Listen to the summary

Key Data Snapshot

| Metric | Value |

|---|---|

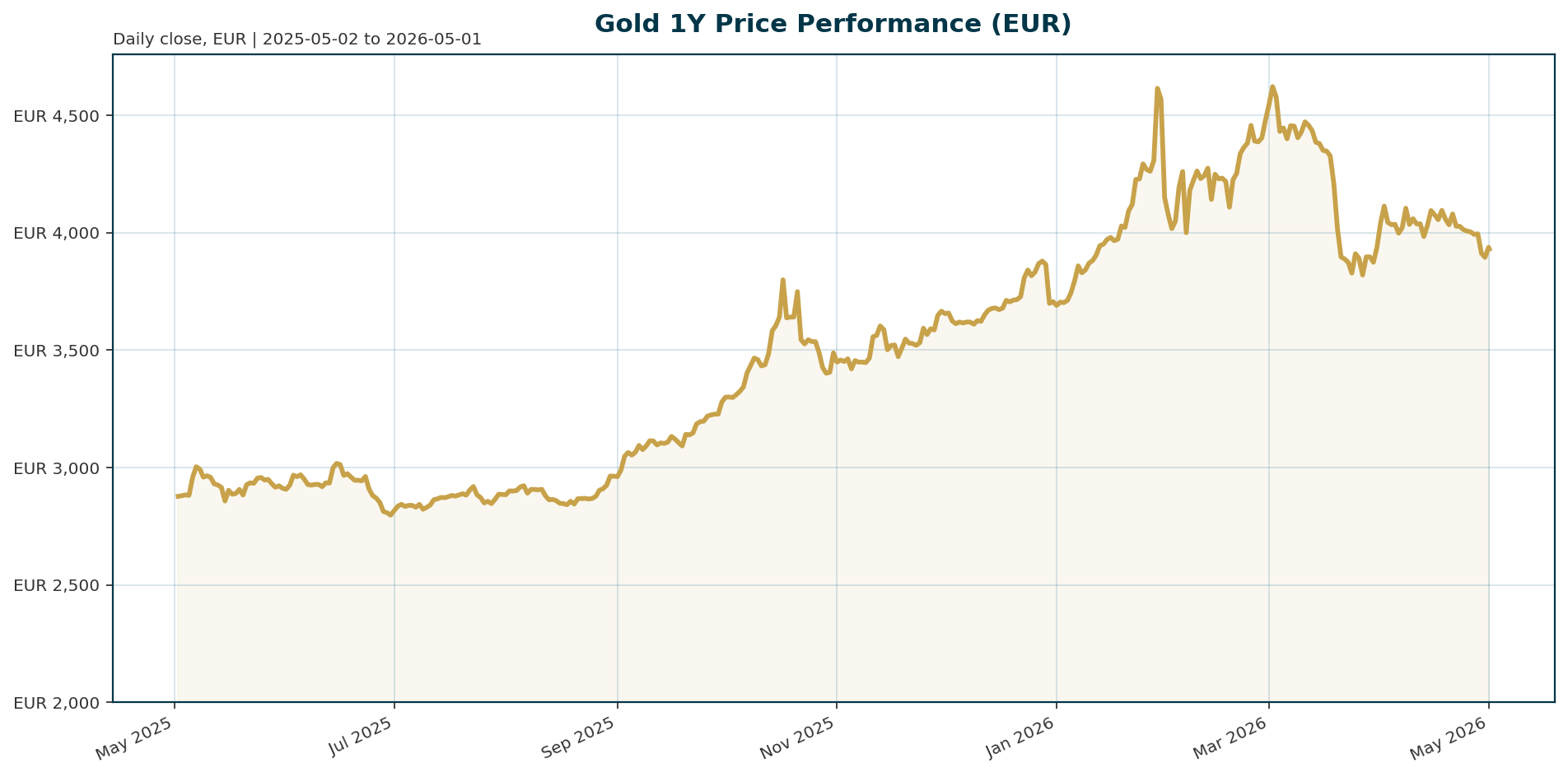

| Spot Price (XAU/EUR) | 3,930.73 |

| 24h Change | +0.86% |

| 7-Day Change | -1.66% |

| ATH (Jan 29, 2026) | 4,688.32 EUR |

| ATH Drawdown | -16.08% |

| 200-Day Return | +12.79% |

| Euro Area 10Y Yield | 3.14% |

| BTC Dominance | 58.23% |

Macro Backdrop

The immediate macro environment presents a complex dichotomy for gold. Global equity risk sentiment remains broadly positive, with the Nasdaq Composite leading on a 1-month basis at 15.29% and the DAX up 7.11% over the same period [T5]. This positive equity momentum creates a headwind for non-yielding assets like gold, diverting capital toward higher-yielding equities. However, the backdrop is not uniformly bullish for traditional risk assets. The Euro area yield curve is flattening, with the 10-year yield at 3.14% and the 2-year yield at 2.67% [T5]. This flattening, coupled with a mixed FX environment where EUR/USD sits at 1.1701, suggests that while investors are chasing growth, they are also wary of inflation persistence and the “higher-for-longer” rate environment that weighs on precious metal valuations.

