Listen to the summary

Key Data Snapshot

| Metric | Value | Context |

|---|---|---|

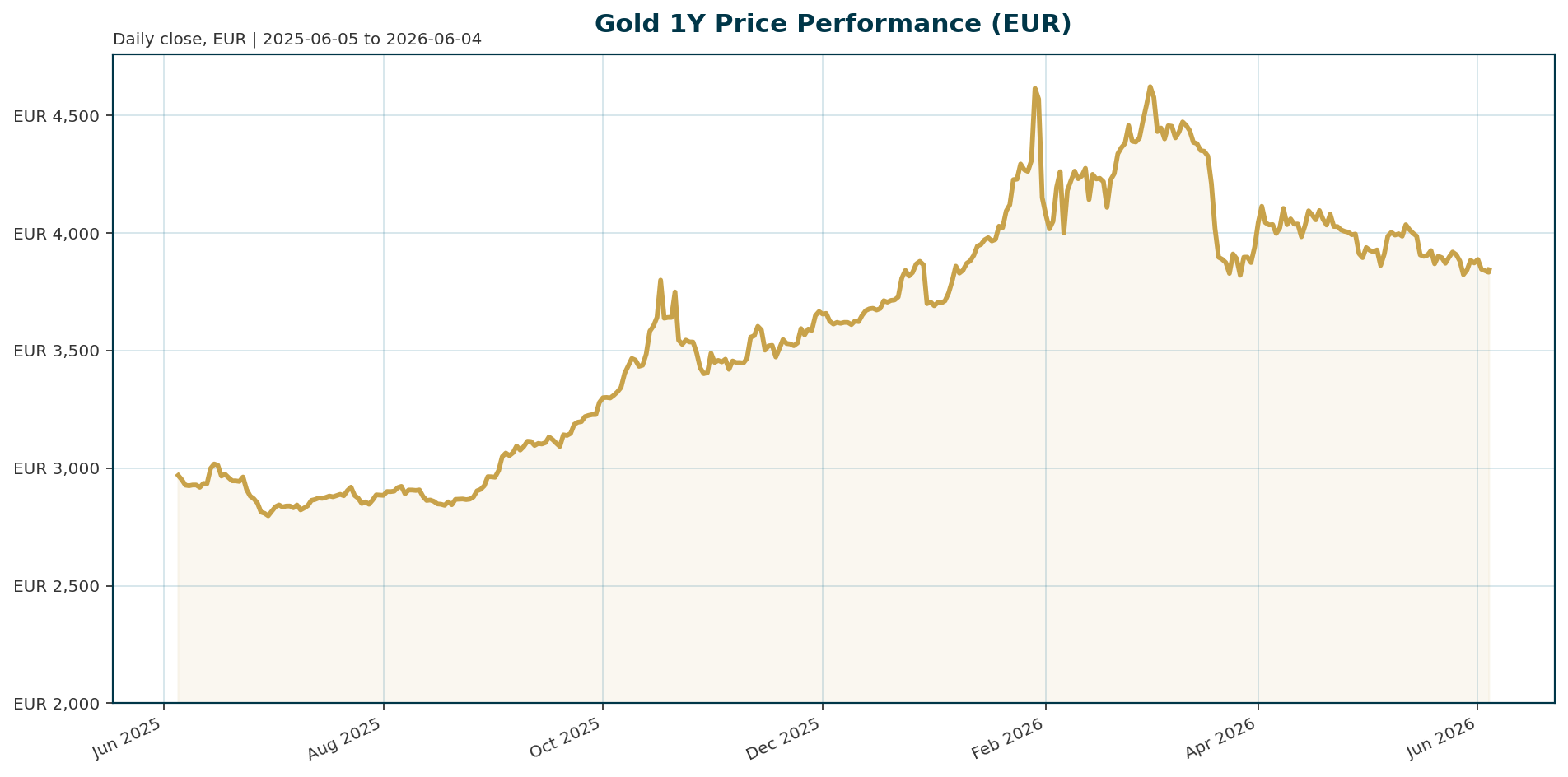

| XAU/EUR Price | 3,843.02 | Current price |

| YTD Performance | +29.35% | Strong annual gain |

| ATH Drawdown | -18.03% | From 4,688.32 EUR (Jan 2026) |

| Global Reserve Share | 27% | ECB report: Gold > US Treasuries (22%) [T1][T7] |

| Q1 2026 Demand | 1,231 tonnes | Record high including OTC [T2] |

| Central Bank Q1 Net Buys | 244 tonnes | td>Robust institutional demand [T2]|

| Euro Area 10Y Yield | 3.02% | td>Rate backdrop [market_overview]

Macro Backdrop

Risk sentiment remains broadly neutral to positive, yet regional divergences are evident. The DAX struggles with a 5-day decline of 1.18%, while the Nikkei 225 leads with a 5-day gain of 1.41%, suggesting a rotation away from European equities toward Asian markets. The Euro Area 10-year yield sits at 3.02%, reflecting a mixed rates environment where real yields continue to weigh on non-yielding assets. The EUR/USD pair is trading at 1.1627, down 0.24% over the past week, which introduces a currency headwind for XAU/EUR. The Federal Reserve maintains a hawkish stance, with New York Fed President Williams stating monetary policy is in the ‘right place’ amid inflation risks [T8], keeping the opportunity cost of holding gold elevated.

