Chinese equities have become an increasingly large presence in our multi-asset portfolios. In the coming years we’re hoping to gain access to the country’s onshore bond market too, says Johanna Kyrklund, Global Head of Multi-Asset Investments at Schroders.

Across multi-asset, China’s presence in our portfolios has been increasing, primarily via the equity markets (see our latest asset allocation views here). However, it is today still uncommon to invest in onshore Chinese government bonds owing to access issues and China’s underrepresentation in the key global bond indices.

This is likely to change over the next few years as the authorities are taking aggressive measures to open the onshore debt markets to foreign investors, which we believe is a necessary step in order to meet regulatory and transparency requirements for inclusion in the major indices.

China maintains two bond markets:

- The Interbank Market (CIBM) is an over-the-counter (OTC) bond market regulated by the People’s Bank of China. 90% of total trading volume is processed via the interbank market.

- The Exchange Market, referring to the Shanghai and Shenzhen stock exchanges which are regulated by the China Securities Regulatory Commission. Only a small percentage is traded on the exchange.

China’s onshore government bond market is now the third largest bond market in the world at about $1.8 trillion. Foreign investors’ market share is around 4% of the China government bond market.

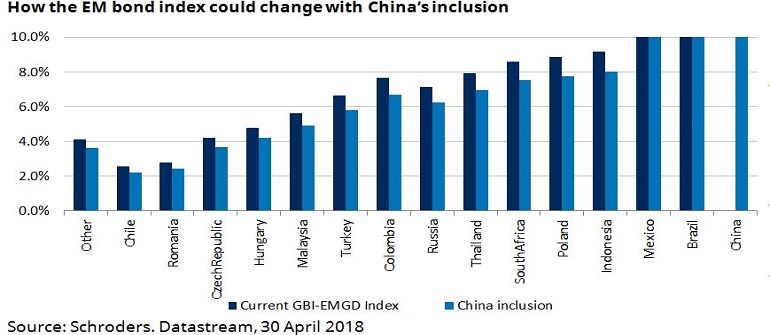

If China is included in the government bond index (JP Morgan Emerging Market Global Diversified index) then its weighting is expected to be capped at 10% due to diversification rules. Other big markets like Brazil and Mexico are also already treated this way. The possible future make up of the index is shown below.

What are the potential opportunities?

- Diversification. Volatility-adjusted returns stand out among other major asset classes. The correlation between Chinese onshore government bonds and major global asset classes has been very low over the past decade. In addition, the more stable Chinese yuan plays a key role in lowering the volatility of Chinese government bonds compared to other emerging market bonds.

- Liquidity. The huge Chinese onshore bond market offers higher liquidity compared with other EM local bond markets. While the average trading volume of onshore government bonds is still lagging that of major developed bond markets, its corporate-bond trading volume is not far behind that of the US.

- Attractive yield. Chinese onshore bonds may continue to offer higher yields than many other major developed market sovereign bonds thanks to China’s independent monetary cycle.

At present, domestic investors are still dominant in the China onshore market and are the biggest contributors to market liquidity; however, the hope is that before long legislation will change, opening the channels for foreign investors to tap into the Chinese bond market.

This article has first been published on schroders.com.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.