Key Data Snapshot

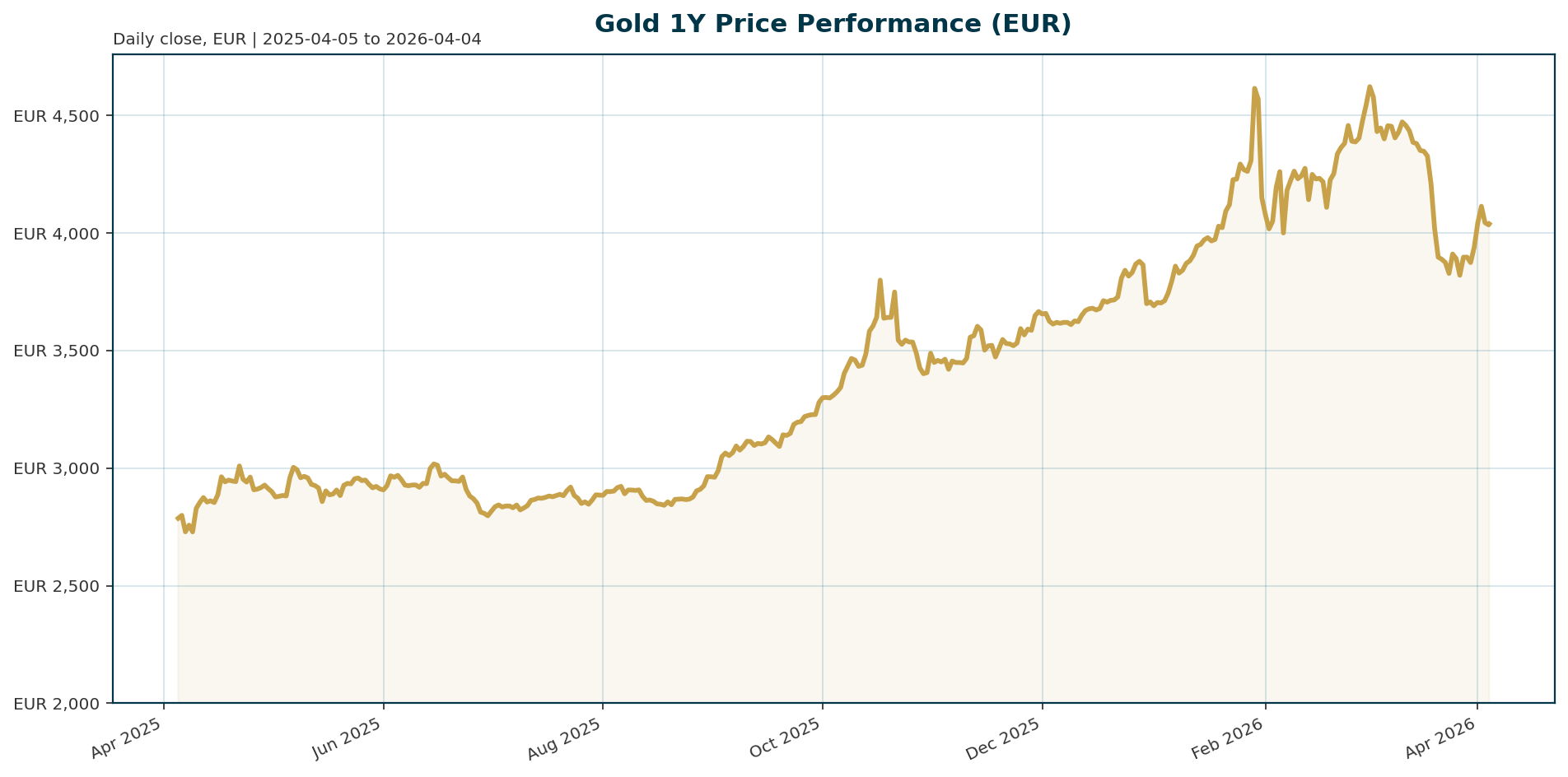

XAU/EUR trades at 4038.06 EUR, reflecting a sharp correction of -13.85% from its all-time high (ATH) of 4688.32 EUR set on January 29, 2026. The asset is currently testing the psychological threshold for a bear market, having fallen roughly 19% from its January peak [T2][T3]. Despite the recent pullback, the year-to-date performance remains robust at 43.77%, supported by a strong rally since early 2023.

| Metric | Value |

|---|---|

| Current Price (EUR) | 4,038.06 |

| ATH (Jan 29, 2026) | 4,688.32 |

| ATH Drawdown | -13.85% |

| 1-Year Return | +43.77% |

| 30-Day Return | -9.66% |

| 7-Day Return | +3.85% |

| US 10-Year Yield Proxy | ~4.50% |

| US National Debt | $39 Trillion |

Macro Backdrop

The macro environment remains “tight” with the Federal Reserve maintaining its federal funds rate target between 3.5% and 3.75% while penciling in a single rate cut for 2026 [T7]. Financial markets are currently grappling with rising war costs, which have pushed the 10-year US Treasury yield briefly above 4.5% for the first time since last summer [T8]. This yield environment is creating headwinds for non-yielding assets like gold.

Simultaneously, fiscal stress is mounting. The US national debt has reached a record $39 trillion, with annual net interest payments expected to hit $1 trillion this fiscal year [T8]. In the Eurozone, inflation remains sticky at 2.5% in March, complicating the central bank’s ability to pivot to easing [T5]. The Bank of England has explicitly urged market participants to prepare for periods of intense volatility, signaling that the current risk-off sentiment may persist [T5][T6].

