Listen to the summary

Key Data Snapshot

| Asset | Symbol | Price (EUR) | 200d Return | Key Metric |

|---|---|---|---|---|

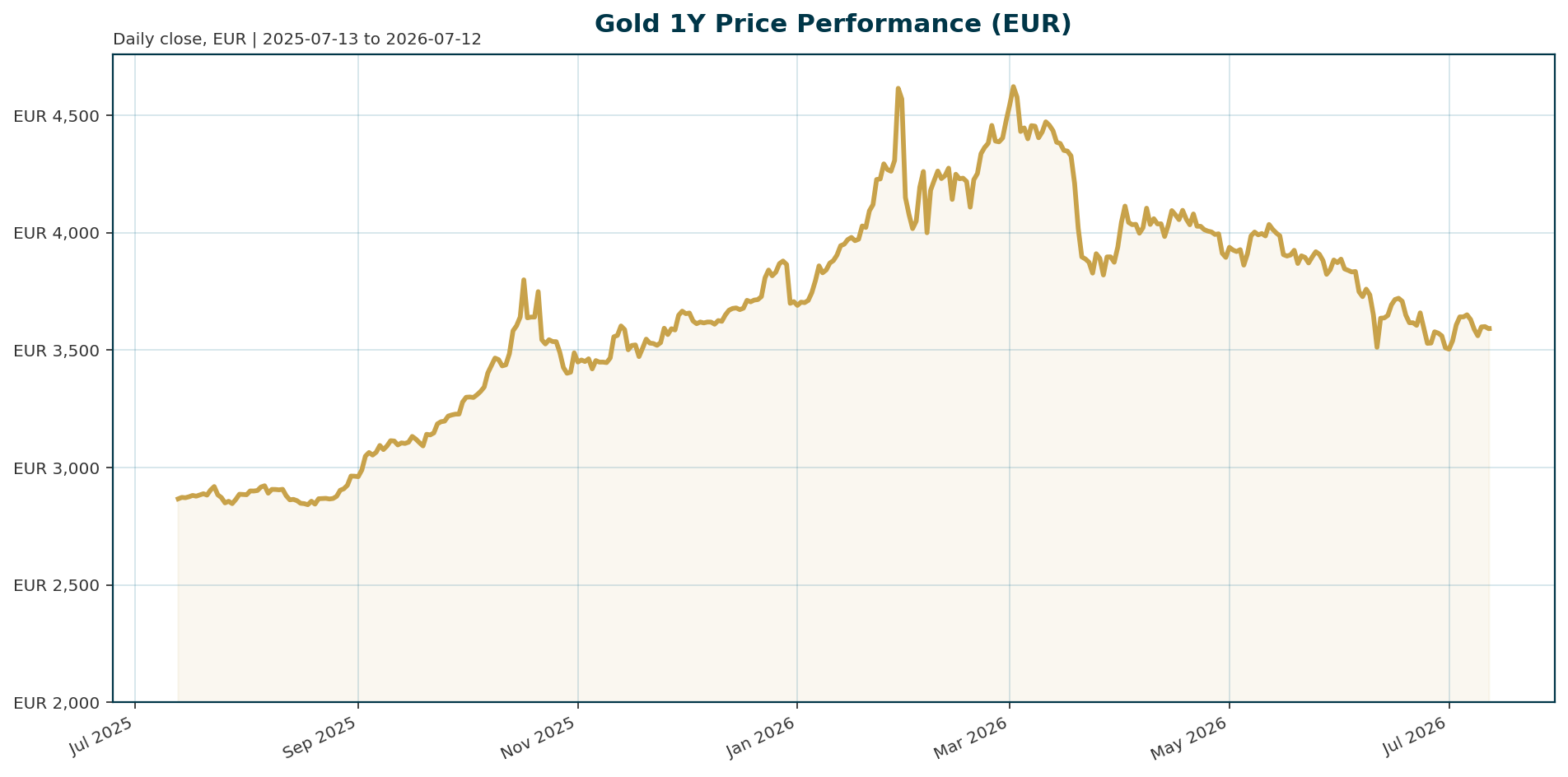

| Gold | XAU | 3591.65 | -6.18% | Central Bank Net Buys (May): 41 tonnes |

| Gold | XAU | 3591.65 | -23.39% (vs ATH) | Euro Area 10Y Yield: 3.13% |

| Gold | XAU | 3591.65 | -0.79% (30d) | Volume 24h: 31.5M EUR |

Macro Backdrop

Risk sentiment is neutral to positive globally, yet the Euro area exhibits distinct divergence. The Hang Seng leads with a strong 5-day move of 2.37%, while the DAX lags significantly at -2.91% [T1][T2]. The rates backdrop is tightening, with the Euro Area AAA 10Y yield rising to 3.13% over the last 5 days, creating headwinds for the non-yielding metal. The EUR/USD pair is trading at 1.1443, showing mixed performance against major peers. Despite the DACH equity lagging, the rising yields suggest a challenging environment for Gold’s carry trade appeal [T3][T4].

