Listen to the summary

Key Data Snapshot

| Metric | Value | Change (Period) |

|---|---|---|

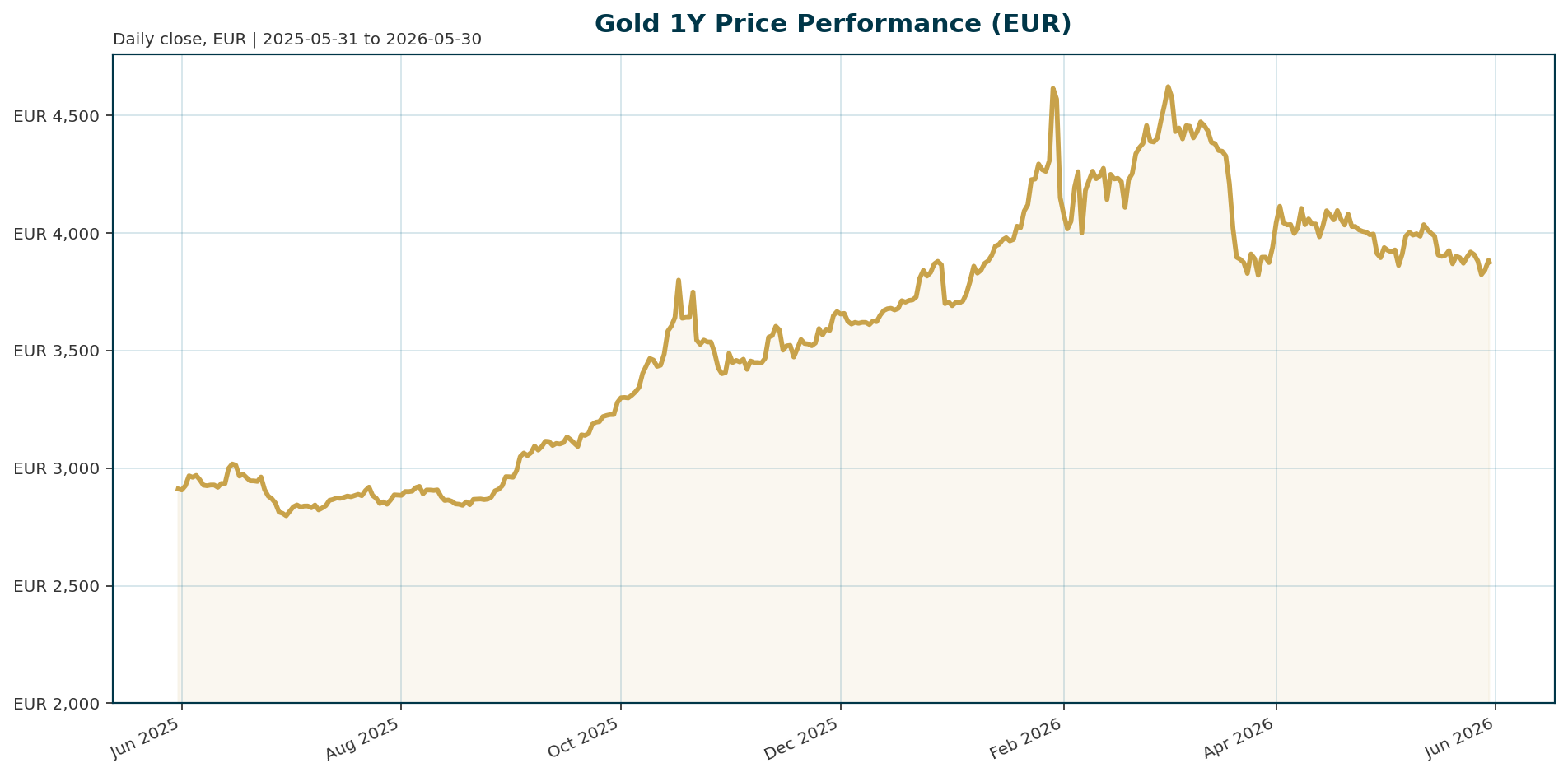

| Price (XAU/EUR) | 3,876.92 | +0.39% (24h) |

| 1-Year Return | 32.94% | YTD |

| 200-Day Return | +8.51% | YTD |

| All-Time High (ATH) | 4,688.32 | -17.29% (from ATH) |

| Market Cap Rank | 43 | Global Crypto |

| BTC Dominance | 57.42% | Global Crypto |

Macro Backdrop

Global risk sentiment remains positive, driven by a 2.39% five-day gain in the Nasdaq Composite, while Eurozone equities lag with the DAX down 1.12%. The Euro area AAA 10-year yield sits at 3.03%, moving -4.8 basis points over the last five days, creating a mixed backdrop for interest-rate-sensitive assets. Markets are pricing in a 41% probability of a December Federal Reserve rate hike according to CME Group data, while the EUR/USD pair trades at 1.1655, offering limited direct FX headwinds for gold denominated in Euros.Investment Thesis

