Listen to the summary

Key Data Snapshot

| Indicator | Value | Context |

|---|---|---|

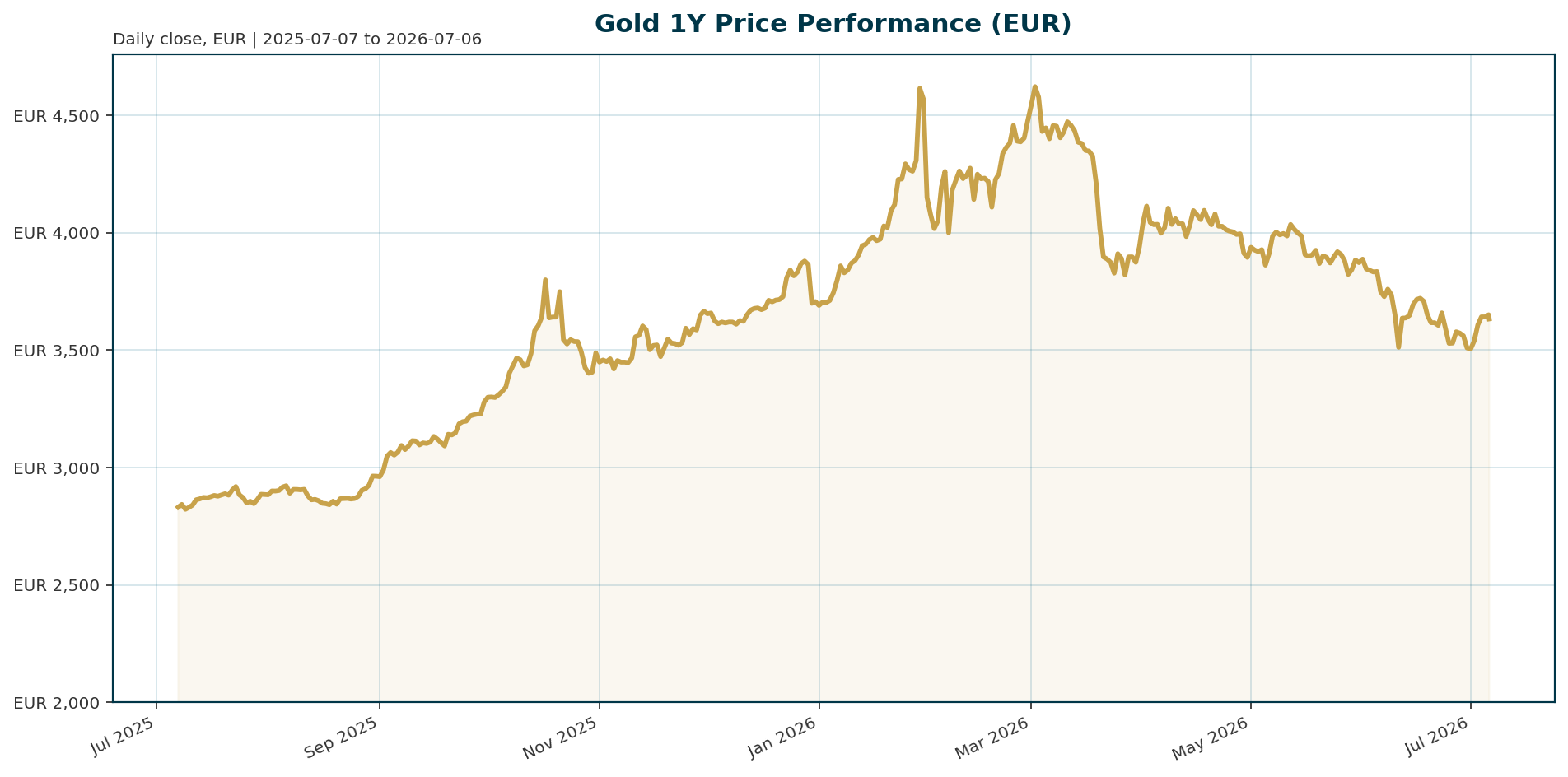

| Current Price (XAU/EUR) | 3,632.21 | Trading 22.5% below January 2026 ATH of 4,688.32 EUR. |

| 1-Year Return | +27.99% | Significant outperformance versus traditional risk assets. |

| Central Bank Consensus | $5,000 – $6,000 | 61% of reserve managers expect this range by June 2027 [T2][T3]. |

| US Real Yields (SocGen) | > 2% | Elevated real yields act as a headwind through Q3 [T4]. |

| Euro Area 10Y Yield | 2.99% | Steepening curve (5d +6.55bp) supports non-yielding assets. |