Investment Thesis

The core thesis for Gold rests on structural demand from sovereigns seeking to de-dollarize and hedge against geopolitical fragmentation. While cyclical headwinds from rising real yields and a Fed pivot pause are pressuring prices, the long-term narrative of a multipolar financial system favors Gold’s monetary characteristics [T2][T8]. Investors are shifting from an “easy money” narrative to a “rates stay high” environment, which is structurally bearish for the spot price in the near term. However, the persistent accumulation by central banks suggests that the current price dip represents a buying opportunity for institutional balance sheet managers rather than a trend reversal [T1][T5].

Bullish Drivers

- Sovereign Accumulation: Central banks remain the primary buyers of last resort. Poland increased reserves by over 100 tonnes last year and is on pace to meet its 700-tonne target, while China added 15 tonnes in June, marking its 20th consecutive month of purchases [T1][T4].

- Survey Data: The World Gold Council reported a record 45% of central banks plan to increase holdings over the next 12 months, while OMFIF survey data shows over 60% of reserve managers expect gold prices to trade between $5,000 and $6,000 an ounce [T1][T2][T5].

- Geopolitical Inflation: Persistent inflation pressures stemming from the global energy crisis and the Iran war are keeping real bond yields elevated, which paradoxically supports Gold as a hedge against currency debasement rather than a yield play [T1][T3].

Relative Positioning vs Bitcoin and Ethereum

Gold is currently underperforming risk assets, with Bitcoin dominance sitting at 56.3%. The YTD performance of Gold is negative (-0.79% over 30 days), contrasting with the strong performance of global equities and digital assets, indicating a rotation away from traditional safe havens toward high-beta assets [T5]. However, in a crisis scenario, Gold would likely reassert its dominance as the primary store of value due to its institutional acceptance and lack of counterparty risk, unlike crypto assets [T2].

Scenario Framework

- Base Case: Euro area yields continue to rise toward 3.5%, maintaining pressure on Gold. The price consolidates within the 3400-3800 EUR range as central banks absorb supply. The DAX remains weak, supporting Gold as a defensive diversifier.

- Bull Case: A resurgence in geopolitical risk or a surprise pivot in Fed policy (unlikely given current signals) could trigger a retest of the January 2026 ATH of 4688.32 EUR. Central bank buying volume accelerates, pushing prices toward the $5,000-$6,000 range forecast by OMFIF [T1][T5].

- Bear Case: If real yields spike above 4% due to sticky inflation, Gold faces significant downside. Continued ETF outflows (2.1 million ounces sold in June) could push prices toward the 3000 EUR psychological support level [T6].

Valuation Discussion

Gold is trading at a 23.4% discount to its January 2026 all-time high of 4688.32 EUR. The 200-day return of -6.18% indicates the asset is in a downtrend, technically in a correction phase [T1]. However, compared to the negative performance of DACH equities (-2.91% for the DAX) and the rising opportunity cost of capital, Gold appears attractively priced for long-term holders despite the short-term yield drag.

Risks

- Rising Real Yields: The primary headwind remains the Euro area 10Y yield rising to 3.13%, which increases the opportunity cost of holding a non-yielding asset [T3].

- ETF Outflows: Investors sold approximately 2.1 million ounces in June, contributing to the price decline. CPM Group warns that further selling could persist if prices do not break below $4,000 [T6].

- Fed Tightening: Fed Chair Kevin Warsh has signaled that monetary policy could tighten further, contradicting the previous “rate cut” narrative that drove the previous run-up [T1][T7].

Appendix

Sources

- Poland’s central bank is buying the dip as gold’s biggest buyers aren’t backing down – KITCO [T1]

- Central banks are voting for gold with their balance sheets – KITCO [T2]

- Have metals bottomed, and have yields peaked? Monetary and fiscal policies will determine both – CME’s Norland – KITCO [T3]

- China gold reserves rise most since 2023 even as bullion tumbles – KITCO [T4]

- China’s top ETF is now gold, not stocks – Mining.com [T5]

- Gold and silver WARNING: The selling is not over – KITCO [T6]

- Fed’s Perli reiterates flexible path of reserve management buying – KITCO [T7]

- Climate acts vs central bank acts – the power of arm’s length distance – Nature [T8]

This report is AI-generated, for informational purposes only, and does not constitute investment advice. The views expressed herein are those of the author and do not reflect the official policy or position of GLM 4.7 Flash or Venice.ai.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.