Listen to the summary

Key Data Snapshot

| Asset | Price (EUR) | 24h Change | 1Y Change | 200D Change | BTC Dominance |

|---|---|---|---|---|---|

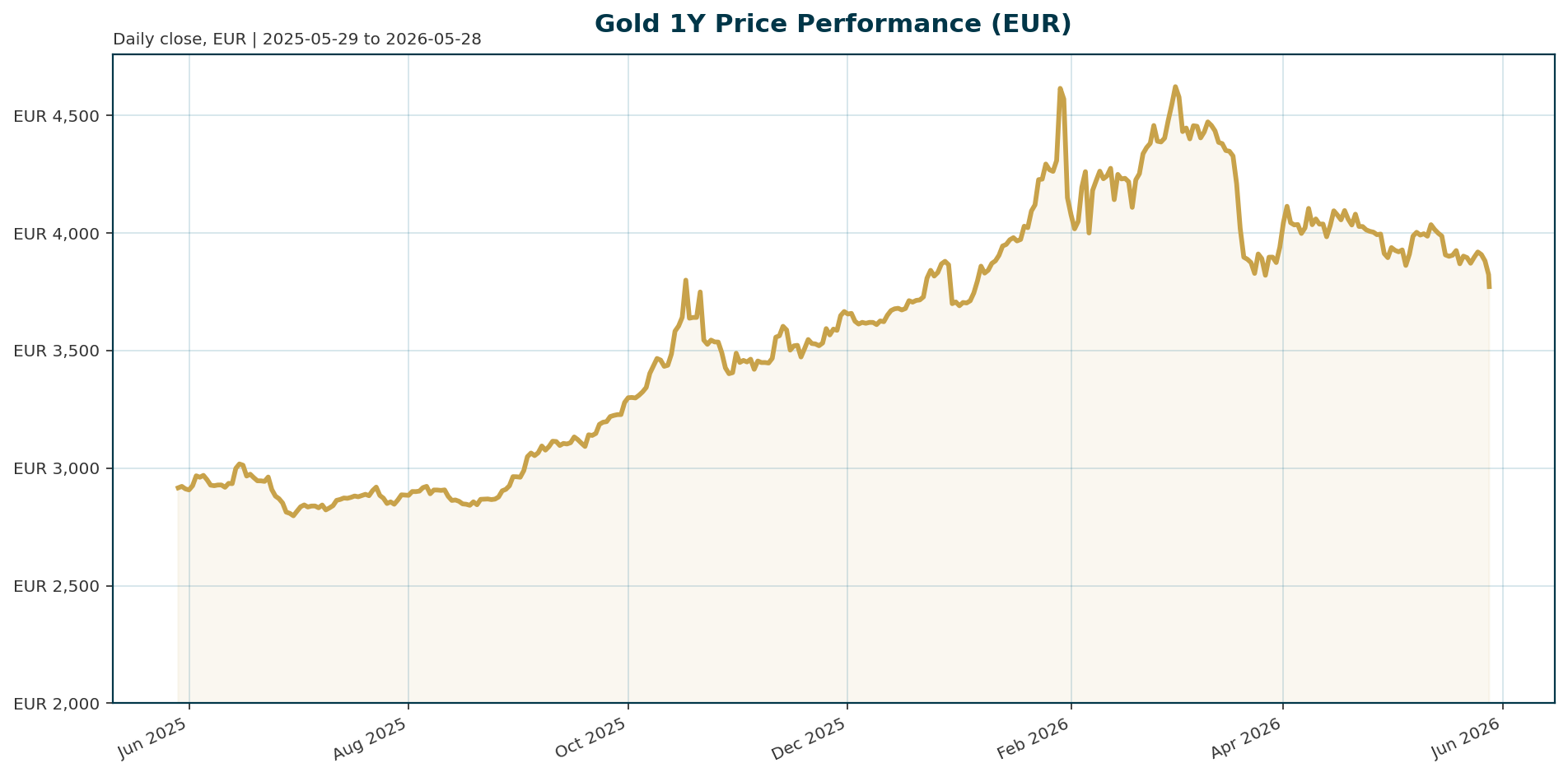

| Gold (XAU) | 3,773.48 | -2.36% | +28.54% | +9.47% | 57.71% |

Key Technical Levels: The asset is currently trading 19.5% below its January 2026 All-Time High (ATH) of 4,688.32 EUR. The 200-day moving average sits near 3,772 EUR, acting as a critical support level against the current pullback.

