Listen to the summary

Key Data Snapshot

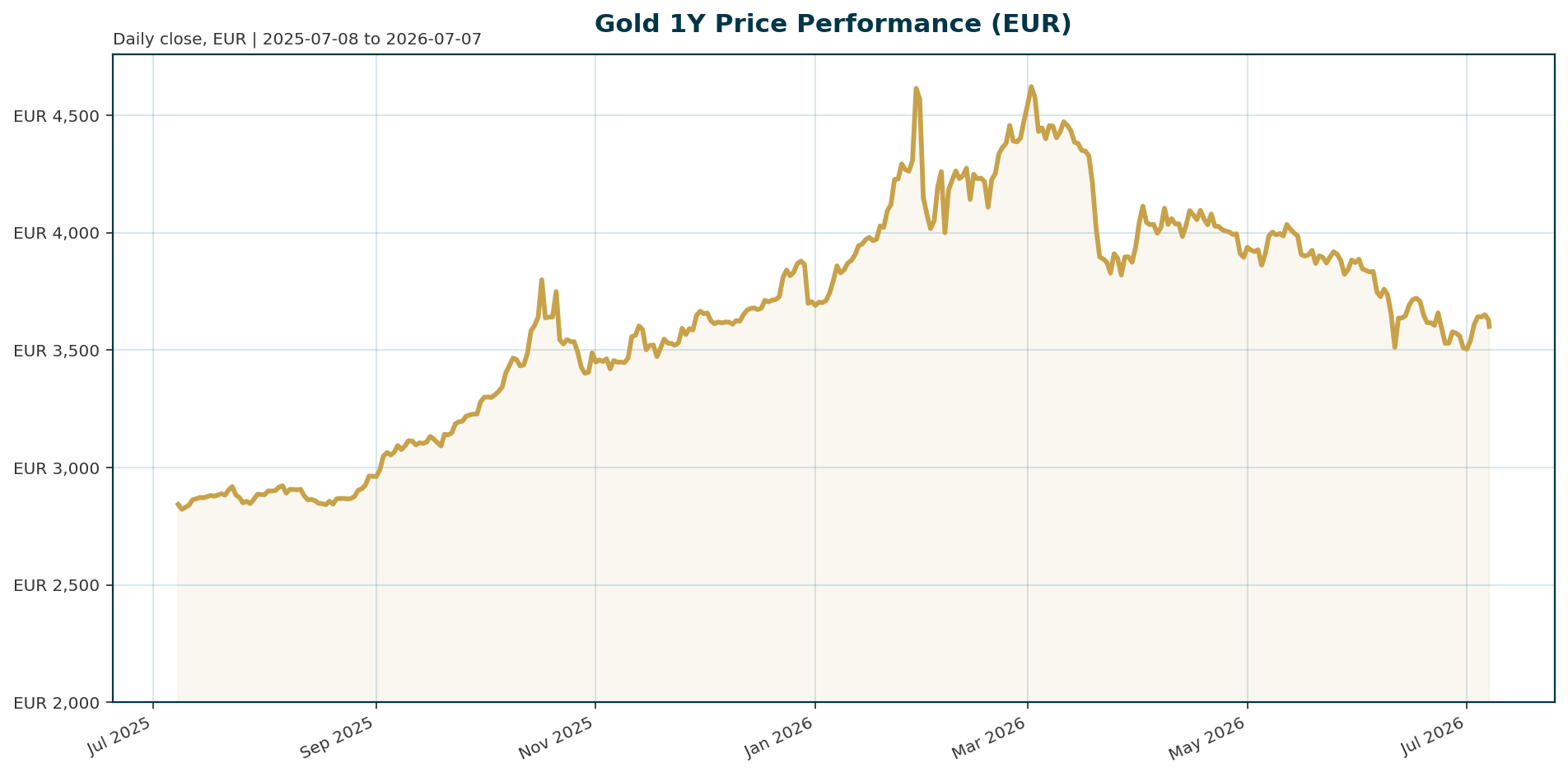

XAU/EUR trades at 3602.29, sitting on long-term support levels following a historic rally that saw prices peak at 4688.32 in January 2026. The asset has corrected 23.21% from its all-time high but remains up 27.76% over the last year. Despite a 30-day pullback of -3.55%, the market shows signs of stabilization with a positive 7-day change of +3.09%.

| Metric | Value |

|---|---|

| Current Price (XAU/EUR) | 3,602.29 |

| 24h Change | -0.65% |

| 30d Change | -3.55% |

| 200d Change | -2.46% |

| 1Y Change | +27.76% |

| ATH (Jan 29, 2026) | 4,688.32 |

| ATH Drawdown | -23.21% |

| Market Cap | 1.63B EUR |

| 24h Volume | 87.00M EUR |

Macro Backdrop

Risk sentiment is neutral to positive, with DACH equities outperforming global peers. The DAX leads with a 5-day gain of 3.29%, while the Euro Area AAA 10Y yield sits at 3.01% with a steepening curve. The FX backdrop is mixed, with EUR/USD at 1.143, offering marginal support for EUR-denominated gold, though the strong U.S. dollar remains a headwind. Recent comments from Fed Chair Kevin Warsh noting falling inflation risks temporarily revived the “debasement trade,” pushing gold up 1.1% as risk assets sold off [T8].

