Listen to the summary

Key Data Snapshot

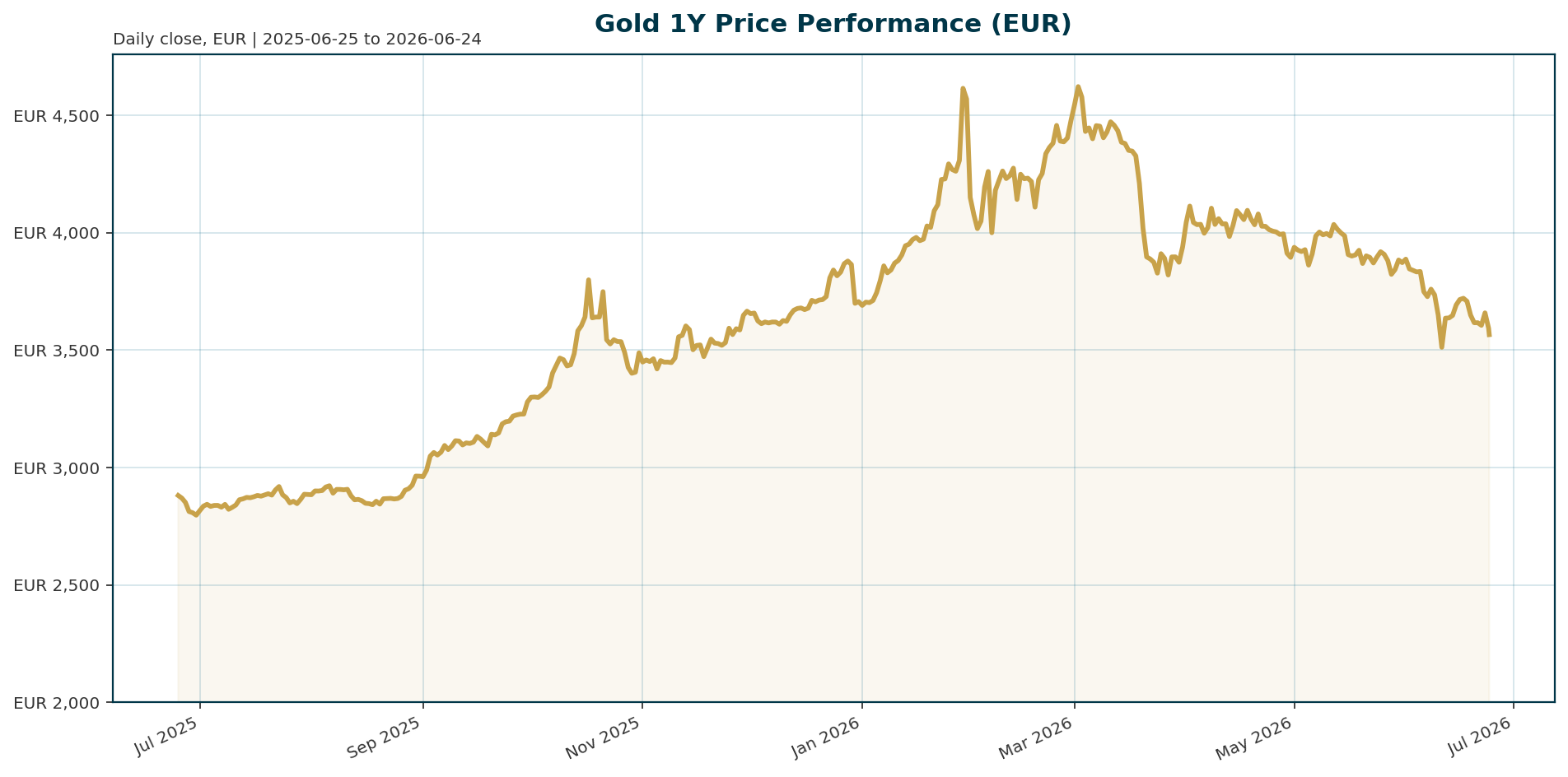

Gold (XAU) is trading at 3565.6 EUR, consolidating after a 23.9% drawdown from its January 2026 all-time high (ATH) of 4688.32 EUR. The 30-day performance stands at -8.82%, reflecting a recent pullback amidst a “higher for longer” rate environment. However, the structural demand backdrop remains exceptionally strong.

| Metric | Value |

|---|---|

| Current Price (XAU/EUR) | 3,565.60 |

| ATH (Jan 2026) | 4,688.32 (-23.9% drawdown) |

| 30-Day Return | -8.82% |

| Central Banks Planning to Buy | 45% (Record high) [T5] |

| Euro Area AAA 10Y Yield | 3.01% [market_overview] |

| EUR/USD | 1.1416 (-0.55% 5d) [market_overview] |

Structural Demand Floor Calculation: Central bank net purchasing (800-1,000+ tonnes annually) represents approximately 28.6% of global mine supply (3,500 tonnes/year), creating a baseline support independent of speculative flows [T4].

Macro Backdrop

The macro environment presents a dichotomy for gold. Risk sentiment is neutral to negative, evidenced by the Hang Seng’s -4.10% five-day performance and the DAX’s marginal -0.16% decline [market_overview]. This risk-off tone provides a baseline support for gold as a safe haven.