Macro Backdrop

The macro environment presents a dichotomy for gold. Risk sentiment remains positive, with DACH equities outperforming global peers, while the euro area 10-year yield has fallen 16.1 basis points over the past five days. However, the rates backdrop remains challenging for gold as US real yields stay elevated, and the FX backdrop is mixed with EUR/USD at 1.1646. Key observations include the ATX leading the region with a 3.13% 5-day move and the Hang Seng underperforming with a -2.68% decline.

Investment Thesis

The core thesis rests on gold’s role as a strategic wealth preservation asset amidst fiscal and geopolitical uncertainty. While rising real yields currently act as the primary headwind, analysts argue that these same forces—persistent inflation and deteriorating fiscal dynamics—may ultimately boost safe-haven demand as confidence in government bonds weakens [T1][T3]. The market is pricing in a Federal Reserve rate hike before year-end, creating a complex environment where gold must navigate both the opportunity cost of non-yielding assets and the potential for a flight to safety [T5].

Bullish Drivers

Structural demand remains robust, driven by official sector accumulation and geopolitical tailwinds. China’s central bank extended its buying streak, and Goldman Sachs raised its forecast for central bank purchases to 60 tons monthly in 2026 [T2][T4]. Additionally, Ghana mandated large-scale miners sell 30% of annual output to the central bank, signaling a global push for reserve diversification [T6]. Geopolitical risks, specifically the Strait of Hormuz crisis, continue to support the monetary-metal bid, potentially pushing the macro regime toward a stagflationary outcome historically favorable to precious metals [T5][T6].

Relative Positioning vs Bitcoin and Ethereum

Gold faces stiff competition from Bitcoin, which holds 57.7% market dominance. Despite a recent selloff where gold slipped to approximately $4,500, net ETF inflows turned positive for the first time since early April, suggesting Main Street investors remain bullish [T6][T7]. Silver has shown relative strength through the selloff, holding its 50-day moving average, which could allow silver to outperform gold if the macro regime shifts [T6].

Scenario Framework

- Scenario A (Bearish – Tightening Spike): The Fed maintains a hawkish stance, and US real yields continue to rise above 5%. This increases the opportunity cost of holding gold, potentially testing the 200-day moving average support around 3,772 EUR.

- Scenario B (Base – Stagflation): Inflation persists due to elevated oil prices, while the Fed pauses rate hikes. Gold consolidates between 3,700 and 3,900 EUR, supported by central bank buying and geopolitical tension.

- Scenario C (Bullish – Debt Crisis): Confidence in sovereign debt erodes, and bond markets stress out. Gold rallies to reclaim the ATH of 4,688.32 EUR as investors rotate into the “risk-free partnership” asset.

Valuation Discussion

Valuation is currently compressed relative to the 2026 ATH, representing a 19.5% drawdown. However, the opportunity cost of holding gold remains high with US 30-year yields maintained above 5% [T1]. The investment thesis relies on the divergence between the short-term headwind of real yields and the long-term structural demand from central banks, which is expected to accelerate despite India’s demand contraction (imports down 47% due to tax hikes) [T4].

Risks

- Real Yield Growth: Continued expansion of real yields remains the biggest barrier to precious metals, pressuring the asset’s opportunity cost [T1][T3].

- Fed Hawkishness: Markets are pricing in a 58% chance of a rate hike before year-end, which could further strengthen the USD and weigh on gold [T5].

- Geopolitical De-escalation: A resolution to the Strait of Hormuz crisis could reduce safe-haven flows and trigger a broader risk-on rotation into equities [T5][T7].

- ECB Policy: The ECB has signaled it will “do what is necessary” to tame inflation, potentially leading to rate hikes that could strengthen the EUR and complicate the FX backdrop [T8].

Appendix

Sources

- Gold prices play a good role as a shelter, silver has a large growth potential – Laodong.vn [T1]

- China’s Gold Holdings Rise Again as Central Bank Extends Buying Streak – The Jerusalem Post [T2]

- Gold, silver and the new fear behind elevated bond yields – KITCO [T3]

- Gold prices face double pressure from inflation, interest rates and new moves by India – Laodong.vn [T4]

- Gold set for weekly loss as oil-driven inflation fears boost rate-hike bets – Reuters [T5]

- Gold SWOT: Net gold ETF inflows turned positive for the first time since early April – KITCO [T6]

- Wall Street stays bearish as gold clings to $4,500, Main Street maintains bullish bias as Fed rate hike concerns mount – KITCO [T7]

- ECB ‘will do what is necessary’ to tame inflation, Bank of France governor tells CNBC – CNBC [T8]

Disclaimer: This report is AI-generated for informational purposes only and does not constitute investment advice. The content provided is based on data available as of the generation date and should not be considered as a guarantee of future performance. Investors are advised to conduct their own due diligence before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.