Listen to the summary

Key Data Snapshot

| Metric | Value |

|---|---|

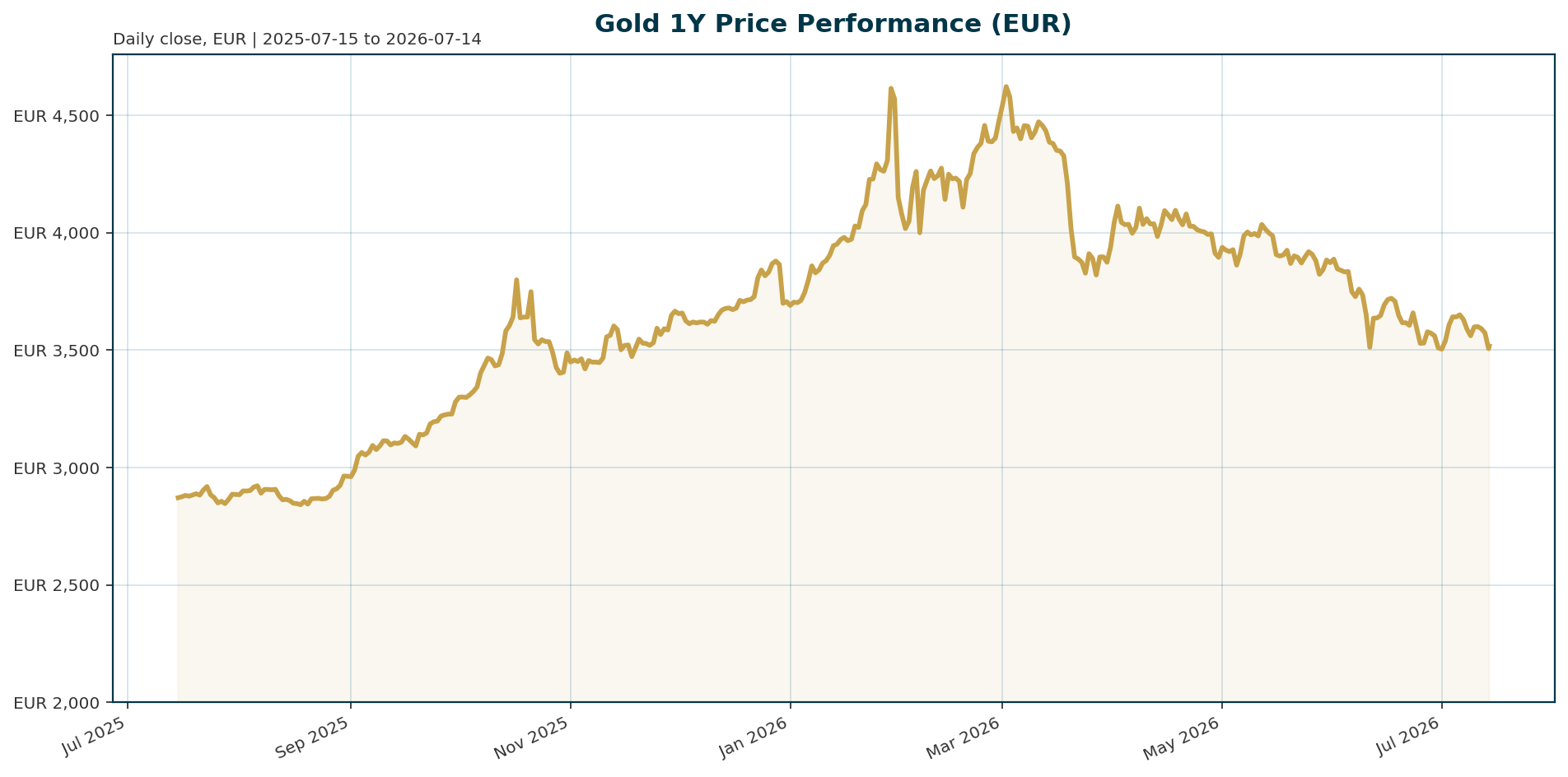

| Price (XAU/EUR) | 3,517.47 |

| All-Time High (ATH) | 4,688.32 EUR (Jan 29, 2026) |

| Drawdown from ATH | -24.97% |

| Year-to-Date (YTD) | +22.71% |

| 200-Day Return | -8.19% |

| BTC Dominance | 56.05% |

| Euro Area AAA 10Y Yield | 3.11% (+9.3bp 5d) |

| EUR/USD | 1.1426 (-0.14% 5d) |

Macro Backdrop

Risk Sentiment: Market sentiment is currently neutral with mixed equity momentum. The DAX leads as the weakest 5-day performer at -1.38%, while the Nikkei 225 shows strength at +0.37%. DACH equity indicators average -0.87% over 5 days versus 0.04% for global indicators.

Rates Backdrop: Euro area yields are mixed but generally sticky. The Euro Area AAA 10Y yield sits at 3.11%, ticking up 9.3 basis points over the last 5 days. The 2Y yield is 2.60%. The backdrop suggests real yields remain elevated, driven by persistent core inflation pressures stemming from the global energy crisis and the Iran war [T1][T3].

FX Backdrop: The EUR is under slight pressure, with EUR/USD trading at 1.1426 and down 0.14% over 5 days. This depreciation creates a headwind for XAU/EUR, as a weaker euro reduces the metal’s value in euro terms.