However, the rates backdrop is challenging. The Euro Area AAA 10Y yield sits at 3.01%, with the Euro Area 2Y yield at 2.55% [market_overview]. SocGen analysts note a “higher for longer” regime, where persistent inflation and oil-driven price shocks cap medium-term upside [T3]. The FX backdrop is mixed, with EUR/USD weakening 0.55% over five days, which offers some relief to EUR-denominated gold but is overshadowed by a firmer USD generally pressuring the metal [T8].

Investment Thesis

The investment thesis for gold has shifted from a rate-sensitive play to a structural reserve asset narrative. The primary driver is the weaponization of the US dollar and the resulting de-dollarization trend. Central banks are aggressively diversifying away from dollar-denominated assets, viewing gold as the premier hedge against currency risk and geopolitical shocks [T2], [T7].

Despite the recent price correction, this is viewed by analysts as a “reset” within a secular uptrend rather than the start of a bear market [T2]. The market is pricing in a hawkish Fed stance and easing Middle East tensions, but the underlying demand from sovereign wealth managers remains robust. Goldman Sachs maintains gold as a highest-conviction long commodity position, centered on geoeconomic uncertainty rather than rate differentials [T4].

Bullish Drivers

- Sovereign Accumulation: Record survey data indicates 45% of central banks plan to increase gold holdings, with 89% expecting global reserves to rise over the next 12 months [T1], [T5]. Gold has recently surpassed US Treasuries to become the world’s largest reserve asset.

- De-dollarization: The freezing of Russian reserves in 2022 has cemented a structural shift. Countries are actively seeking stores of value outside the US dollar and Treasury market [T2].

- Persistent Inflation: Reshoring and supply-chain realignment are reversing decades of globalization-driven disinflation, making gold a necessary hedge against structurally higher inflation [T2].

- Attractive Valuation: The current pullback offers an entry point. Analysts note that much of the downside has been priced in, and sovereign buying will likely resume as oil flows normalize [T2], [T8].

Relative Positioning vs Bitcoin and Ethereum

Gold is diverging from risk assets like Bitcoin and Ethereum. Bitcoin is trading significantly off its highs and behaving as a liquidity-sensitive risk asset, moving in tandem with broader market sentiment rather than serving as a stable store of value [T7].

Conversely, gold is increasingly being priced by different investor communities. Its role as the world’s largest reserve asset provides a structural demand floor that has no analog in the crypto market [T4], [T7]. While Bitcoin may rally on liquidity injections, gold tends to hold value during risk-off periods, making it a distinct asset class for portfolio diversification.

Scenario Framework

- Bullish Scenario (Base Case): A pivot in Fed policy or a resurgence in geopolitical tension triggers safe-haven flows. With real rates likely to remain low due to structural inflation, gold could reclaim the 4000 EUR level and target Goldman Sachs’ year-end target of 4900 EUR [T7].

- Base Case: The “higher for longer” rate regime persists. Inflation remains sticky, and the Fed stays on hold. Gold consolidates in a range between 3000 EUR and 4000 EUR, supported by central bank buying which offsets bearish rate pressure [T3], [T8].

- Bearish Scenario: A sharp de-escalation in Middle East tensions or a sudden spike in global real yields (driven by an energy shock) could trigger a deeper correction. However, the structural demand floor from central banks limits the downside, likely keeping the price above the 3000 EUR mark [T3], [T4].

Valuation Discussion

Current valuations are attractive relative to the 2026 ATH, offering a margin of safety for long-term holders. The structural demand floor created by central banks (consuming 25-30% of mine supply) acts as a price support mechanism that is distinct from speculative positioning [T4].

Valuation is also supported by the concept of negative real rates. With Euro Area 10Y yields at 3.01% and inflation expected to remain elevated into early 2027, the opportunity cost of holding gold remains low, incentivizing capital allocation to hard assets [T3], [T6].

Risks

- Higher Real Yields: Should inflation moderate faster than expected or real yields rise sharply, the opportunity cost of holding gold increases, potentially capping upside [T3].

- Strong Equity Markets: Robust equity performance, particularly in the US and Japan, continues to draw capital away from safe havens like gold [T3].

- Geopolitical De-escalation: A reduction in perceived risk could lead to a reduction in safe-haven demand, triggering a technical correction [T8].

- Supply Constraints: While central bank demand is robust, a significant expansion in mine supply or a technological shift in energy use could alter the supply-demand balance [T4].

Appendix

Sources

- Central banks are bringing gold reserves home as geopolitical risks rise – CNBC [T1]

- Gold’s pullback creates attractive entry as de-dollarization turns structural – KITCO [T2]

- Persistent inflation, oil-driven price shocks and higher-for-longer rates will cap gold’s medium-term upside – SocGen [T3]

- Why Central Bank Gold Demand Is Reshaping Global Reserves – Discovery Alert [T4]

- Record 45% of central banks plan to increase gold holdings, WGC survey finds – Shanghai Metals Market [T5]

- Gold Bull Market and Mining Stocks: A Comprehensive Investor’s Guide – Discovery Alert [T6]

- Gold, Bitcoin, And The New Safe-Haven Playbook – Forbes [T7]

- Gold’s current correction sets up second big buying opportunity – Mining.com.au [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. Always conduct your own due diligence before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.