Listen to the summary

Key Data Snapshot

| Metric | Value |

|---|---|

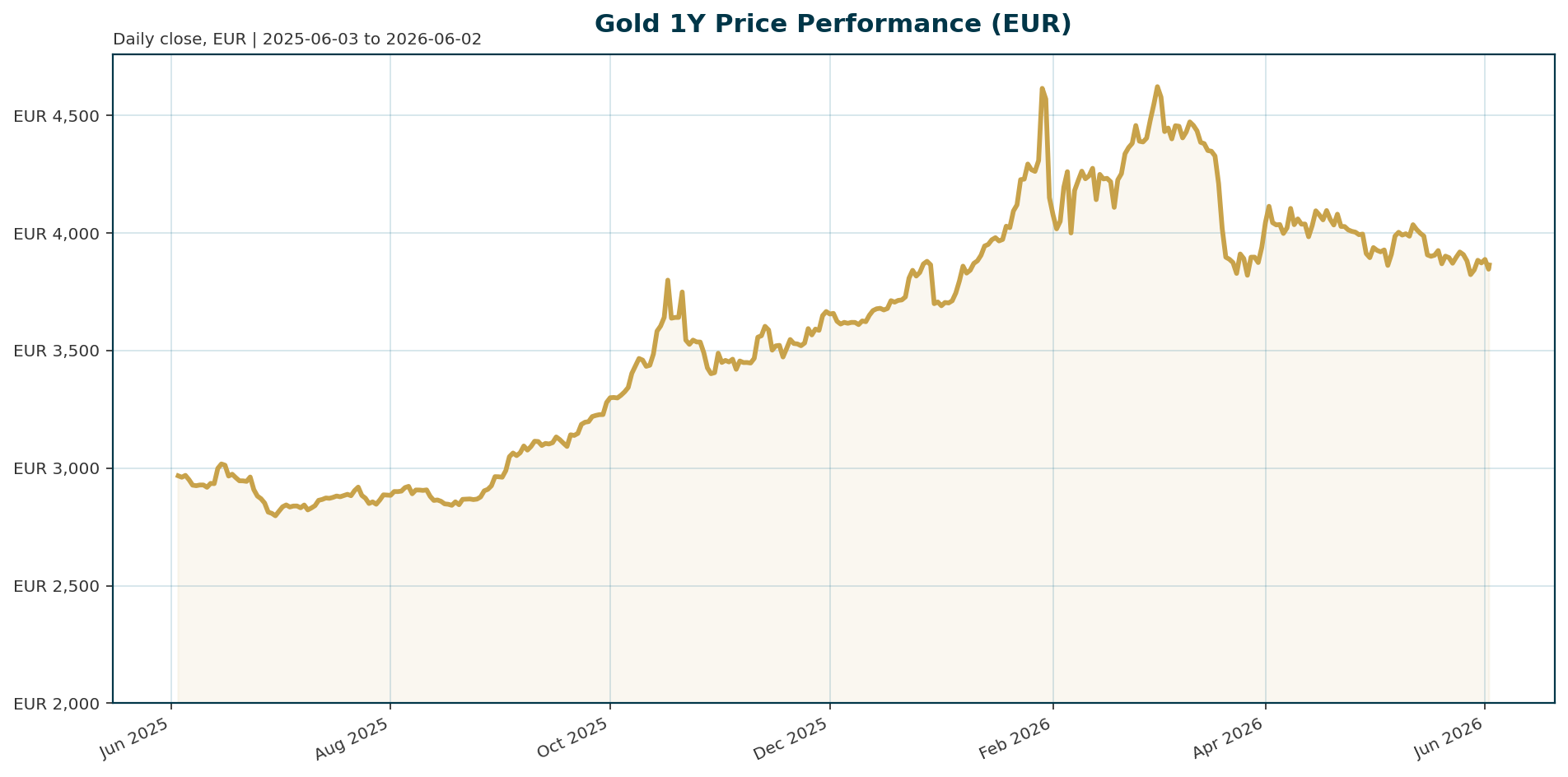

| Current Price (XAU/EUR) | 3,863.77 EUR |

| All-Time High (ATH) | 4,688.32 EUR (Jan 29, 2026) |

| ATH Drawdown | -17.58% |

| 200-Day Change | +7.19% |

| 1-Year Change | +32.29% |

| 24h Volume | 133.60 M EUR |

| BTC Dominance | 56.46% |

Calculated ATH Drawdown: (3,863.77 – 4,688.32) / 4,688.32 = -17.58%

Macro Backdrop

Risk sentiment is broadly positive with global equities rallying, yet the DACH region lags significantly behind US and Asian peers. The Euro area 10Y yield sits at 3.02%, moving higher over the past five days, while the EUR/USD pair trades at 1.1658. Key observations highlight the Nasdaq Composite leading gains while the DAX underperforms, suggesting a divergence in regional risk appetite. Euro area yields are mixed, with the 2Y yield at 2.50%, creating a complex backdrop for non-yielding assets like gold.

