Key Data Snapshot

| Asset | Symbol | Price (EUR) | 24h Change | 30d Change | 1y Change | ATH | ATH Drawdown |

|---|---|---|---|---|---|---|---|

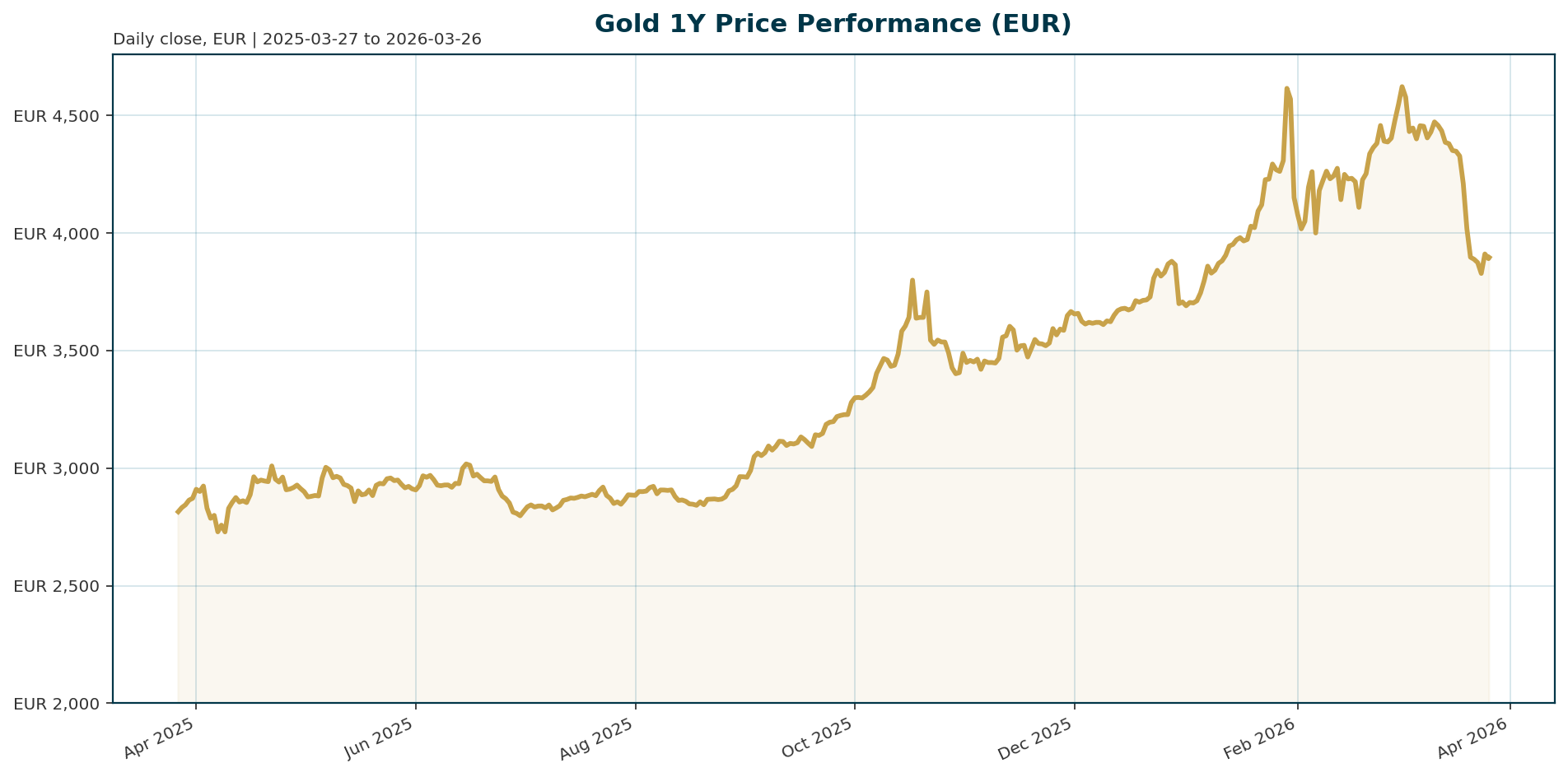

| Gold | XAU | 3,897.22 | -0.92% | -11.59% | +38.86% | 4,688.32 | -16.69% |

Gold is currently correcting from an all-time high of 4,688.32 EUR, trading at 3,897.22 EUR. The recent 30-day decline of 11.59% marks a significant pullback from the 200-day gain of 26.20%, bringing the asset into a volatile correction phase.

