Listen to the summary

Key Data Snapshot

| Metric | Value | Change (24h) |

|---|---|---|

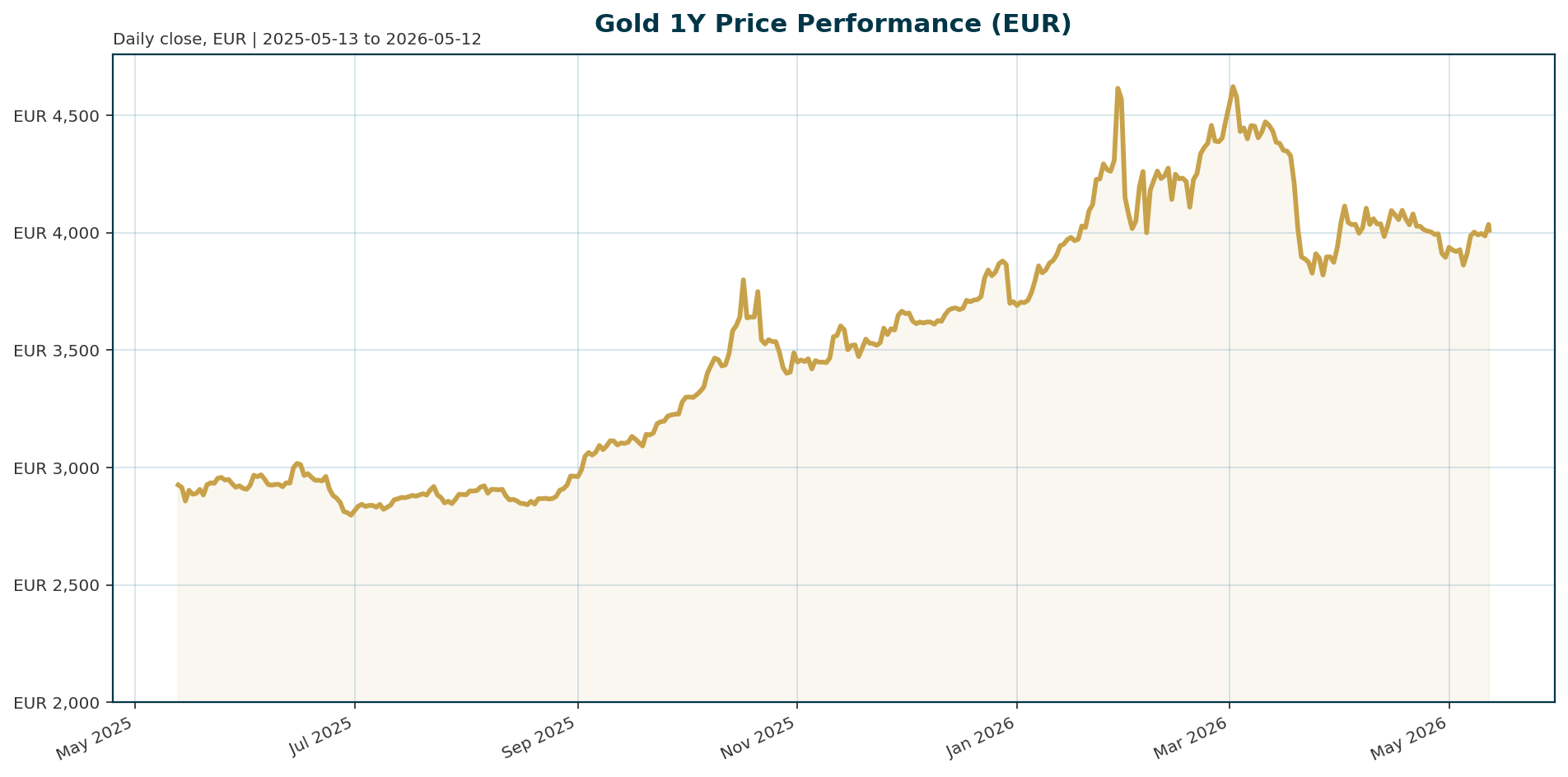

| Spot Price (EUR) | 4,011.16 | +0.97% |

| 1-Year Change | +37.24% | — |

| 200-Day Change | +13.21% | — |

| ATH (Jan 2026) | 4,688.32 | -14.56% |

| ATL (Nov 2019) | 1,265.28 | +216.57% |

| BTC Dominance | 58.26% | — |

Gold is trading 13.21% above its 200-day moving average but remains 14.56% below its January 2026 all-time high.