Investment Thesis

The fundamental narrative for gold remains anchored in the structural shift toward de-dollarization. As trust in US assets erodes, sovereign wealth funds and central banks are aggressively pivoting away from the dollar, which has fallen from a peak of over 60% of global reserves to approximately 40% [T1][T4]. This trend is not limited to emerging markets, as evidenced by France’s recent strategic move to repatriate gold custody from the Federal Reserve Bank of New York to Europe, booking a €12.8 billion capital gain in the process [T7]. Gold is positioned to be the primary beneficiary of this fragmented financial system, serving as a sovereign hedge against counterparty risk and potential Western sanctions.

Bullish Drivers

Despite recent volatility, the structural supply and demand dynamics remain overwhelmingly supportive of the long-term bull case. Institutional demand is the primary catalyst, with central banks having purchased 863.3 tonnes of gold in 2025—the fourth-largest annual total on record—and forecast to buy approximately 850 tonnes in 2026 [T3]. This represents a near doubling of pre-2022 norms and creates a robust price floor that speculative selling has repeatedly failed to break through. Geopolitical fragmentation further underpins this thesis, with the World Gold Council noting that central banks view economic and geopolitical uncertainty as a key factor for accumulation [T4]. Additionally, rising energy prices are reviving inflation fears, which historically supports gold as a hedge against currency debasement [T5].

Relative Positioning vs Bitcoin and Ethereum

Gold maintains its status as the benchmark asset for the broader “hard money” complex, despite the dominance of Bitcoin in the crypto market cap hierarchy. With Bitcoin dominance currently at 58.23% and the total crypto market cap exceeding $2.2 trillion, digital assets represent a significant alternative store of value [T5]. However, gold remains the underlying asset backing many crypto-linked products, such as Pax Gold, and offers significantly lower volatility compared to Ethereum or Bitcoin. While crypto markets react to speculative liquidity and technological adoption, gold is driven by sovereign balance sheet management and macroeconomic uncertainty, positioning it as the more stable anchor in a diversified portfolio.

Scenario Framework

- Bull Case: De-dollarization accelerates, Euro yields fall, and geopolitical tensions in the Middle East escalate. If the Euro Area 10Y yield declines below 3.0% and the US Dollar weakens, XAU/EUR could reclaim the 4,500 EUR level and target Deutsche Bank’s projected $8,000 scenario [T1][T4].

- Base Case: Central bank buying remains strong at ~850 tonnes annually, absorbing supply shocks. Gold consolidates around the 4,000 EUR mark, trading in a range dictated by the flattening Euro yield curve and persistent geopolitical risk [T3][T5].

- Bear Case: The Federal Reserve maintains a hawkish stance, the US Dollar strengthens, and inflation expectations cool. This would increase the opportunity cost of holding gold, potentially pushing XAU/EUR to test the 3,600 EUR support level [T2][T4].

Valuation Discussion

Gold is currently trading at a discount to its January 2026 all-time high, offering a margin of safety for new entrants. However, the valuation is sensitive to the real yield environment. With the Euro Area 10Y yield at 3.14%, the opportunity cost of holding zero-yielding gold is elevated. The market is pricing in a risk premium for geopolitical instability, but a sustained period of high real yields could compress valuations. Despite this, the “price floor” established by the forecasted 850 tonnes of central bank purchases in 2026 suggests that downside risk is limited, as institutional demand provides a floor that speculative trading cannot easily breach [T3].

Risks

- Hawkish Monetary Policy: A stronger US Dollar and persistent inflation could force the Federal Reserve to keep interest rates higher for longer, making gold less attractive compared to short-term bonds [T2][T4].

- Liquidity Crunches: Recent price pullbacks have been exacerbated by ETF outflows and profit-taking, indicating that gold is susceptible to deleveraging in risk-off scenarios [T5].

- Geopolitical Resolution: A sudden de-escalation of the US-Iran conflict or a resolution to the Ukraine war could reduce safe-haven demand, triggering a sharp correction in bullion prices [T2].

Appendix

- Sources:

- Gold price could see $8,000 on de-dollarization, Deutsche Bank projects – Mining.com [T1]

- Central banks ‘scoop up a load’ of gold in bumpy first quarter – Bitget [T2]

- What Switzerland’s Gold Freeze Means for Investors – GoldSilver [T3]

- Gold to clinch $8,000 in just 5 years? Germany’s Deutsche Bank makes bold prediction – Bitget [T4]

- Gold Squeezed Between Safe-Haven Allure, Rate Fears as Underlying Demand Holds — Update – marketscreener.com [T5]

- Swiss central bank has no plans to increase gold reserves, says chairman – KITCO [T6]

- Comedy Gold: France’s Quiet Exit and the Option Value of Distrust – The Times of Israel [T7]

- Japan’s fiscal and monetary policy still favors the bulls, says Jim Caron – CNBC [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. The analysis is based on data available up to May 1, 2026, and should not be considered a guarantee of future performance.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.