Listen to the summary

Key Data Snapshot

| Metric | Value | Change (24h) |

|---|---|---|

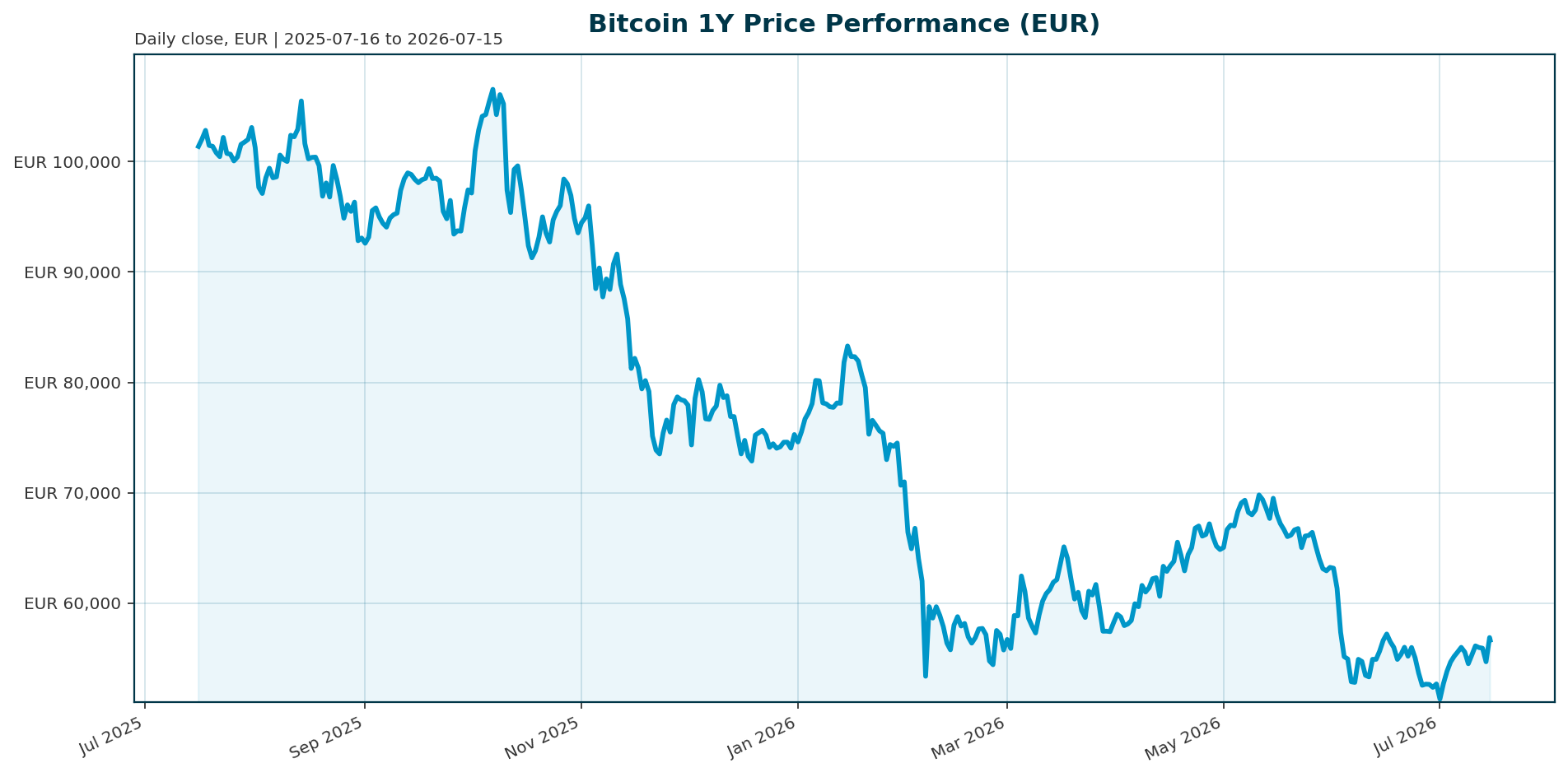

| Price (EUR) | 56,648.00 | +3.27% |

| Market Cap (EUR) | 1.136 T | +3.28% |

| 24h Volume (EUR) | 26.2 B | N/A |

| BTC Dominance | 56.33% | N/A |

| ATH (EUR) | 107,662.00 | -47.38% |

| YTD Change | -44.07% | N/A |

Market Setup

Risk sentiment is neutral to positive, supported by moderately positive equity momentum in the DACH region where the ATX leads with a 1-month gain of 3.94% while the S&P 500 lags at 0.81% over 5 days. The rates backdrop is mixed with Euro area AAA 10Y yields at 3.12% and the FX landscape showing EUR/USD weakness at 1.1423. Key observations include the Hang Seng leading regional strength at 2.60% over 5 days and a divergence in DXY technicals that could provide macro relief for risk assets. Despite this macro backdrop, Bitcoin is navigating a challenging environment defined by the longest losing streak since 2022, as institutional capital rotates aggressively into AI equities [T1][T6].Investment Thesis