Investment Thesis

The core thesis for gold has shifted from a cyclical inflation hedge to a structural monetary asset driven by global fragmentation. Central banks are actively diversifying away from the U.S. dollar, viewing gold as the premier safe asset in a multipolar monetary system [T2]. Structural monetary debasement, driven by fiscal dominance and money printing, remains the dominant long-term driver rather than short-term inflation fears [T5]. The market is pricing in a pivot from the Fed’s hawkish stance to a more dovish approach, which would alleviate pressure on real yields.

Bullish Drivers

- Central Bank Accumulation: Global reserve managers remain overwhelmingly constructive. The OMFIF survey found 61% of respondents expect gold to trade between $5,000 and $6,000 by June 2027, while 45% plan to increase their own holdings [T2][T3].

- Institutional Flows: China’s largest ETF has flipped from equities to gold, signaling a major shift in domestic capital allocation [T7]. HSBC maintains an Overweight stance, anticipating further upside by year-end despite near-term headwinds [T4].

- Policy Expectations: Markets are pricing in a Fed transition from hawkish to dovish. J.P. Morgan notes that while the Fed has paused the structural bull story, the expectation of future cuts supports the asset [T6]. Goldman Sachs forecasts gold could approach $4,900 next year [T3].

Relative Positioning vs Bitcoin and Ethereum

In the short term, gold is underperforming Bitcoin, which gained 2.38% while gold slipped 0.65% [T8]. This suggests a rotation into risk assets. However, gold retains its distinct role as a portfolio diversifier. HSBC notes that while gold moved in tandem with equities during the Iran conflict, it remains a critical hedge against broader portfolio risks, unlike the highly speculative nature of crypto [T4]. Gold is viewed as the “hard money” anchor in a de-dollarizing world, contrasting with the volatility of digital assets.

Scenario Framework

- Bullish Scenario: Fed Chair Warsh signals a dovish pivot, inflation risks decline further, and the dollar weakens. Real yields fall, triggering a breakout above the January ATH toward $4,900+.

- Base Case: The Fed maintains restrictive policy (“deeper freeze”) while real yields remain elevated. Gold trades rangebound between 3,500 and 4,000 EUR, supported solely by relentless central bank buying and ETF inflows.

- Bearish Scenario: A resurgence in inflation or geopolitical escalation causes real yields to spike. Gold fails to find support, correcting further to test 2024 lows as the “debasement trade” reverses.

Valuation Discussion

Current levels present a compelling entry point following a 23% drawdown from the January ATH. The market cap of 1.63B EUR reflects a maturing infrastructure, but the structural demand from central banks dwarfs this supply. Valuation metrics suggest gold miners remain significantly undervalued relative to spot prices, offering leverage to a potential bull run [T5]. The current price of 3602.29 EUR is supported by long-term technical levels, with the path of least resistance appearing higher [T1].

Risks

- Real Yield Shock: Persistent spikes in U.S. or Euro Area real yields would cap gold’s upside. J.P. Morgan cautions that gold may not reliably offset market corrections if real yields remain high [T6].

- Correlation Breakdown: If gold continues to move in tandem with equities rather than acting as a safe haven, it could face significant selling pressure. HSBC noted gold did not rally during the Iran conflict, moving with equities [T4].

- Geopolitical Resolution: While current conflict drives safe-haven flows, a sudden resolution to the Middle East conflict could remove the premium supporting the price [T2].

Appendix

Sources

- Gold and silver: From reset to setup heading into Q3 – KITCO [T1]

- Central banks see gold prices trading between $5,000 and $6,000 in 12 months – OMFIF Survey – KITCO [T2]

- Central banks are still betting on gold – KITCO [T3]

- ‘We anticipate further upside for gold by year-end’ – HSBC’s Sels and Ku – KITCO [T4]

- Gold’s correction is a buying opportunity as governments won’t tolerate economic pain – Waratah Capital’s Dunkley – Bitget [T5]

- Fed turned a ‘pause in the structural bullish gold story’ into ‘a deeper freeze’ – J.P. Morgan’s Shearer – KITCO [T6]

- China’s top ETF is now gold, not stocks – Mining.com [T7]

- Warsh’s throwaway comment injects life into the debasement trade, for one day at least – MarketWatch [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. The analysis reflects the data and perspectives available as of 2026-07-07.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.