remain elevated, real income growth could cap. This mixed-signal environment would create headwinds for gold, as the metal competes with the opportunity cost of high yields [T3].

Valuation Discussion

Current valuation metrics suggest gold is attractive relative to its structural utility, despite its recent drawdown. Gold is trading approximately 300 EUR below the consensus targets of 30 Reuters analysts [T4]. Furthermore, the 22.8% decline from the ATH represents a significant discount to historical highs.

Crucially, central banks are accumulating gold despite the elevated price levels. The fact that they are buying 244 tonnes in Q1 2026 [T2] and maintaining gold as the top reserve asset indicates that the market is undervaluing the metal in terms of its function as a core collateral and store of value. The 2025 price surge of 60% was partially driven by increased buying volume rather than price alone, highlighting the strength of the underlying demand [T7].

Risks

- Real Yield Spike: The primary risk to the thesis is a divergence where inflation expectations rise faster than nominal yields. This would increase the opportunity cost of holding non-yielding gold, putting immediate pressure on prices [T2, T5].

- Geopolitical Escalation: While conflict usually supports gold, a scenario where tensions (like US-Iran) spike oil prices and force central banks to keep rates steady or higher can act as a headwind. This creates a stagflationary environment where gold’s traditional inflation hedge role competes with elevated real yields [T8].

- Fed Policy Error: A hawkish pivot by the Federal Reserve, driven by a resilient labor market, could trigger a sharp correction in all risk assets, including gold [T5].

Appendix

Sources

- Debt cycle points to stronger case for gold price: Sprott – Mining.com [T1]

- Gold and silver will gain as rising debt and inflation reprice bonds and the broader market – Sprott’s Wong – KITCO [T2]

- Gold Price Momentum Amid Geopolitical Headwinds in 2026 – Discovery Alert [T3]

- Central Banks Picked Gold Over Treasuries. Should You? – GoldSilver [T4]

- Gold braces for make-or-break CPI print as rate hike fears mount – KITCO [T5]

- Central banks buy net 17 tonnes of gold in April, led by Poland and China – WGC – KITCO [T6]

- Why gold is now more like a risk asset – Axios [T7]

- Gold Extends Decline as Iran Tensions Rekindle Inflation Fears – Yahoo Finance [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. Readers should conduct their own due diligence before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.