Listen to the summary

Key Data Snapshot

| Metric | Value |

|---|---|

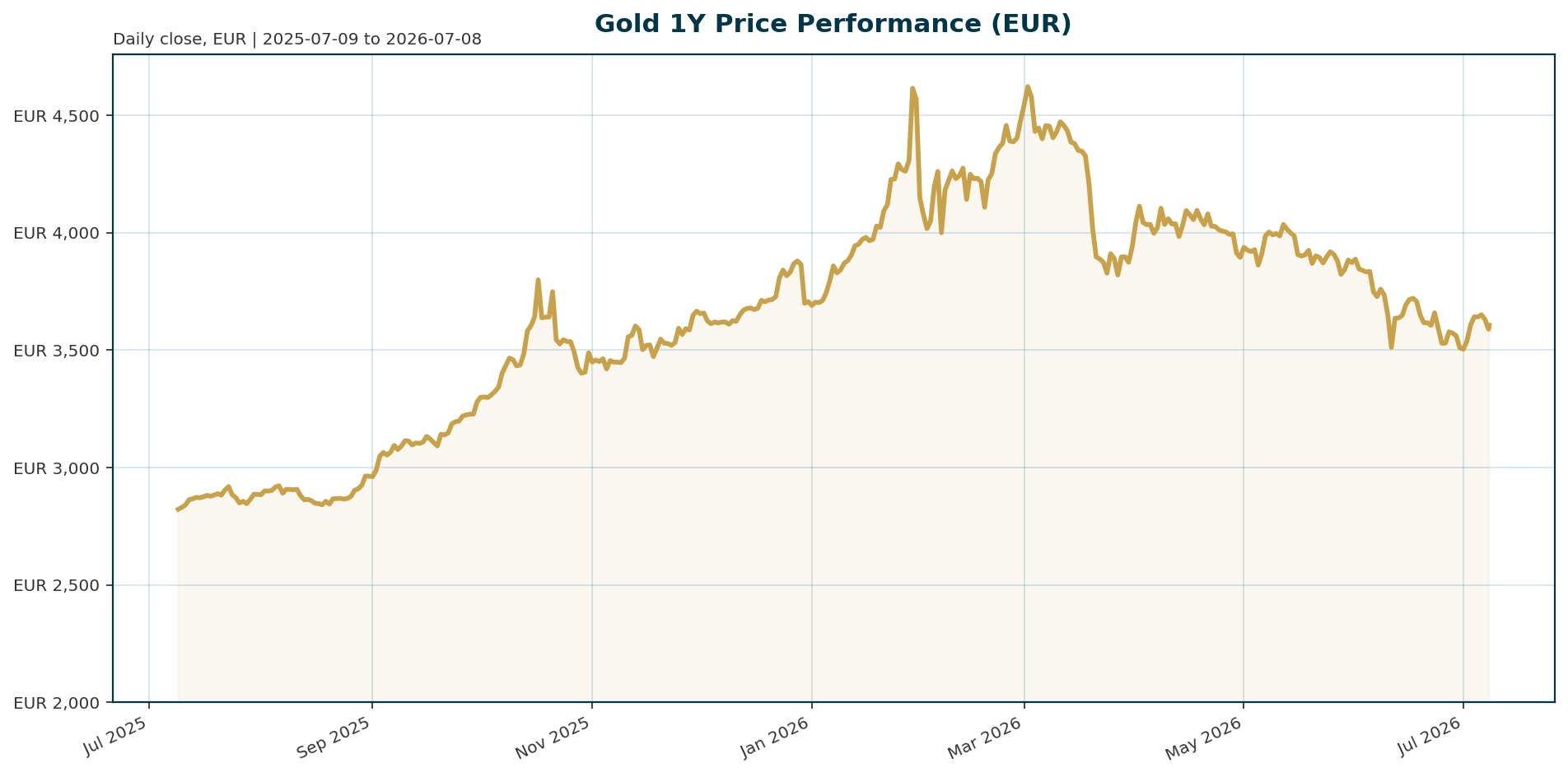

| Current Price (XAU/EUR) | 3,605.92 |

| 30-Day Performance | -3.45% |

| 1-Year Performance | +26.70% |

| All-Time High (ATH) | 4,688.32 (Jan 29, 2026) |

| ATH Drawdown | -23.08% |

| Central Bank Net Purchases (May) | 41 tonnes |

| PBOC Gold Reserves (June) | +15 tonnes (20th consecutive month) |

| Implied USD Price | ~4,125.00 EUR |

Macro Backdrop

Market sentiment remains neutral to positive with DACH equities outperforming global peers on a five-day basis. The Euro area yield curve is steepening, with the 10-year AAA yield at 3.02% and the 2-year yield at 2.48%, which creates a headwind for non-yielding assets like gold. The FX backdrop is mixed, with EUR/USD at 1.1437 and showing a year-to-date decline of -2.69%. Despite the strength in Euro yields, the Fed Chair’s recent comments suggesting inflation risks have cooled have injected life into the debasement trade, supporting gold’s resilience [T1][T8].Investment Thesis