Investment Thesis

The core thesis rests on the Federal Reserve’s “policy trap” [T5]. The Fed faces an increasingly difficult balancing act between sticky inflation and rising sovereign debt risks. Higher real yields increase the opportunity cost of holding gold, yet the financial strain from these yields signals deteriorating fiscal health, which ultimately benefits the precious metal. Furthermore, a structural shift in global reserves is underway. The European Central Bank confirmed gold now constitutes 27% of global official reserves, overtaking US Treasuries for the first time since 1996 [T1][T4]. This de-dollarization trend, driven by geopolitical fragmentation, positions gold as the premier alternative reserve asset.

Bullish Drivers

- Structural Reserve Diversification: Central banks remain the primary demand engine. A WGC survey indicates 95% of respondents expect global reserves to increase over the next 12 months [T3]. Poland and China continue aggressive accumulation, with Poland targeting 700 tonnes and China holding 2,322 tonnes (9% of reserves) [T3].

- Record Demand Fundamentals: Global gold demand hit 1,231 tonnes in Q1 2026, the highest January-March figure on record. This includes robust central bank buying of 244 tonnes and a 50% year-on-year rise in private investment [T2].

- Geopolitical Risk Premium: The freezing of Russian dollar reserves following the 2022 Ukraine invasion has permanently altered reserve management strategies. Gold offers no counterparty risk and cannot be frozen or seized [T4].

- Supply Constraints: Gold supply is inelastic and does not adjust seamlessly to demand shifts, providing a natural floor for prices [T1].

Relative Positioning vs Bitcoin and Ethereum

Gold maintains its dominance as the global reserve anchor, with a market cap of $1.77B compared to the total crypto market cap of $2.0T. Bitcoin dominance stands at 55.49%, indicating a risk-on rotation into digital assets. While gold’s 30-day performance is negative at -0.88%, its 1-year return of +29.35% remains superior to the broader equity risk appetite. Gold acts as the primary hedge against systemic risk, whereas Bitcoin and Ethereum are currently viewed as speculative growth assets in this macro cycle.

Scenario Framework

- Bull Case: A dovish shift at the upcoming FOMC meeting (June 16-17) or softening labor data could trigger a rate cut. This would lower real yields and strengthen the EUR, providing significant upside for XAU/EUR.

- Bear Case: Persistent inflation data (April CPI nearly double the 2% target) reinforces Fed hawkishness. Elevated real yields and a firmer USD would likely pressure gold lower, testing the 18% drawdown from ATH.

- Base Case: The Fed maintains a data-dependent stance. Gold consolidates around current levels, with volatility driven by upcoming US macro releases such as JOLTS and unemployment claims [T2].

Valuation Discussion

Gold is currently trading 18% below its all-time high of 4,688.32 EUR, suggesting the recent correction has trimmed some speculative premium. However, valuation remains sensitive to real yield levels. At current EUR/USD levels (1.1627), gold is expensive for international buyers, limiting upside until the currency strengthens. The ECB notes that while gold’s share of reserves has surged, its price volatility and storage costs remain limitations compared to fiat currencies [T1].

Risks

- Real Yield Spike: A rapid increase in US real yields would immediately increase the opportunity cost of holding gold, triggering a sharp correction.

- USD Strength: A sustained firming of the US dollar makes gold more expensive for non-US buyers, dampening demand.

- Central Bank Slowdown: While demand remains robust, a significant drop below the 850 tonnes/year purchase target would question the structural demand floor [T1].

Appendix

Sources

- Central banks see gold as the reserve asset of choice – ECB report – KITCO [T1]

- July, gold losing $90 in what could be fourth successive monthly drop – KITCO [T2]

- Central banks buy net 17 tonnes of gold in April, led by Poland and China – WGC – KITCO [T3]

- Central Banks Picked Gold Over Treasuries. Should You? – GoldSilver [T4]

- Fed trapped between inflation and debt crisis, and gold wins either way – Sprott’s McIntyre – KITCO [T5]

- Gold overtakes US Treasuries in global reserve shift: ECB – Mining.com [T7]

- Fed’s Williams tells Yahoo monetary policy is in ‘right place’ amid inflation risks – KITCO [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed herein are those of the model and do not reflect the official positions of any financial institution.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.