Investment Thesis

The fundamental case for gold remains intact despite short-term volatility. Structural tailwinds persist, driven by inflation risks, fiscal pressures, and concerns over bond credibility [T2]. The primary narrative is the diversification of global reserves away from the US dollar, a theme accelerated by the freezing of Russian foreign exchange reserves [T2].

Gold serves as a critical hedge against currency debasement and the erosion of purchasing power caused by record government deficits. As central banks and institutional investors seek to protect wealth in a fractured geopolitical landscape, gold retains its status as the ultimate store of value. The recent dip is viewed by many strategists as a buying opportunity rather than a trend reversal, as the underlying drivers of debt accumulation and geopolitical fragmentation remain unchanged [T2][T3].

Bullish Drivers

Central Bank Accumulation: Despite rising geopolitical uncertainty, central banks remained net buyers of gold in February. This sustained institutional demand provides a floor for prices and signals long-term confidence in the metal as a reserve asset [T4].

Global Reserve Diversification: Singapore is actively positioning itself as an international bullion hub to attract global central bank reserves, competing with established hubs like London and Hong Kong [T1]. This competition suggests a structural increase in demand for physical storage and custody services.

Fiscal Stress: The record levels of US debt and the rising cost of servicing that debt ($1 trillion in interest payments) reinforce the argument for non-sovereign assets. Gold offers a non-correlated asset that is not exposed to sovereign default risk [T8].

Relative Positioning vs Bitcoin and Ethereum

Gold is currently outperforming major risk assets in the short term. While Bitcoin dominance stands at 56.12%, gold has posted a 7-day gain of 3.85%, contrasting with the volatility seen in the broader crypto market [T2][T3].

In a regime defined by “flight to quality,” gold typically outperforms cryptocurrencies. The recent market selloff saw investors liquidate positions across stocks, bonds, and currencies to cover losses elsewhere, with gold acting as a liquid safe haven [T2]. As long as geopolitical tensions drive volatility, the traditional hierarchy of assets places gold at the top of the liquidity chain, ahead of digital assets.

Scenario Framework

- Base Case (Recovery): Dip-buyers sustain the price around current levels. Central bank buying slows but remains positive. If Middle East tensions de-escalate, the “flight to quality” in the dollar eases, allowing EUR-denominated gold to reclaim support levels.

- Bear Case (Bear Market Confirmation): The 20% drawdown threshold is breached. This could be triggered by a sustained surge in US Treasury yields above 4.5% driven by war costs, combined with a stronger dollar as the ultimate safe haven [T3][T8]. A broader cohort of central banks, potentially following Turkey’s lead, could begin selling reserves.

- Bull Case (Resumption of Rally): War inflation pressures subside, prompting the Fed to cut rates sooner than expected. Bond yields retreat, compressing the real yield environment and making gold more attractive relative to interest-bearing assets. Gold reclaims its ATH of 4688.32 EUR.

Valuation Discussion

Valuation is currently dictated by the real yield environment. Using the 10-year US Treasury yield (~4.5%) as a proxy and Eurozone inflation (2.5%) as a deflator, the real yield proxy stands at approximately 2.0% [T5][T8].

At a price of 4038.06 EUR, gold is trading at a premium to its real yield. However, this valuation is supported by the fiscal backdrop. The P/E ratio (Price / Real Yield) suggests a premium is warranted given the $39 trillion debt burden and the risk of inflation resurgence [T8]. If yields continue to climb, the premium would compress, potentially leading to a re-rating of gold to lower price levels.

Risks

- Yield Spike Risk: The most immediate threat to XAU/EUR is a sustained rise in US Treasury yields. War-driven inflation could push the 10-year yield significantly higher, making gold less attractive relative to bonds [T7][T8].

- Dollar Strength: Geopolitical escalation has historically strengthened the US dollar as a safe haven. A stronger dollar directly suppresses the price of EUR-denominated gold [T3].

- Central Bank Pivot: While net buyers in February, the trend could reverse if Turkey’s sales of gold to support its currency are replicated by other nations [T2]. A shift in central bank sentiment from accumulation to distribution would remove a major pillar of support.

Appendix

Sources

- Singapore weighs adding gold storage for global central banks – Mining.com [T1]

- Dip-buyers arrive to pull gold back from brink of a bear market – Bitget [T2]

- Dip-buyers arrive to pull gold back from brink of a bear market – Mining.com [T3]

- Central banks remain net gold buyers in February despite rising geopolitical uncertainty – KITCO [T4]

- BOE Urges Readiness for More Periods of ‘Intense’ Volatility in Financial Markets – WSJ [T5]

- BOE Urges Readiness for More Periods of ‘Intense’ Volatility in Financial Markets – WSJ [T6]

- Fed’s Williams says monetary policy ‘well positioned’ for ‘unusual’ circumstances – KITCO [T7]

- Treasury market’s next test: rising war costs – kitco.com [T8]

This report is AI-generated by GLM 4.7 Flash for informational purposes only and does not constitute investment advice. The views expressed are those of the model and should not be taken as professional financial guidance.

Important Note / Wichtiger Hinweis:

EN: This report may contain AI-assisted analysis or be generated entirely by AI, which processes market data from publicly available sources for which altii accepts no responsibility for its accuracy. We strongly advise against using this report as a basis for investment decisions.

DE: Dieser Bericht kann KI-gestützte Analysen enthalten oder vollständig von KI erstellt worden sein, die Marktdaten aus öffentlich zugänglichen Quellen verarbeitet, für deren Richtigkeit altii keine Verantwortung übernimmt. Wir raten dringend davon ab, diesen Bericht als Grundlage für Anlageentscheidungen zu verwenden.