Key Observations: The Euro Area AAA 10Y-2Y spread is 50.9 bp. The ATX leads regional performance on a 1-month basis at +3.28%, while the Hang Seng is the weakest major index at -2.68% over 5 days.

Investment Thesis

The investment thesis for gold remains intact despite short-term technical headwinds. The core argument rests on the divergence between monetary and fiscal policy. While central banks, led by the Federal Reserve under Kevin Warsh, are tightening policy to combat inflation, fiscal policy remains extremely loose globally [T3]. This divergence supports gold’s role as a hedge against fiscal dominance and currency debasement.

However, the thesis faces immediate pressure from rising real yields. The opportunity cost of holding a non-yielding asset is increasing due to energy-driven inflation, which has pushed real bond yields higher [T1]. The market is currently pricing in this conflict, evidenced by the sharp correction in June where gold posted its largest monthly decline since 2008 [T1].

Bullish Drivers

- Central Bank Accumulation: Sovereign demand is the primary support floor. Poland is aggressively buying the dip, targeting 700 tonnes of reserves and currently holding 632.4 tonnes [T1]. China added 15 tonnes in June, marking its 20th consecutive month of purchases [T2][T4]. Global central banks added 41 tonnes in May, with 45% of surveyed banks planning to increase holdings over the next 12 months [T1][T2].

- Fed Flexibility: Fed Reserve Management Purchases (RMPs) are not on a preset course and can be adjusted based on money market conditions. This flexibility suggests the Fed could act as a buyer of last resort if market conditions tighten [T8].

- Digital Gold Potential: Tokenization of bullion could unlock new liquidity and 24/7 trading, potentially creating a structural tailwind for gold’s role in modern financial markets [T6].

- Geopolitical Risk: The war with Iran and a multipolar global financial system reinforce gold’s appeal as an independent store of value free of counterparty risk [T2].

Relative Positioning vs Bitcoin and Ethereum

Gold is currently facing a rotation of speculative capital away from traditional safe havens toward growth assets and cryptocurrencies. Bitcoin dominance is high at 56.05%, indicating a significant share of risk-on capital is flowing into digital assets rather than gold [T5].

While gold is increasingly viewed as “digital gold” due to tokenization trends [T6], it is currently underperforming Bitcoin in terms of speculative momentum. ETF data shows the largest weekly gold outflows since 2018, driven by investors rotating into AI and growth sectors [T5]. This suggests that while gold retains its fundamental monetary value, it is losing short-term speculative favor to the crypto ecosystem.

Scenario Framework

- Scenario 1: Stagflation & CB Support (Base Case): Real yields remain sticky due to energy costs. Gold consolidates around current levels (3,500-4,000 EUR) supported by robust central bank buying. The Euro remains weak, keeping XAU/EUR elevated relative to USD peers.

- Scenario 2: Reflation & Fed Pivot (Bullish): If the Fed signals a rate cut, real yields fall sharply. Combined with a strengthening Euro, XAU/EUR rallies aggressively, potentially targeting 4,500 EUR as central bank surveys suggest a target range of $5,000-6,000/oz [T1].

- Scenario 3: Hard Landing & Rate Spike (Bearish): A sharp deterioration in global risk sentiment triggers a flight to the US dollar. Euro area yields spike, and real yields rise. Gold tests support levels below 3,000 EUR as ETF outflows accelerate and Russian central bank selling continues [T7].

Valuation Discussion

Valuation metrics suggest gold is attractive relative to its recent peak but expensive relative to current real yields. The metal is down 24.97% from its January 2026 ATH of 4,688.32 EUR [T1]. On a 200-day basis, the return is negative at -8.19%, indicating the market has not fully priced in the recent macro tightening.

However, the long-term narrative remains compelling. Reserve managers surveyed by OMFIF expect gold prices to trade between $5,000 and $6,000 an ounce over the next year [T1]. This implies significant upside potential from current levels if the market corrects for the long-term monetary value of gold versus short-term yield pressure.

Risks

- Real Yield Spike: A resurgence in energy prices or hawkish central bank messaging could push real yields higher, increasing the opportunity cost of holding gold [T1].

- Speculative Capitulation: Continued ETF outflows, such as the 2.1 million ounces sold in June, could lead to a self-fulfilling price decline [T7].

- Russian Selling: Russia has sold gold in ten of the past 12 months, and if this trend accelerates, it adds supply pressure to the market [T7].

- Euro Strength: A sudden strengthening of the EUR/USD pair would directly weigh on the XAU/EUR price.

Appendix

Sources

- [T1] Poland’s central bank is buying the dip as gold’s biggest buyers aren’t backing down – KITCO

- [T2] Central banks are voting for gold with their balance sheets – KITCO

- [T3] Have metals bottomed, and have yields peaked? Monetary and fiscal policies will determine both – CME’s Norland – KITCO

- [T4] China gold reserves rise most since 2023 even as bullion tumbles – KITCO

- [T5] Gold SWOT: DPM Metals delivers solid Q2 production – KITCO

- [T6] Digital gold could unlock bullion’s next bull market by solving liquidity challenges, but trust remains a challenge – KITCO

- [T7] Gold and silver WARNING: The selling is not over – KITCO

- [T8] Fed’s Perli reiterates flexible path of reserve management buying – KITCO

This report is AI-generated, for informational purposes only, and does not constitute investment advice. Readers should conduct their own due diligence before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.