Macro Backdrop

The immediate macro environment is defined by a hawkish pivot from major central banks. The Federal Reserve projects rates to decrease to 3.4% by year-end, but markets are increasingly pricing in a “higher-for-longer” stance due to sticky inflation [T1].

Elevated energy prices driven by the Middle East conflict have fueled inflation concerns, pushing real yields higher. As nominal rates rise faster than inflation expectations, the opportunity cost of holding non-yielding gold increases, capping the upside [T1][T6]. The European Central Bank has maintained current rates, adding to the restrictive monetary backdrop [T2].

Investment Thesis

Despite short-term noise from real yield headwinds, the long-term investment thesis remains robust. The primary driver is the unsustainable level of global debt, which central banks will eventually be forced to address through monetary easing [T2].

Gold serves as a critical hedge against de-dollarization and geopolitical fragmentation. While the recent 15% decline since the Iran conflict began tarnished its reputation as a haven, historical patterns suggest this is a technical correction rather than a trend reversal [T8]. The asset remains up over 50% in the past year, retaining its status as a primary store of value.

Bullish Drivers

Central bank accumulation remains the strongest fundamental pillar. Global central banks are firm buyers, with new entrants including Guatemala, Indonesia, and Malaysia entering the market [T7].

Specific demand drivers include Turkey’s aggressive accumulation of approximately $135 billion in reserves to defend the lira [T5] and established buyers like China and Russia maintaining reserves exceeding 2,300 tonnes each [T3]. The World Gold Council expects central bank buying to slow to 850 metric tons this year but notes that demand remains elevated compared to pre-2022 levels [T7].

Relative Positioning vs Bitcoin and Ethereum

Gold has significantly outperformed the broader crypto market over the last year with a 38.86% return. However, during periods of acute geopolitical risk aversion, gold has underperformed traditional safe havens like the US dollar [T6].

Crypto assets tend to be more sensitive to risk-on/off sentiment shifts. While gold failed to secure lasting safe-haven status during the recent escalation of the Iran conflict, its long-term correlation with risk assets has weakened compared to the 2008 and 2020 crises [T8].

Scenario Framework

- Bull Case: Inflation cools due to easing energy prices, allowing the Fed to cut rates to 3.4%. Real yields decline, removing the primary headwind and triggering a re-rating of gold.

- Base Case: Inflation remains sticky due to energy constraints. Central banks maintain restrictive policies (“higher for longer”). Gold trades in a range, consolidating losses from the recent 16.7% drawdown.

- Bear Case: The Middle East conflict deepens, causing a severe energy shock. Central banks sell gold reserves to fund defense and energy expenditures (“piggy bank” usage), while real yields spike, pushing gold toward the 3,000 EUR support level.

Valuation Discussion

Current levels represent a deep correction but remain within a multi-year bull market. The asset is down 16.7% from its January peak but is still up 26.2% over the last 200 days.

Valuation is attractive relative to the 200-day moving average trend. However, the recent margin call-related selling observed in the rout to 4,340 EUR highlights that liquidity is drying up in the short term [T7]. The market is pricing in significant inflation risk, which keeps the discount to ATH wider than historical averages.

Risks

- Real Yield Risk: A sustained rise in real yields due to sticky inflation could trigger a prolonged bear market for gold [T1][T6].

- Central Bank Profit-Taking: Central banks may begin selling gold to fund increased energy and defense expenditures, reducing net demand [T8].

- Geopolitical Shock: Escalation in the Middle East could force resource-poor nations to liquidate reserves, exacerbating the selloff [T5][T8].

- Liquidity Crunch: Margin call selling pressure could accelerate the current downtrend if price levels breach key support zones [T7].

Appendix

Sources

- Gold, silver hit one-month lows on hawkish Fed: will downtrend deepen? – CryptoRank [T1]

- Gold pullback offers profit opportunity as debt risks grow, says analyst – Invezz [T2]

- Central banks’ gold buying momentum carries into 2026 – Mining.com [T3]

- Central banks’ gold buying momentum carries into 2026 – Bitget [T4]

- Turkey eyes $135 billion gold reserves for lira defense – Mining.com [T5]

- The charts to watch in tech, gold and emerging market stocks as volatility persists – CNBC [T6]

- Additional central banks to buy gold on geopolitical risks, WGC says – KITCO [T7]

- Gold Becomes More Useful as a Piggy Bank Than a Haven – Bloomberg.com [T8]

Disclaimer: This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed herein are those of the author and do not necessarily reflect the views of altii or its affiliates. Readers should conduct their own research and consult with a qualified financial advisor before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.