Listen to the summary

Key Data Snapshot

| Asset | Price (EUR) | 24h Change | 200-Day Change | ATH (USD) | ATH Change |

|---|---|---|---|---|---|

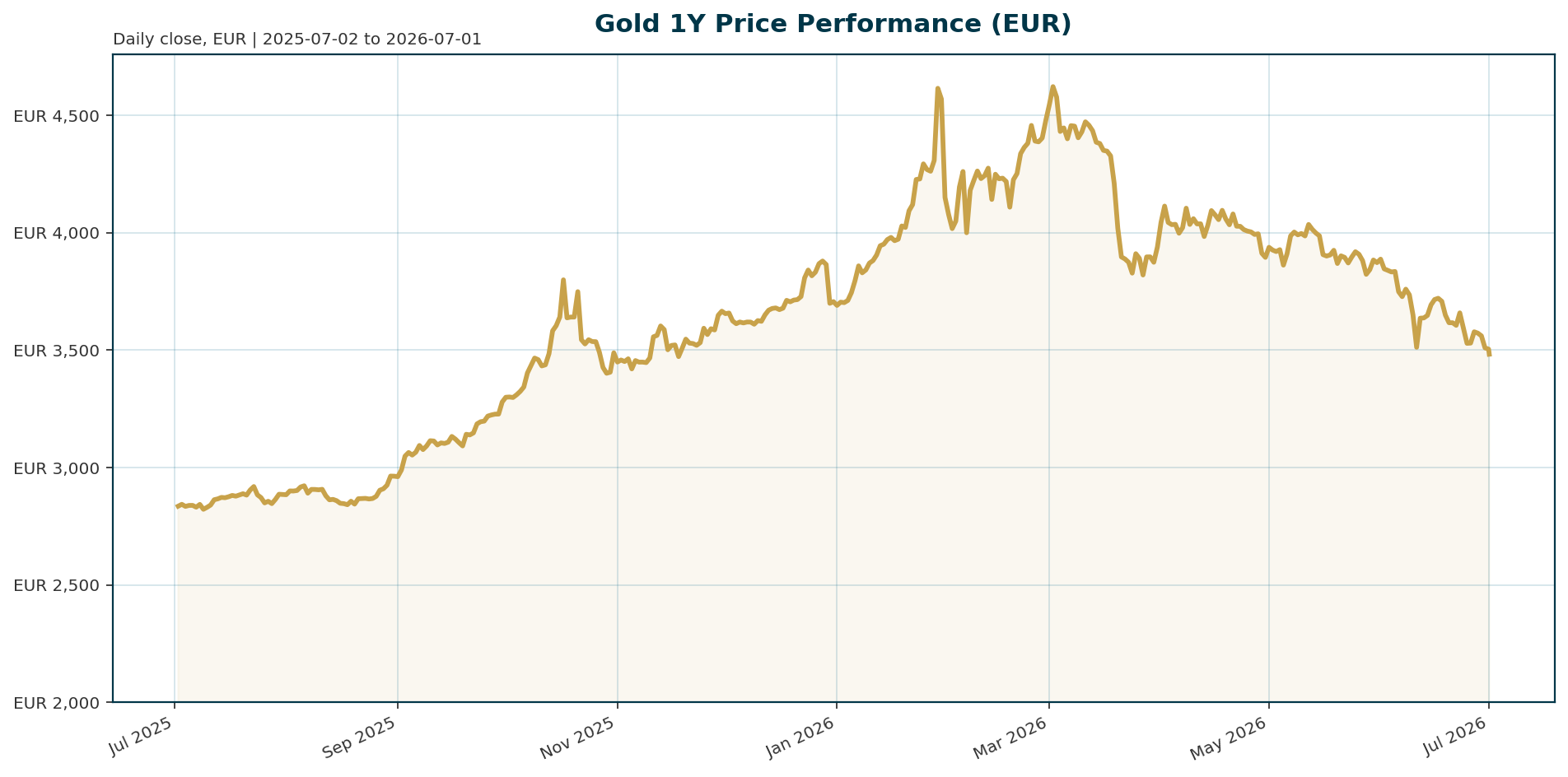

| Gold (XAU) | 3,482.69 | -0.016% | -5.14% | 4,688.32 | -25.72% |

Gold is currently consolidating after a record run, trading 34.9% below its all-time high in EUR terms (calculated as 4,688.32 USD * 1.1412 EUR/USD = 5,351.00 EUR) [T4]. The 200-day decline of -5.14% indicates a correction phase within a secular bull market. Institutional demand remains robust, with 61% of central banks expecting prices to trade between $5,000 and $6,000 per ounce by June 2027 [T1]. Bitcoin dominance stands at 55.37%, highlighting gold’s continued primacy as the primary store of value despite crypto competition [market_data].