Macro Backdrop

Risk sentiment is broadly positive, though DACH equities lag global markets with the DAX down 0.21% over five days. Euro area yields are mixed, with the 10-year yield holding at 3.05% while FX markets remain choppy. Key observations highlight Nikkei strength at 5.40% versus DAX weakness, and EUR/USD stability at 1.1772. This divergence suggests investors are rotating into specific regional leaders while remaining cautious on the broader European equity landscape.

Investment Thesis

The investment thesis for gold centers on the structural shift in reserve management and the dual role the metal plays during periods of global stress. While gold currently serves as a critical source of dollar liquidity for stressed nations like Turkey and Gulf states [T3], it is simultaneously acting as a hedge against potential policy errors by central bankers [T4]. The core argument is that despite short-term volatility driven by funding needs, the long-term trend of de-dollarization and central bank diversification remains intact, supported by BRICS+ demand [T2].

Bullish Drivers

- Central Bank Accumulation: Major economies, including China, continue to buy the dip in gold, reinforcing the trend of reserve diversification away from the US dollar [T1][T5].

- De-Dollarization: The shift from dollar reserves to gold is described as a trend rather than a prediction, with BRICS+ demand potentially driving the entire market higher [T2].

- Attractive Bond Yields: Strategists note that bond markets are mispricing future rate hikes and that the yield side of the ledger is attractive, supporting a wait-and-see approach that favors gold [T7].

- Primary Alternative: Gold is increasingly viewed as the primary alternative to the US dollar, with price targets above $6,000/oz cited by some analysts [T2].

Relative Positioning vs Bitcoin and Ethereum

Gold maintains its status as the premier institutional reserve asset, evidenced by Bitcoin’s dominance sitting at 58.26%. While crypto assets capture speculative capital, gold remains the “hard” asset of choice during periods of systemic dollar stress, offering superior liquidity and stability compared to volatile digital assets. The current macro environment, characterized by mixed Eurozone yields and geopolitical friction, favors the stability of gold over the high-beta nature of cryptocurrencies.

Scenario Framework

- Base Case (Consolidation): Central banks pause rate hikes, keeping Euro area 10-year yields stable around 3.05%. Gold consolidates around 4,000 EUR, supported by ongoing central bank buying.

- Bull Case (Breakout): Euro yields fall further due to persistent inflation or growth concerns, triggering a flight to safety. Gold breaks its January 2026 ATH, targeting 4,500+ EUR.

- Bear Case (Correction): Dollar liquidity improves significantly as energy disruptions in the Strait of Hormuz ease, reducing the need for gold as a funding source. Central banks stop buying, leading to a correction toward 3,500 EUR.

Valuation Discussion

Current valuation appears attractive relative to the 200-day trend, which sits at +13.21%. However, the price is stretched from the January 2026 all-time high of 4,688.32 EUR, currently trading at a discount of 14.56%. Given the sensitivity of gold to real yields and dollar funding conditions, the current discount offers a favorable entry point for long-term holders betting on the continuation of the de-dollarization trend.

Risks

- Sovereign Liquidity Needs: Gold is currently functioning as a funding source for Turkey and Persian Gulf states facing dollar shortages. If energy disruptions ease, this demand could reverse sharply [T3].

- Policy Mistake Risk: Central bankers are on the verge of “policy mistake territory,” and a premature pivot in monetary policy could introduce volatility into the markets [T4].

- Real Yield Pressure: CPI risk is lifting yields, increasing the opportunity cost of holding non-yielding assets like gold [T6].

Appendix

Sources

- Central banks are still hungry for gold – KITCO [T1]

- Global gold demand drives Canada’s trade into surplus, helps mitigate economic uncertainty – KITCO [T2]

- Why Safe Haven Gold Is Falling Despite The War In Iran – Yahoo News Malaysia [T3]

- Central banks ‘on verge of policy mistake territory’: Strategist – CNBC [T4]

- China and other central banks continue to buy the dip in gold – KITCO [T5]

- Spot silver surges, gold firms as CPI risk lifts yields – Kitco PM Report – KITCO [T6]

- 3 ways the pros are trading markets right now — including a mistake one says bond traders are making – CNBC [T7]

- Markets are overlooking a growth slowdown, which is a looming concern: Azimut – CNBC [T8]

Disclaimer: This report is AI-generated for informational purposes only and does not constitute investment advice. The views expressed herein are those of the AI assistant and do not reflect the official positions of any financial institution. Readers should conduct their own research and consult with a qualified financial advisor before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.