Investment Thesis

The long-term bull case for gold remains structurally intact despite short-term volatility. The Federal Reserve faces a “trapped” scenario where it cannot easily navigate between inflation control and sovereign debt sustainability without hurting financial stability [T3]. Ryan McIntyre of Sprott argues that regardless of whether the Fed cuts or hikes rates, gold benefits: aggressive tightening risks triggering a debt crisis, while rate cuts risk reigniting inflation. This conundrum forces investors toward hard assets. Furthermore, the weaponization of the dollar and the ongoing de-dollarization of global GDP provide a firm floor for gold prices supported by central bank accumulation [T1].

Bullish Drivers

- Central Bank Accumulation: Official sector buying remains the primary demand pillar. China extended its reserve buying streak, while Goldman Sachs raised its forecast for global central bank purchases to 60 tons per month in 2026 [T5]. Ghana also increased its domestic gold purchase mandate to 30% of output from 20% starting June 1 [T4][T6].

- ETF Inflows: Net gold ETF inflows have turned positive for the first time since early April, signaling a return of institutional support [T6].

- Supply Constraints: India’s decision to raise gold import taxes from 6% to 15% is expected to significantly reduce physical supply in the second quarter of 2026 [T5].

- Structural Inflation: Deglobalization and supply chain fragmentation are creating a more inflationary global backdrop that could persist for years, supporting the real value of gold [T3].

Relative Positioning vs Bitcoin and Ethereum

Gold is currently facing headwinds from a high-risk appetite environment, evidenced by Bitcoin dominance sitting at 56.46%. As risk-on capital flows into crypto assets, gold has seen relative underperformance recently. However, silver has shown resilience through the selloff, holding its 50-day moving average, which suggests that if the macro regime shifts toward stagflation, precious metals could outperform [T6]. Gold retains its role as the primary monetary metal, while Bitcoin absorbs a significant portion of speculative risk-on capital.

Scenario Framework

- Bull Scenario: If the Fed pivots to rate cuts and geopolitical tensions ease, gold targets reclaiming its ATH of 4,688.32 EUR. A dovish shift in Euro area yields would further support this move.

- Base Scenario: The market consolidates within a range between 3,700 EUR and 4,200 EUR. Central bank buying offsets weaker physical demand, while real yields remain suppressed due to structural debt issues.

- Bear Scenario: A renewed Fed hike cycle (41% probability of a December hike) combined with a stronger dollar could force gold to test support levels below the 200-day moving average [T7].

Valuation Discussion

Gold is currently trading at a 17.58% discount to its January 2026 ATH, despite a strong 32.29% gain over the past year. The current price of 3,863.77 EUR reflects a consolidation phase following a sharp rally. Valuation expansion is likely contingent on the Fed’s inability to normalize policy without causing financial stress. The structural case for gold is supported by elevated global debt burdens and persistent fiscal deficits in major Western economies [T7], which should continue to elevate the strategic case for hard assets.

Risks

- Technical Risk: Spot gold is approaching a potential daily close below its 200-day moving average for the first time since October 2023, which could trigger further technical selling [T4].

- Policy Risk: Markets are pricing in a 41% chance of a Fed rate hike before year-end, which would likely strengthen the dollar and create immediate headwinds for gold [T7].

- Emerging Market Reserves: Downward pressure on gold could increase if emerging market central banks draw down reserves to defend their currencies against a strong dollar [T4].

Appendix

Sources

- [T1] Gold is just taking a breath and the race is not over – Midas Discovery Fund’s Winmill – KITCO

- [T2] China’s Gold Holdings Rise Again as Central Bank Extends Buying Streak – The Jerusalem Post

- [T3] Fed trapped between inflation and debt crisis, and gold wins either way – Sprott’s McIntyre – KITCO

- [T4] Gold SWOT: China’s GFEX is exploring night trading for platinum and palladium contracts – KITCO

- [T5] Gold prices face double pressure from inflation, interest rates and new moves by India – Laodong.vn

- [T6] Gold SWOT: Net gold ETF inflows turned positive for the first time since early April – KITCO

- [T7] Gold falls as renewed US-Iran tensions dampen peace hopes, clouds interest rate outlook – KITCO

- [T8] Inflation fight again putting central bank independence under strain, policymakers say – Reuters

This report is AI-generated for informational purposes only and does not constitute investment advice. Please consult a qualified financial advisor before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.