Macro Backdrop

The macro backdrop presents a mixed environment for Gold. Risk sentiment remains neutral to positive, with DACH equities leading global indices on a five-day basis. Euro area yields are steepening, with the 10-year AAA yield rising 6.55 basis points to 2.99 percent, which generally supports non-yielding assets. However, the EUR/USD pair is mixed, limiting some upside for EUR-denominated Gold. The DAX leads regional performance with a 4.68% five-day gain, while the Euro area curve steepening suggests a potential shift in monetary policy stance that could eventually benefit gold.Investment Thesis

Gold is transitioning from a cyclical commodity to a structural monetary asset. The core thesis rests on the inevitable fragmentation of the global monetary system. Nearly 80% of central banks believe the world is moving toward a multipolar reserve structure [T6]. Gold is no longer viewed merely as a hedge but as a central pillar of reserve management strategy. As public investors increasingly view volatility as a permanent feature, gold offers the liquidity and “store of value” properties required to navigate a de-dollarizing world [T6].Bullish Drivers

Structural demand remains the primary bullish anchor. A record 45% of central banks expect to increase their gold holdings over the next 12 months, reinforcing the floor under the market [T3]. Forward guidance from major institutions is constructive. Goldman Sachs forecasts gold approaching $4,900 next year, while HSBC maintains an Overweight stance and anticipates further upside by year-end [T3][T5]. Additionally, Federal Reserve Chair Kevin Warsh’s comments on declining inflation risks have successfully revived the “debasement trade,” which helped propel gold above $5,000 previously and suggests a path for renewed price discovery [T1][T7].Relative Positioning vs Bitcoin and Ethereum

Gold and Bitcoin currently share a correlation driven by the “debasement trade” narrative, as evidenced by both assets rallying on Warsh’s comments [T7]. However, their fundamental drivers differ. Gold is viewed as a safe haven and portfolio diversifier against broader risks, whereas Bitcoin remains a risk-on asset correlated with tech equities. During the recent Iran conflict, gold moved in tandem with equities rather than acting as a safe haven, highlighting its current status as a growth proxy [T5]. If the Fed pivot leads to a liquidity-driven rally, Bitcoin may outperform. Conversely, if the pivot is driven by economic weakness, gold is likely to hold up better as a defensive play.Scenario Framework

- Base Case: US Real Yields remain above 2% through Q3 as per SocGen’s central scenario [T4]. Gold consolidates between 3,500 and 3,800 EUR. Central bank buying provides a floor, preventing a deeper correction despite elevated opportunity costs.

- Bull Case: Fed Chair Warsh’s dovish pivot materializes, leading to a steepening of the Treasury curve and a decline in real yields. Gold breaks the 4,688.32 EUR ATH, targeting 4,500+ EUR as the multipolar reserve narrative accelerates.

- Bear Case: Real yields spike above 3% due to persistent inflation or hawkish policy, or the Middle East conflict escalates. Gold tests the 200-day moving average support, potentially dropping toward 3,500 EUR.

Valuation Discussion

Gold currently trades at a significant discount to its January 2026 all-time high, offering an attractive entry point for investors betting on the structural shift in reserves. The market is pricing in the recent volatility and the headwind of elevated real yields. However, the consensus of 61% of central banks expecting prices to trade between $5,000 and $6,000 by June 2027 implies substantial upside potential from current spot levels (~3,740 EUR implied). This forward guidance suggests the current price discount to the ATH is a temporary consolidation phase rather than a permanent de-rating of the asset.Risks

The primary risk is the persistence of elevated US Real Yields. SocGen forecasts 10Y US Real Yields will remain above 2% through Q3, which will continue to limit gold’s upside by increasing the opportunity cost of holding the non-yielding metal [T4]. Geopolitical risks remain elevated, with 85% of central banks citing the Middle East conflict as their top concern [T2]. Additionally, the recent rally in the US dollar driven by Warsh’s comments highlights the sensitivity of gold to Fed rhetoric; a hawkish surprise could trigger a sharp correction in the precious metal.Appendix

Sources

- Gold and silver: From reset to setup heading into Q3 – KITCO [T1]

- Central banks see gold prices trading between $5,000 and $6,000 in 12 months – OMFIF Survey – KITCO [T2]

- Central banks are still betting on gold – KITCO [T3]

- Gold’s biggest buyers aren’t slowing down, but SocGen sees a more measured pace ahead – KITCO [T4]

- We anticipate further upside for gold by year-end – HSBC’s Sels and Ku – KITCO [T5]

- For first time, more central banks are set to shrink dollar holdings, survey finds – Reuters [T6]

- Warsh’s throwaway comment injects life into the debasement trade, for one day at least – MarketWatch [T7]

This report is AI-generated for informational purposes only and does not constitute investment advice. Readers should conduct their own due diligence before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.