Listen to the summary

Key Data Snapshot

| Metric | Value |

|---|---|

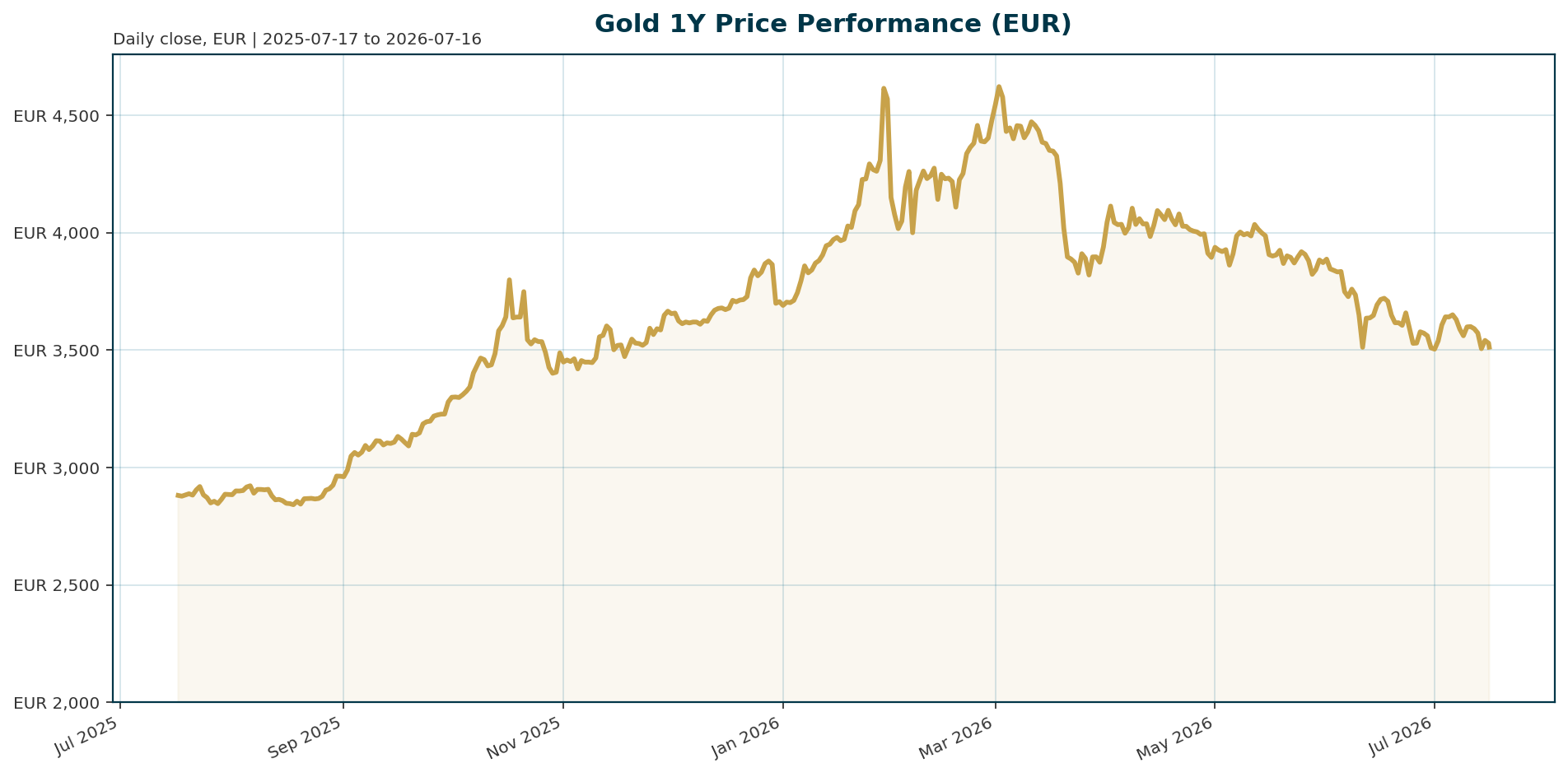

| Current Price (XAU/EUR) | 3,512.03 EUR |

| 24h Change | -0.21% |

| 200-Day Change | -9.34% |

| ATH (Jan 2026) | 4,688.32 EUR (-25.1% drawdown) |

| Market Cap | 1.58 Billion EUR |

| BTC Dominance | 56.19% |

| EUR/USD | 1.1437 |

Key Calculations: The implied USD price is approximately 4,017 USD (3,512.03 EUR * 1.1437). The Euro area real yield spread (10Y – 2Y) is 45.9 basis points.

