Listen to the summary

Key Data Snapshot

| Metric | Value |

|---|---|

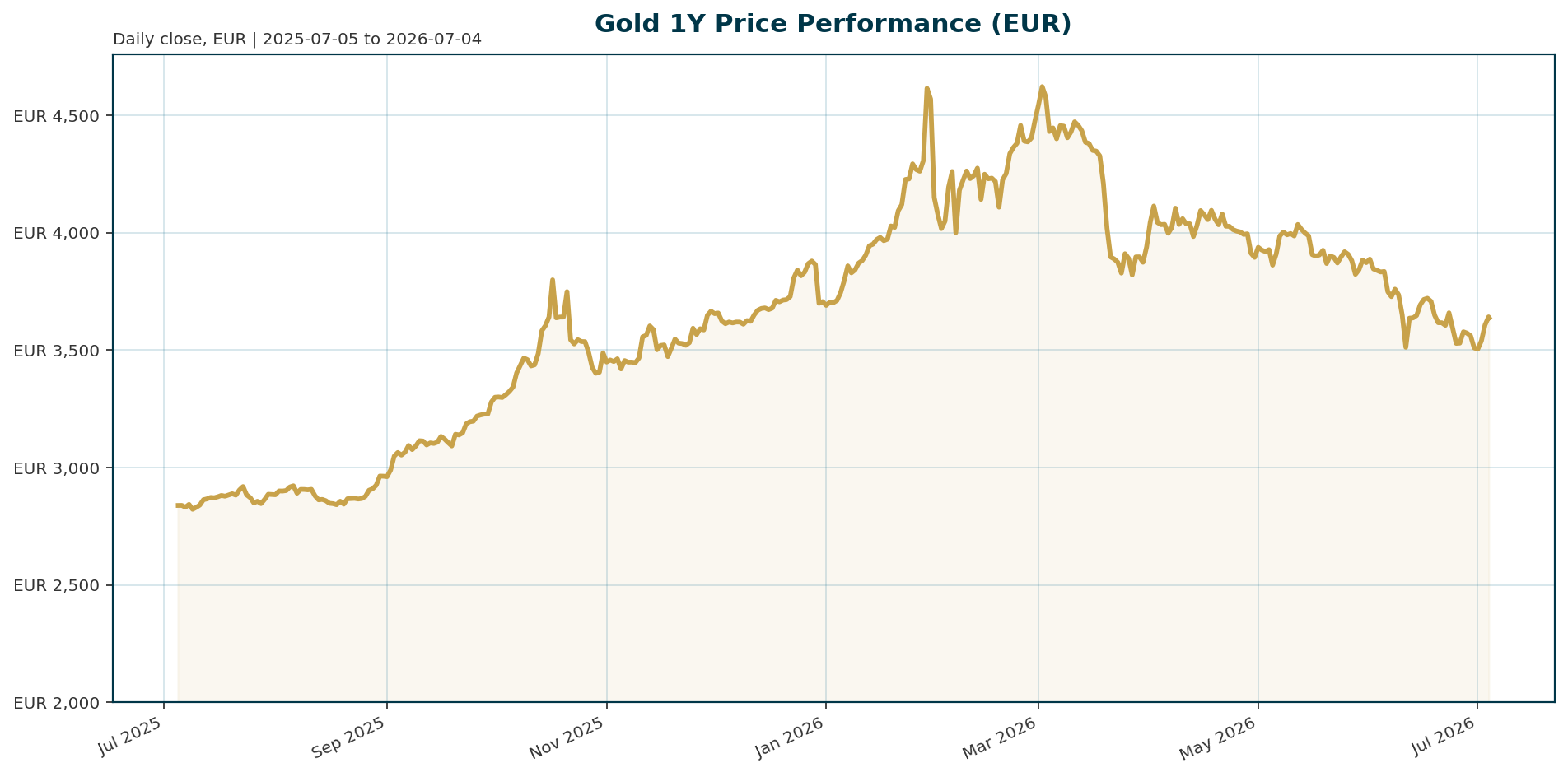

| Price (XAU/EUR) | 3,637.33 |

| All-Time High (ATH) | 4,688.32 (Jan 2026) |

| ATH Change | -22.41% |

| 1-Year Return | +28.40% |

| 7-Day Return | +1.72% |

| 24h Volume | 76.76M EUR |

| BTC Dominance | 55.69% |

Macro Backdrop

Risk sentiment is neutral to positive, supported by outperformance in DACH equities where the DAX gained 4.68% over five days against a mixed global equity backdrop. The Euro area yield curve is steepening with AAA 10Y yields at 2.99%, while EUR/USD trades at 1.1444, creating a complex environment for EUR-denominated assets. Rates are mixed but generally hawkish, with Euro area yields rising and US real yields remaining elevated above 2%, limiting immediate upside for the yellow metal.Investment Thesis