The investment thesis for Gold is bifurcated between structural de-dollarization and short-term rate sensitivity. The long-term narrative remains bullish, anchored by the weaponization of the dollar and the erosion of its reserve currency prestige, which supports central bank accumulation [T1]. Conversely, the short-term thesis is constrained by elevated real yields, specifically US 30-year Treasury yields maintaining above 5%, which increases the opportunity cost of holding non-yielding assets [T3]. The market is currently navigating a divergence where geopolitical risks drive safe-haven demand, but monetary policy tightening dampens price action.Bullish Drivers

Several structural catalysts support the long-term bull case for Gold. Central banks continue to extend buying streaks, with China adding to reserves and Ghana implementing a 30% reserve-building mandate for miners [T7]. A potential “bond crisis” or loss of confidence in government debt quality could trigger a flight to hard assets, as analysts note the fragility between rising yields due to inflation and the risk of a systemic debt crisis [T5]. Furthermore, stagflationary risks stemming from the Iran conflict, which has spiked oil prices, reinforce Gold’s role as a hedge against persistent inflation and currency debasement [T4].Relative Positioning vs Bitcoin and Ethereum

Gold is currently underperforming risk assets despite geopolitical stress, as the Nasdaq Composite leads global equities with a 5-day gain of 2.39% while the Hang Seng lags at -1.65% [market_overview]. This divergence suggests that rate expectations are currently overriding safe-haven flows into Gold. Meanwhile, Bitcoin dominance stands at 57.42%, indicating a rotation into crypto as a hedge against traditional monetary policy risks. Silver has shown relative strength through the recent selloff, holding its 50-day moving average and potentially outperforming Gold if the macro regime shifts toward stagflation [T6].Scenario Framework

- Bear Case: Real yields remain elevated above 5% on the 30-year US Treasury, and the Fed maintains a hawkish stance. In this scenario, Gold faces further downside pressure, with analysts warning of a potential correction toward $4,000 per ounce [T3][T5].

- Bull Case: A collapse in real yields or a significant devaluation of the USD triggers a “second wind” for Gold. If the weaponization of the dollar accelerates, analysts predict Gold could reach $10,000 per ounce driven by reserve diversification [T1][T5].

- Neutral/Stagflation Case: Oil prices remain sticky due to the Iran conflict, keeping inflation elevated. The ECB may be forced to adopt a more restrictive policy if inflation overshoots targets, keeping Gold range-bound but supported by central bank buying [T8].

Valuation Discussion

At 17.29% below its January 2026 ATH of 4,688.32 EUR, Gold offers a premium entry point relative to recent highs. The pullback is viewed by some as a “breath” rather than a trend reversal, with portfolio managers citing a “firm floor” provided by central bank demand [T1]. Rick Rule of Rule Investment Media characterizes the current weakness as “heaven-sent,” arguing that higher rates will eventually force policymakers to cut rates, which would trigger a dramatic move in Gold [T2]. The valuation is supported by Gold’s “risk-free partnership” characteristics relative to deteriorating government bond quality [T3].Risks

- Real Yield Growth: Rising US Treasury yields, currently exceeding 4.5% on the 10-year and 5% on the 30-year, remain the primary headwind, acting as the biggest barrier to precious metals [T3].

- Fed Hawkishness: A confirmed December rate hike or a prolonged period of restrictive monetary policy would likely exacerbate the current correction [T4].

- Geopolitical Escalation: While currently a safe-haven driver, a prolonged conflict that severely disrupts energy supply chains could force central banks to keep rates high to combat inflation, negating Gold’s inflation hedge appeal [T8].

Appendix

Sources

- Gold is just taking a breath and the race is not over – KITCO [T1]

- Gold pullback puts rate pressure, mining M&A back in focus – KITCO [T2]

- Gold prices play a good role as a shelter, silver has a large growth potential – Laodong.vn [T3]

- Gold falls as renewed US-Iran tensions dampen peace hopes, clouds interest rate outlook – KITCO [T4]

- Experts worry about US bonds, gold prices may fluctuate sharply – Laodong.vn [T5]

- Gold SWOT: Net gold ETF inflows turned positive for the first time since early April – KITCO [T6]

- China’s Gold Holdings Rise Again as Central Bank Extends Buying Streak – The Jerusalem Post [T7]

- ECB’s Stournaras says more restrictive monetary policy needed if inflation overshoots target – CNBC [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. Always conduct your own research before making financial decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.