Macro Backdrop

Risk sentiment remains neutral as equity markets exhibit divergent momentum, with the Hang Seng leading gains at 4.00% over five days while the Nikkei 225 lags at -2.03% [T5]. The rates backdrop features a mixed Euro area curve with the 10-year yield at 3.146% and the 2-year yield at 2.687%, resulting in a flattening spread of 45.9 basis points. The FX landscape is mixed, with the EUR/USD trading at 1.1437, providing a modest tailwind for EUR-denominated gold. The primary macro constraint is the Euro area AAA 10Y yield, which has risen 0.92 basis points over five days, reflecting persistent inflation pressures stemming from the global energy crisis and the Iran war. The Federal Reserve, under Chair Kevin Warsh, is preoccupied with inflation, signaling that monetary policy may tighten further before the end of the year, despite the central bank’s flexible approach to balance sheet management [T1][T3][T4].

Investment Thesis

The investment thesis for gold centers on its role as a non-sovereign reserve asset in a fragmented global financial system. Unlike rate-sensitive speculative assets, gold is accumulating due to strategic balance sheet construction rather than tactical rate bets. Central banks are prioritizing gold to mitigate counterparty risk and currency volatility, viewing it as independent of any single government’s policy. The U.S. policy environment, characterized by erratic decision-making and sanctions, has exacerbated the diversification away from the dollar, driving sovereign demand for gold as a store of value [T2][T3]. While fiscal policy remains extremely loose globally, central banks are tightening monetary policy, creating an environment where gold’s lack of yield becomes less of a penalty and its liquidity and universal acceptance become more valuable.

Bullish Drivers

- Sovereign Accumulation: Central bank buying is accelerating despite price declines. Poland is on pace to meet its 700-tonne accumulation goal, having purchased 64 tonnes year-to-date. China added 15 tonnes in May, marking its 20th consecutive month of purchases [T1][T5]. The World Gold Council reports a record 45% of central banks plan to increase holdings over the next 12 months [T2].

- Structural Demand: Reserve managers measure risk in decades, not quarters. They are building balance sheets to withstand geopolitical shocks and a multipolar world. OMFIF surveys indicate over 60% of reserve managers expect gold prices to trade between $5,000 and $6,000 an ounce over the next year [T1].

- Fiscal vs. Monetary: While central banks are tightening, fiscal policy remains loose. This divergence supports gold as a hedge against potential inflationary pressures and currency debasement [T4].

- Supply Dynamics: Russia has sold gold during ten of the past 12 months, reducing potential supply pressure on the market [T6].

Relative Positioning vs Bitcoin and Ethereum

With Bitcoin dominance at 56.19%, gold maintains its status as the primary store of value, often outperforming risk-on assets during periods of market stress. While Bitcoin rallies on improving sentiment toward AI and growth sectors, gold acts as a diversifier against equity volatility. Ethereum, as a smart contract platform, is correlated with growth narratives rather than the defensive monetary characteristics of gold. In a neutral to bearish equity environment, gold typically holds value better than digital assets, which are more sensitive to liquidity conditions.

Scenario Framework

- Base Case (Hold): The Fed maintains a hawkish hold, keeping real yields elevated but stable. Gold trades in a range between 3,500 and 3,800 EUR, supported by central bank buying which absorbs speculative ETF outflows.

- Bull Case: A shift in Fed policy or a stabilization in the energy crisis leads to a decline in real yields. Gold reclaims the 4,000 EUR mark, targeting 4,500 EUR as OMFIF price targets are met.

- Bear Case: The energy crisis intensifies, causing real yields to spike. Gold tests the 3,000 EUR support level if speculative selling accelerates alongside central bank pauses.

Valuation Discussion

Gold is currently trading at a 25% discount to its January 2026 ATH. While real yield headwinds make the current valuation expensive on an opportunity cost basis, the strategic value is supported by central bank surveys suggesting a 60% probability of $5,000-$6,000 prices within a year. The current price of 3,512 EUR reflects a market pricing in aggressive Fed tightening and a strong USD. However, if the Fed holds rates as suggested by Chair Warsh, the market may be overpricing the cost of carry, presenting a value opportunity for long-term holders.

Risks

- Real Yield Spike: Continued escalation of the Iran war could spike energy prices, driving real yields higher and increasing the opportunity cost of holding gold [T1][T4].

- Speculative Rotation: Gold ETFs saw outflows of approximately 2.1 million ounces in June. If this rotation into AI and growth sectors accelerates, price pressure could intensify [T5][T6].

- USD Strength: A break in EUR/USD support below 1.14 would exert significant selling pressure on EUR-denominated gold.

Appendix

Sources

- Poland’s central bank is buying the dip as gold’s biggest buyers aren’t backing down – KITCO [T1]

- Central banks are voting for gold with their balance sheets – KITCO [T2]

- Fed won’t hike but hold, Warsh may have started too hawkish, and U.S. policy is driving sovereign gold demand – Natixis’ Christopher Hodge – KITCO [T3]

- Have metals bottomed, and have yields peaked? Monetary and fiscal policies will determine both – CME’s Norland – KITCO [T4]

- Gold SWOT: DPM Metals delivers solid Q2 production – KITCO [T5]

- Gold and silver WARNING: The selling is not over – KITCO [T6]

Disclaimer: This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed are those of the model and do not reflect the official positions of any financial institution.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.