Macro Backdrop

Risk sentiment is neutral with mixed equity momentum. The Nasdaq Composite leads on a five-day basis with a gain of 2.89%, while the Nikkei 225 is the weakest performer at -2.44% [market_overview]. The Euro area AAA 10Y yield is 2.92%, moving -4.8 basis points over five days, while the 10Y-2Y spread remains at 44.6 bp [market_overview]. The EUR/USD pair is weak at 1.1412, moving 0.14% over five days, which provides a tailwind for EUR-denominated gold. However, SocGen’s central scenario sees 10Y US real yields remaining above 2% through Q3, creating a high opportunity cost for holding non-yielding gold [T2]. Geopolitical risks remain elevated, with 85% of central banks citing the Middle East conflict as their top concern [T1].

Investment Thesis

The core thesis rests on a structural shift toward a multipolar global monetary system. Nearly 80% of reserve managers believe the global monetary system is transitioning toward a multipolar structure, necessitating a reduction in dollar exposure and an increase in alternative reserve assets like gold [T3]. Gold has moved to the center of reserve management strategy, with 82% of central banks holding it [T3]. As central banks shift from government bonds to gold as their second preferred long-term asset, demand is expected to remain resilient despite current price levels [T1].

Bullish Drivers

- Central Bank Re-entry: The Iran war de-escalation has allowed Hormuz to reopen, removing a major headwind. Central banks are eager to resume buying physical gold to protect against the weaponization of fiat currency [T5].

- Multipolar Diversification: A structural trend of diversifying away from the US dollar is accelerating. Central banks are actively increasing allocations to currencies other than the top eight and are viewing gold as a critical hedge against policy uncertainty [T3].

- Survey Optimism: Despite record prices, 61% of respondents expect gold to trade between $5,000 and $6,000 by June 2027, and only 28% view higher prices as discouraging purchases [T1].

- Fed Divergence: A potential scenario involving an “empire with no clothes” Fed—talking hawkish but taking no action—could trigger a divergence where gold rallies alongside equities [T5].

Relative Positioning vs Bitcoin and Ethereum

Despite the growth of the crypto asset class, gold maintains a dominant market share. With a market cap of 1.575 billion and a BTC dominance of 55.37%, gold remains the primary store of value narrative. Central bank survey data confirms gold is still the preferred long-term reserve asset over crypto, ranking second only to cash equivalents in long-term strategic allocations [T1].

Scenario Framework

- Base Case: US Real Yields decline gradually into H1 2027 as SocGen predicts, while central banks resume buying. Gold tests its previous all-time highs.

- Bull Case: Acceleration of the multipolar transition and a Fed pivot (rates falling below 2%) trigger a rapid re-rating. Gold targets the $5,000 to $6,000 range by mid-2027.

- Bear Case: Persistent US Real Yields above 2% through Q3 and a de-escalation of Middle East tensions lead to a re-test of the $3,000 support level.

Valuation Discussion

Current valuation is attractive relative to the all-time high, offering a risk reward for long-term holders. The survey expectations imply a potential 40% to 90% upside from current levels by mid-2027 (calculated as $5,000 to $6,000 USD converted to EUR). The price action suggests a correction phase rather than a top in the secular bull market, supported by the fact that central banks remain remarkably optimistic despite record prices [T1].

Risks

- Opportunity Cost: If US Real Yields remain above 2% through Q3, the opportunity cost of holding gold will cap upside [T2].

- ETF Selling: CPM Group notes ETF selling and Comex inventories not falling, which could prolong the current consolidation phase [T4].

- Geopolitical Flare-up: A sudden resurgence in the Middle East conflict could trigger a flight to USD, negatively impacting gold prices [T3].

- Euro Area Volatility: Euro area yields are mixed, and a sharp rise in Euro yields would weigh on EUR-denominated gold [market_overview].

Appendix

Sources

- Central banks see gold prices trading between $5,000 and $6,000 in 12 months – OMFIF Survey – KITCO [T1]

- Gold’s biggest buyers aren’t slowing down, but SocGen sees a more measured pace ahead – KITCO [T2]

- For first time, more central banks are set to shrink dollar holdings, survey finds – Reuters [T3]

- Gold & silver market update: Silver below $60, gold $4,100 test, ETF selling, Comex inventories, and Treasury gold rumors – KITCO [T4]

- Gold stocks & silver: The road to new highs – KITCO [T5]

- Alan Greenspan’s Legacy On Inflation And Trade – InsuranceNewsNet [T6]

- Gold and silver market update: Why interest rate changes may mislead investors – KITCO [T7]

This report is AI-generated for informational purposes only and does not constitute investment advice. The information contained herein is based on data available as of the date of publication and may become outdated without notice.

Important Note / Wichtiger Hinweis:

EN: This report may have been generated using AI. It processes data from publicly available sources. The content is provided for informational purposes only.DE: Dieser Bericht kann mithilfe von KI erstellt worden sein. Dabei werden Daten aus öffentlich zugänglichen Quellen verarbeitet. Die Inhalte dienen ausschließlich Informationszwecken.

* DE: Die ergänzenden Inhalte können KI-generiert sein. EN: The additional content may be AI-generated.