Gold is currently navigating a correction phase following a historic rally into January 2026. The fundamental thesis remains anchored in structural diversification and reserve management. Despite recent volatility, the World Gold Council and OMFIF surveys indicate a record 45% of central banks expect to increase their own gold reserves over the next 12 months, reinforcing the metal’s role as a critical reserve asset in a fragmented geopolitical landscape [T3][T7]. Goldman Sachs forecasts sovereign demand will remain a primary pillar, targeting prices near $4,900 per ounce next year [T3].Bullish Drivers

The primary bullish catalysts for XAU/EUR are the unwinding of real yield pressure and persistent central bank accumulation. Fed Chair Warsh has signaled a shift toward dovishness, favoring trimmed-average measures and noting that inflation risks have come down, which could trigger a Fed pivot from hawkish to neutral [T1][T8]. On the demand side, central banks have been relentless buyers, with May seeing a net 41 tonnes of purchases and China adding 15 tonnes in June despite a sharp price decline [T4][T5][T6]. Technical analysis suggests a solid floor is forming around $4,000 per ounce, supported by this institutional buying [T5].Relative Positioning vs Bitcoin and Ethereum

Gold and Bitcoin are increasingly decoupling from traditional equity correlations, reacting to macro shifts rather than growth sentiment. On the day of the Fed Chair’s comments, gold rallied 1.1% while the S&P 500 declined 0.33%, with Bitcoin gaining 2.38% [T8]. This divergence highlights a growing “debasement trade” where both hard assets benefit from perceived monetary policy easing. While equities have been the primary beneficiary of the recent risk-on rotation, gold and crypto are positioning themselves as hedges against potential currency debasement and fiscal anxiety.Scenario Framework

- Bullish Scenario: The Fed successfully pivots to dovish policy as inflation expectations normalize. Real yields decline, and central bank buying accelerates. Gold breaks above its ATH, targeting the $4,900 level forecast by Goldman Sachs [T3].

- Base Case: The Fed maintains a “higher for longer” stance with at least one hike before year-end. Gold consolidates in a range of 3,600 to 3,800 EUR, supported by steady central bank demand but capped by rising Euro yields.

- Bearish Scenario: Real yields spike further due to sticky inflation or geopolitical escalation. The USD strengthens, pressuring XAU/EUR. Gold tests support levels near 3,500 EUR if the “debasement trade” reverses.

Valuation Discussion

The current price of 3,605.92 EUR represents a 23.08% drawdown from the January 2026 ATH of 4,688.32 EUR. Calculated implied USD pricing is approximately 4,125.00 EUR, which aligns with recent spot levels reported in the market [T8]. Valuation appears attractive relative to the 200-day moving average support levels discussed by analysts, who note the market is building a floor around $4,000/oz [T5]. However, the elevated Euro area yield curve (10Y at 3.02%) continues to weigh on the carry trade appeal of gold.Risks

The primary risk to the bullish thesis is the persistence of high real yields. If the Fed maintains a hawkish stance and inflation remains sticky due to geopolitical tensions, the dollar could strengthen, pressuring gold in EUR terms. Additionally, a sharp de-escalation in the Middle East conflict could remove the inflation hedge premium currently supporting the metal [T6].Appendix

Sources

- Gold and silver: From reset to setup heading into Q3 – KITCO [T1]

- These are the key factors that could restart the gold rally this year, or drive prices even lower – World Gold Council H2 Outlook – KITCO [T2]

- Central banks are still betting on gold – KITCO [T3]

- Central banks boost gold reserves with net 41 tonnes purchased in May – World Gold Council – KITCO [T4]

- China’s central bank buys the dip, increasing gold reserves by 15 tonnes in June – KITCO [T5]

- China gold reserves rise most since 2023 even as bullion tumbles – KITCO [T6]

- China’s top ETF is now gold, not stocks – Mining.com [T7]

- Warsh’s throwaway comment injects life into the debasement trade, for one day at least – MarketWatch [T8]

This report is AI-generated for informational purposes only and does not constitute investment advice. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.