Gold is transitioning from a pure inflation hedge to a core portfolio diversifier and reserve asset. The structural shift toward a multipolar monetary system is driving central bank accumulation, with 61% of respondents expecting prices between $5,000 and $6,000 by 2027 [T2]. Despite equity strength in DACH, cross-asset correlations suggest gold remains a critical hedge against fragmentation [T5].Bullish Drivers

- Central Bank Accumulation: A record 45% of central banks plan to increase holdings over the next 12 months, with nearly 90% expecting total global reserves to rise [T3]. The OMFIF survey highlights a global trend where gold is the second most desired asset for long-term portfolios [T2].

- Geopolitical Fragmentation: Conflict in the Middle East and uncertainty surrounding US policy reinforce gold’s monetary role, with 85% of reserve managers citing the Middle East as their top geopolitical risk [T2].

- Policy Pivot Potential: Fed Chair Warsh’s comments suggesting inflation risks have come down could trigger a resurgence in the “debasement trade,” reviving demand for hard assets [T6]. HSBC anticipates further upside for gold by year-end, maintaining an Overweight stance [T5].

Relative Positioning vs Bitcoin and Ethereum

BTC dominance stands at 55.69%, but gold and Bitcoin moved in tandem (+1.07% vs +2.38%) on the day Warsh spoke, suggesting a shared risk correlation rather than distinct asset classes [T6]. Gold’s defensive utility is highlighted by its outperformance against the S&P 500 (-0.33%) on days of strength [T6]. As cross-asset correlations rise, gold becomes more valuable as a diversifier, particularly for institutional investors seeking to balance exposure to digital assets and traditional markets [T5].Scenario Framework

- Base Case: The Fed remains hawkish, with 10Y US real yields staying elevated above 2% through Q3. Gold trades rangebound between 3,637 and 3,800 EUR, supported by central bank buying but capped by opportunity costs [T4].

- Bull Case: Inflation risks drop faster than expected, the debasement trade reignites, and the Fed pivots to dovish. Gold breaks its January ATH and targets the $5,000 level anticipated by central banks [T2][T6].

- Bear Case: Geopolitical tensions in the Middle East escalate, spiking energy prices and real yields. Gold corrects below 3,500 EUR as investors rotate into yield-bearing assets.

Valuation Discussion

Current levels are down 22.4% from the January ATH but up 28.4% year-on-year, suggesting a valuation premium driven by structural demand rather than speculative debasement alone. Valuation is increasingly dictated by real yields; as long as real yields remain above 2%, the opportunity cost of holding gold remains a headwind [T4]. The “reset” phase from the historic rally is over, with price action now dictated by macro policy and central bank balance sheet composition.Risks

- Geopolitical Escalation: A worsening of the Middle East conflict could spike real yields and energy prices, creating a “risk-off” environment that favors USD strength over gold [T2][T4].

- Yield Competition: Euro area yield steepening and persistent US real yields above 2% continue to compete with gold for capital allocation [market_overview][T4].

- Policy Stagnation: Failure of the Fed to pivot from a hawkish stance could keep real yields elevated, limiting upside to the current range and pressuring EUR-denominated gold [T1].

Appendix

Sources

- Gold and silver: From reset to setup heading into Q3 – KITCO [T1]

- Central banks see gold prices trading between $5,000 and $6,000 in 12 months – OMFIF Survey – KITCO [T2]

- Central banks are still betting on gold – KITCO [T3]

- Gold’s biggest buyers aren’t slowing down, but SocGen sees a more measured pace ahead – KITCO [T4]

- ‘We anticipate further upside for gold by year-end’ – HSBC’s Sels and Ku – KITCO [T5]

- Warsh’s throwaway comment injects life into the debasement trade, for one day at least – MarketWatch [T6]

- Gold and silver market update: Why interest rate changes may mislead investors – KITCO [T7]

This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed herein are those of the AI assistant and do not reflect the official positions of any financial institution or entity.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.