Bitcoin is currently in a transitional phase, trading at a significant discount to its October 2025 all-time high while consolidating above the 60,000 EUR floor. The primary investment thesis rests on the transition from a speculative asset to a regulated financial instrument, driven by the potential passage of the U.S. Clarity Act. While current capital flows remain negative due to regulatory uncertainty and AI rotation, structural adoption indicators persist, particularly in the UK where the FCA and Bank of England have finalized rules to facilitate institutional crypto adoption [T2][T4][T5]. The thesis posits that the current price action represents a capitulation phase where long-term holders absorb supply amidst short-term outflows, setting the stage for a re-rating once regulatory guardrails are established.Bullish Drivers

The primary catalyst for a potential breakout is the U.S. regulatory framework. The Senate Banking and Agriculture Committees are finalizing a merged CLARITY Act draft, which a former Credit Suisse risk head argues is the ultimate catalyst for a new bull market driven by institutional FOMO [T4][T5]. Technically, Bitcoin has reclaimed the Ichimoku cloud, and ETH/Altcoin rotation is strengthening, suggesting a broader market rotation back into crypto assets [T6]. Additionally, a potential reversal in the DXY could ease USDJPY pressure and support risk assets, while the UK regulatory clarity provides a structural tailwind that contrasts with the uncertainty in the U.S. market [T2].Relative Positioning vs Gold and Ethereum

Bitcoin currently holds a dominant position in the crypto market with a 56.33% share, but its relative strength against traditional safe havens is waning. Gold has printed a bullish divergence against Bitcoin, suggesting that BTC may be lagging in risk-off environments or failing to act as a traditional hedge currently [T6]. Meanwhile, Ethereum rotation is strengthening, with ETH.D/SOL.D remaining constructive, which poses a risk to Bitcoin dominance if the smart contract narrative outperforms the store-of-value narrative in the near term [T6].Scenario Framework

- Base Case (60% probability): The Clarity Act fails or is delayed due to political gridlock. Bitcoin consolidates between 50,000 and 65,000 EUR. Institutional inflows remain muted, and miners continue to deleverage, but the asset maintains its 60,000 EUR floor.

- Bull Case (30% probability): The Clarity Act passes, unlocking massive institutional capital. Bitcoin targets 100,000 EUR, driven by a “fear of missing out” dynamic as allocators rush to gain exposure [T4].

- Bear Case (10% probability): Regulatory crackdown or macro recession triggers a breakdown below 50,000 EUR. Continued selling from miners and ETF outflows accelerate, leading to a deeper correction.

Valuation Discussion

Bitcoin is currently trading at a deep discount to its peak, sitting at approximately 52.6% of its all-time high. The market cap to 24h volume ratio is approximately 43:1, indicating high liquidity and deep order books despite outflows. The fixed supply cap of 21 million coins provides a deflationary floor, but current valuation is heavily influenced by demand-side sentiment regarding regulatory clarity rather than intrinsic utility metrics.Risks

The most significant risk is the failure of the Clarity Act, which would leave institutional capital in the “sidelines” and potentially trigger a renewed bear market [T4]. Continued capital rotation from crypto into AI equities remains a headwind, evidenced by the largest quarterly ETF outflows on record [T1][T3]. Furthermore, miner deleveraging poses a specific supply shock risk, as seen with BitFuFu selling 184 BTC in July [T7]. Finally, macro headwinds from Euro area yield increases or persistent EUR/USD weakness could impact the EUR-denominated valuation of the asset.Appendix

Sources

- Signs of life?: State of Crypto – CoinDesk [T1]

- The UK has finally shown it’s serious about crypto – CoinDesk [T2]

- Crypto SWOT: Kraken is pursuing a full European banking license. – KITCO [T3]

- Bitcoin’s ‘Ultimate Catalyst’ Predicted To Spark A $10 Trillion ‘FOMO’ Price Boom – Forbes [T4]

- New CLARITY Act Draft Expected Next Week as Senate Banking & Agriculture Committees Merge Text – CoinGape [T5]

- Bitcoin reclaims the cloud as Ethereum and Altcoin rotation strengthen – KITCO [T6]

- Singapore-listed bitcoin mining company BitFuFu sells 184 BTC, currently holds 1,671 BTC – Bitget [T7]

This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed herein are those of the AI model GLM 4.7 Flash and do not reflect the official positions of any financial institution or regulatory body.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.